Your business’s general ledger plays a significant role in forecasting the financial health of your company. But if you’re slacking on your general ledger entries, your business could suffer the consequences.

So… how’s your small business general ledger lookin’? Does it need a little love? If so, read on to learn all about the general ledger, including what it is, the types of accounts in a ledger, and more.

What is a general ledger?

Your business general ledger is the foundation of your books. Your ledger is a record used to sort and summarize your transactions.

In your ledger, you’re responsible for recording debits and credits. Your credits and debits in your business ledger must always be in balance. Unbalanced credits and debits can impact your business’s financial statements and give you inaccurate financial reports.

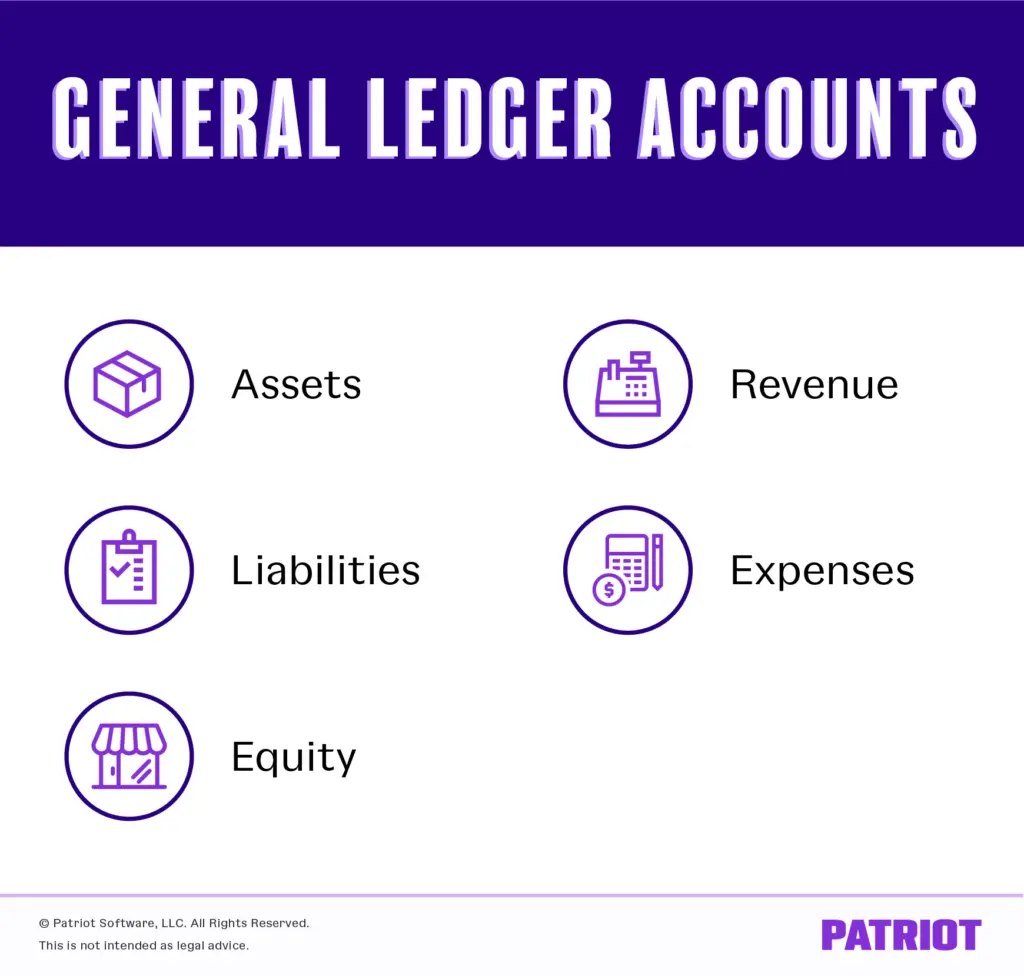

A company ledger is typically broken down into five main categories. You can also use sub-categories or sub-ledgers to give additional details about business transactions.

Accounts in a general ledger

Accounts work similarly to a filing cabinet. Each account is labeled with a name. And, you must file (or record) related transactions in each account.

The accounts in a general ledger come from your chart of accounts (COA). Your business’s COA categorizes your business transactions.

The most common accounts used in a small business ledger include:

- Assets

- Liabilities

- Equity

- Revenue

- Expenses

Assets are items that add value to your small business. Assets can be tangible (physical) or intangible (non-physical). Property, vehicles, trademarks, and patents are just a few examples of assets your business might have.

Liabilities are existing debts your business owes. Money owed to another business, vendor, organization, employee, or government agency is usually considered a liability. Some examples of liabilities include loans, mortgages, and accrued expenses.

Equity, also called net assets, net worth, and owner’s equity, is the amount of ownership you have in your company. You can calculate equity by subtracting your total liabilities from your total assets.

Revenue is the amount of money your business receives during a period. You earn operating revenue from main business operations and activities, such as sales. You can also earn revenue from activities that aren’t directly related to your business (e.g., renting a building), called non-operating revenue.

Expenses are costs associated with business operations. You likely have a variety of business expenses, including fees, equipment, supplies, rent, and utilities.

