If you want to take advantage of business deductions before the end of the year, you may decide to prepay some of your expenses. But, hold up! Before you do that, you need to learn about the 12-month rule for prepaid expenses.

What are prepaid expenses?

So, what do prepaid expenses include? Prepaid expenses are expenses you pay for in advance before receiving a product or service. Any time you pay for something in advance, you must record it in your books as a prepaid expenses journal entry.

Prepaid expenses can include, but are not limited to:

- Rent

- Small business insurance

- Equipment

- Estimated taxes

- Some utility bills

- Interest expenses

Businesses and individuals alike can have prepaid expenses. If your business pays for products or services in advance before receiving them, you have a prepaid expense.

What is the 12-month rule?

If you use the cash method of accounting, you deduct expenses in the tax year you actually pay them. But, you may not be able to deduct an expense you pay in advance, aka a prepaid expense.

A prepaid expense is only deductible in the year to which it applies, unless it qualifies for the 12-month rule…

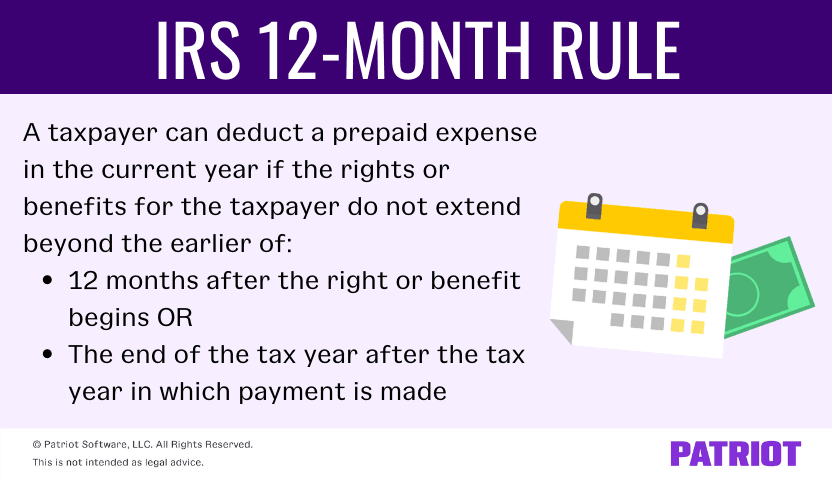

Under the IRS 12-month rule, a taxpayer can deduct a prepaid expense in the current year if the rights or benefits for the taxpayer do not extend beyond the earlier of:

- 12 months after the right or benefit begins OR

- The end of the tax year after the tax year in which payment is made

You can use the 12-month rule for business insurance premiums, business licenses, rent and lease payments, and payments to terminate business contracts. But, you cannot use the rule for payments for interest, loans, and other financial interests, or purchases of furniture, equipment, and other long-term capital assets.

If you use cash-basis accounting, you can deduct prepaid expenses as long as the 12-month rule applies.

In other cases, you may need to use the general rule. Under the general rule, you may not deduct the full amount of an advance payment covering more than 12 months. And, you must deduct a portion of the payment based on the year it applies.

If you haven’t been using the 12-month rule and/or the general rule, contact the IRS to get approval before using them.

For more information on the 12-month rule for prepaid expenses, check out Publication 538.

12-Month rule: Examples

The 12-month rule scrambling your brain? You’re not alone. To make sense of the rule, let’s take a look at a couple of examples of how it all works.

Example 1

Say your business pays $5,000 on December 31, 2021 for an insurance policy that is effective January 1, 2022 – December 31, 2022.

Because the benefit (aka insurance policy) does not go past a 12-month period or beyond the end of the taxable year following the year the payment was made, the 12-month rule applies. And, the full $5,000 is deductible in 2021.

Example 2

You’re a cash-basis taxpayer using a calendar year. On September 1, 2021, you pay $1,000 for business insurance covering the first six months of 2022 (January through June 2022).

In this situation, the 12-month rule applies even though the benefit begins in the new year because it does not extend beyond the end of 2021. Deduct the full $1,000 in 2021.

General rule: Example

You are a calendar year taxpayer and pay $6,000 in 2021 for an insurance policy that is effective for three years (or 36 months). The policy begins July 1, 2022.

In this situation, the 12-month rule does not apply. Instead, the general rule that an expense paid in advance is only deductible in the year to which it applies is applicable.

Because you need to follow the general rule, only $1,000 [(6 months / 36 months) X $6,000] is deductible in 2022. In 2023 and 2024, only $2,000 is deductible [(12 months / 36 months) X $6,000] and the remaining $1,000 is deductible in 2025 ($6,000 – $1,000 – $2,000 – $2,000).

- Easy onboarding with startup wizard

- Import your customers, vendors, and trial balance

- Create invoices, pay bills, and generate financial reports

How does the 12-month rule work for accrual accounting?

The 12-month rule works differently for accrual-basis taxpayers. So, listen up.

There are two tests your business must pass before you can apply the 12-month rule:

- All events test

- Economic performance test

Generally, the taxpayer cannot deduct a prepaid expense until the obligation to pay is fixed (all events have occurred to establish liability), the cost is determinable, and the taxpayer actually receives the prepaid product or service (economic performance).

Some cash payments can result in economic performance, including insurance contracts, warranty contracts, taxes, and workers’ compensation liability.

Say you pay $20,000 on December 31, 2021 for property taxes that cover the first six months of 2022 (January – June). Because taxes count as economic performance, you can deduct the prepaid property tax expense in 2021.

This is not intended as legal advice; for more information, please click here.