Before you can begin looking into your business’s profit, you need to understand and know how to calculate cost of goods sold (COGS). So, where do you begin? Start here by learning all about COGS, including how to get cost of goods sold using the cost of goods sold equation.

What is cost of goods sold?

Your cost of goods sold, also known as cost of sales or cost of services, is how much it costs to produce your business’s products or services. The cost of goods sold (COGS) is essential for calculating how much you spent to produce the goods you sell.

COGS include the following costs:

- Direct labor

- Materials to create the good

Cost of goods sold only includes the expenses that go into the production of each product or service you sell (e.g., wood, screws, paint, labor, etc.). When calculating cost of the goods sold, do not include the cost of creating products or services that you don’t sell.

COGS excludes indirect costs, such as distribution expenses. Do not factor things like utilities, marketing expenses, or shipping fees into the cost of goods sold. Again, COGS only includes the production costs.

- Easy-to-use accounting software

- Record income and expenses anytime, anywhere

- Enjoy free, USA-based support

COGS vs. operating expenses

As a business owner, you’ve likely heard of operating expenses at some point. But, what’s the difference between COGS vs. operating expenses?

Operating expenses, or OPEX, are costs companies incur during normal business operations to keep the company up and running. Essentially, operating expenses are the opposite of COGS and include selling, general, and administrative expenses.

Chances are, if an expense doesn’t fall under COGS, it typically falls under operating expenses. Here are a few examples of operating expenses:

- Rent

- Equipment

- Marketing

- Salaries and wages (other than direct labor)

- Insurance

- Office supplies

- Insurance

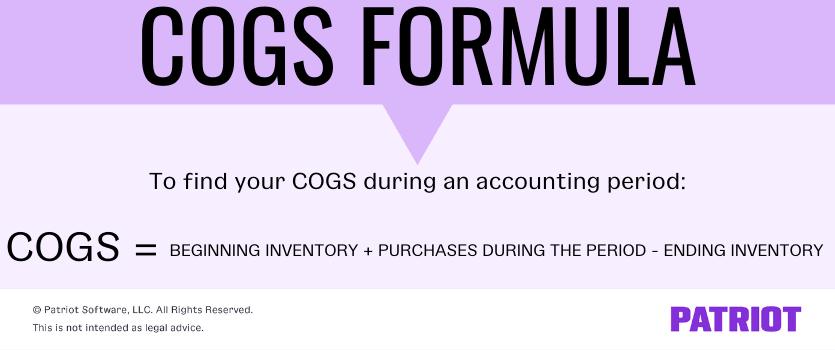

Cost of goods sold formula (COGS formula)

Calculating COGS is pretty straightforward. To calculate COGS, use the COGS formula:

COGS = Beginning Inventory + Purchases During the Period – Ending Inventory

Not sure where to get the above information to plug into the formula? Here’s a breakdown of everything you need:

- Beginning inventory: Amount of inventory left over from the previous period (e.g., month, quarter, etc.)

- Purchases during the period: Cost of what you purchased during the accounting period

- Ending inventory: Inventory you did not sell during the period

After you gather the above information, you can begin calculating your cost of goods sold. Depending on your business and goals, you may decide to calculate COGS weekly, monthly, quarterly, or annually.

What is an example of cost of goods sold?

Let’s say you want to know your cost of goods sold for the quarter. You record beginning inventory on January 1 and ending inventory on March 31 (end of Quarter 1).

Your business has a beginning inventory of $15,000. Your purchases total up to $7,000 for the quarter. And, your ending inventory is $4,000. Find your total COGS for the quarter using the cost of goods sold calculation.

COGS = Beginning Inventory + Purchases During the Period – Ending Inventory

COGS = $15,000 + $7,000 – $4,000

Your cost of goods sold for the quarter is $18,000.

Calculating gross profit

After determining cost of goods sold, you can find your business’s gross profit for the period. Gross profit is the revenue left over after you deduct the costs of making a product or providing a service. To find gross profit, use the following formula:

Gross Profit = Revenue – COGS

Let’s say you have revenue of $50,000 for the quarter. Subtract your COGS of $18,000 from $50,000.

Gross Profit = $50,000 – $18,000

Your gross profit for the period is $32,000.

Importance of COGS in business

So, why is your cost of goods sold so important to your business? Well, your COGS can tell you a lot of information, including:

- How much your profits are for a period

- If you need to change your pricing

- If you’re spending too much on costs to produce the product or service

Profits

Again, you can use your cost of goods sold to find your business’s gross profit. And when you know your gross profit, you can calculate your net profit, which is the amount your business earns after subtracting all expenses.

Knowing your business’s profits can help you:

- Make financial decisions

- Seek financing (e.g., business loan)

- Determine if you need to make adjustments

Setting prices for products and services using COGS

Pricing your products and services is one of the biggest responsibilities you have as a business owner. And just like Goldilocks, you need to find the price that’s just right for your products or services. Otherwise, you could wind up losing out on profits.

If you price your products too high, you may see a decrease in interest and sales. And if you price your products too low, you won’t turn enough of a profit.

To find the sweet spot when it comes to pricing, use your cost of goods sold. If you know your COGS, you can set prices that leave you with a healthy profit margin. And, you can determine when prices on a particular product need to increase.

For example, let’s say your cost of goods sold for Product A equals $10. You need to price the product higher than $10 to turn a profit. If you price it less than $10, you will not turn a profit.

Costs

Your COGS can also tell you if you’re spending too much on production costs. The higher your production costs, the higher you need to price your product or service to turn a profit.

If you notice your production costs are too high, you can look for ways to cut down on expenses, such as finding a new supplier.

How to get cost of goods sold in accounting

Learn how to calculate the cost of goods sold using the COGS formula.

- Determine beginning inventory

Find your business’s beginning inventory for the period.

- Add purchases during the period

Add any purchases made during the accounting period.

- Subtract ending inventory

Subtract the inventory remaining at the end of the period.

You can find your cost of goods sold on your business income statement. An income statement details your company’s profits or losses over a period of time, and is one of the main financial statements.

On your income statement, COGS appears under your business’s sales (aka revenue). Deduct your COGS from your revenue on your income statement to get your gross profit.

Your COGS also play a role when it comes to your balance sheet. The balance sheet lists your business’s inventory under current assets. Use your balance sheet to find your ending inventory balance.

What type of account is cost of goods sold?

So, what kind of account is COGS? Is cost of goods sold an asset? Liability?

COGS is a type of expense. Expenses are costs your business incurs during operations.

When you create a COGS journal entry, increase expenses with a debit, and decrease them with a credit.

Changes in COGS

Your cost of goods sold can change throughout the accounting period. COGS depends on changing costs and the inventory methods you use.

The three inventory costing methods include:

- FIFO (first in, first out): First items made or purchased are the first sold

- LIFO (last in, first out): Last goods made or purchased are the first sold

- Average cost: Calculate average cost per item

The method you use depends on your type of inventory. And, the IRS sets specific rules for which method you can use and when you can make changes to your inventory cost method.

If you use the FIFO method, the first goods you sell are the ones you purchased or manufactured first. Generally, this means that you sell your least expensive products first. As a result, you record a lower cost of goods sold.

Under the LIFO method, you sell the most recent goods you purchased or manufactured. With LIFO, your COGS might be higher.

With the average method, you take an average of your inventory to determine your cost of goods sold. This keeps your COGS more level than the FIFO or LIFO methods.

This article has been updated from its original publication date of August 25, 2015.

This is not intended as legal advice; for more information, please click here.