General ledger sub-accounts

Sub-accounts, or sub-ledgers, give you details behind your general ledger entries. Sub-accounts let you break down your accounts even further so you know exactly where funds are coming in and out of. You can find sub-accounts under each main account.

Take a look at examples of sub-accounts under each main account type below:

Asset sub-accounts:

- Checking

- Savings

- Petty cash

- Inventory

- Accounts receivable

Liability sub-accounts:

- Payroll tax liabilities

- Sales tax

- Accounts payable

Equity sub-accounts:

- Owner’s equity

- Common stock

- Retained earnings

Revenue sub-accounts:

- Product sales

- Earned interest

- Miscellaneous income

Expense sub-accounts:

- Insurance

- Rent

- Equipment

- Supplies

- Cost of goods sold

Creating a general ledger

When it comes to creating a general ledger, you have a few options for recording your transactions. You can:

- Create a general ledger on paper

- Use a spreadsheet

- Get accounting software

The size of your general ledger depends on how big your business is. If you have a smaller business, you might have fewer accounts and sub-accounts because you have fewer transactions.

Each general ledger entry should have:

- An account number (if applicable)

- Account name

- Beginning account balance

- Transaction type

- Customer, vendor, and employee name (if applicable)

- Date

- Description

- Debit and credit columns

- Ending account balance

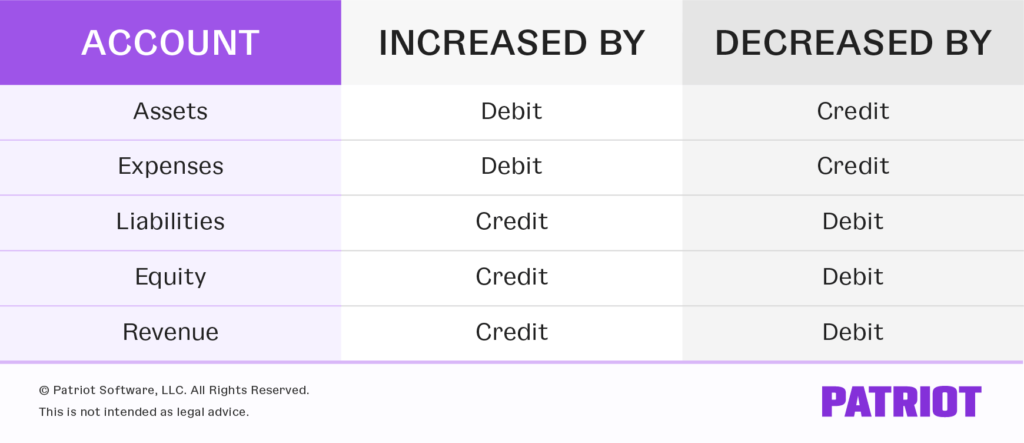

To post to the ledger, you must use double-entry bookkeeping. Double-entry bookkeeping means that you record two entries for every transaction. One entry is a debit and the other is a credit.

Again, your general ledger should contain a debit and credit entry for every transaction. Your debits and credits must always balance in your general ledger. If they don’t match, there’s an issue in your general ledger.

When creating a general ledger, divide each account (e.g., asset account) into two columns. The left column should contain your debits while the right side contains your credits.

Put your assets and expenses on the left side of the ledger. Your liabilities, equity, and revenue go on the right side. Both sides must have equal values for your ledger to balance.

At the end of each period, transfer your journal entries into your general ledger for small business.

Keep this chart in mind when making entries in your general ledger:

General ledger example

If you’re wondering what a general ledger looks like, you’ve come to the right place.

To get started, here’s what a basic general ledger might look like:

| Date | Description | Journal Ref. # | Transaction | Transaction |

| Debit | Credit | |||

| Total |

Now let’s take a look at an account in action. Take a look at a Checking Account within the general ledger:

| Date | Description | Debit Transaction | Credit Transaction |

| 9/13/19 | Cash Deposit | 100 | |

| 9/13/19 | Sale-Coffee | 100 | |

| 9/28/19 | Cash Deposit | 500 | |

| 9/28/19 | Sale-Cake | 500 | |

| Total | 600 | 600 |

As you can tell, the transactions above balance each other out. If your accounts don’t balance, you might have forgotten to record a transaction, entered an incorrect amount, or miscalculated totals.

Importance of a general ledger

General ledgers are an essential part of the accounting process. Without a general ledger, your accounting books can quickly become sloppy and disorganized, thus causing financial inaccuracies and issues down the road.

Your general ledger provides necessary information to create financial statements, like your business balance sheet, cash flow statement, and income statement. Your financial statements can give you a clear snapshot of your business’s financial well-being.

Your general ledger can also help you with things like:

- Preparing for an audit

- Organizing business transactions

- Getting small business loans

- Reporting real financial figures (not forecasts)

- Balancing your books

Need help organizing your business’s transactions? Patriot’s online accounting software lets you easily record income and expenses. Start your free trial today!

This article has been updated from its original publication date of September 17, 2012.

This is not intended as legal advice; for more information, please click here.