As your small business begins to make transactions, you must record them in your books. If you want an “easy” way to track business finances, you may consider using single-entry bookkeeping instead of double-entry bookkeeping.

Single-entry bookkeeping lets you record transactions quickly so you can get back to running your business. But what are the hazards of using single-entry bookkeeping?

What is single-entry bookkeeping?

Single-entry bookkeeping is a method for recording your business’s finances. You record one entry for every transaction. The single-entry method is the foundation of cash-basis accounting. You mostly record cash disbursements and cash receipts with the single-entry system of bookkeeping.

Under single-entry bookkeeping, record incoming and outgoing money in the cash book. Usually, you track assets and liabilities separately.

What’s a cash book

Record transactions with the single-entry system in a cash book. A cash book is a larger version of a check register. It uses columns to organize different uses of cash for your business.

Cash book columns track key information about your finances. Each transaction gets a line in the cash book. Record the following items with the single-entry bookkeeping system:

- Date: The day the transaction takes place

- Description: A brief explanation of the transaction

- Income/expenses: The value of the transaction

- Balance: The running total of how much cash you have on hand

The first entry in the cash book should be the cash balance at the beginning of the accounting period. During the period, record transactions as individual line items. The last line in the cash book should be the cash balance at the end of the accounting period.

The items in your cash book will vary, depending on your business. Here is a single-entry bookkeeping example for using a cash book:

| Description | Date | Notes | Expense (Debit) | Income (Credit) | Account Balance |

|---|---|---|---|---|---|

| Starting Balance | 6/1 | 2,000 | |||

| Rent | 6/3 | 800 | 1,200 | ||

| Sales | 6/8 | 500 | 1,700 | ||

| Supplies | 6/20 | 200 | 1,500 | ||

| Ending Balance | 6/30 | 1,500 |

Income statement for single-entry bookkeeping

The single-entry bookkeeping system is centered on the results in your company’s income statement. The income statement shows information about a specific accounting period. It is also called a profit and loss statement for small business.

The income statement shows profitability during a time frame. It begins with sales and itemizes financial details down to the net income. Sales and gains are at the top of the income statement. Business expenses and losses are listed next. The bottom figure is the net income, or the take-home earnings after expenses and debts are paid.

To create an income statement, compile information from your cash book.

Single-entry bookkeeping vs. double-entry bookkeeping

If you don’t use the single-entry method, record transactions with double-entry bookkeeping. The double-entry method is a little more complicated than single-entry and is the basis of accrual accounting.

With double-entry bookkeeping, you record two entries for every business transaction. Each entry is either a debit or credit. The entries are equal but opposite. Your debit and credit entries must be the same values.

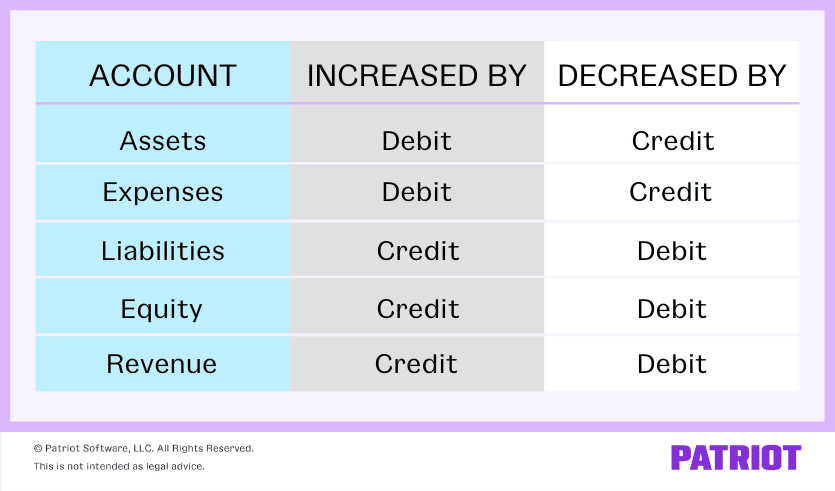

Some accounts are increased by debits and decreased by credits. Other accounts are increased by credits and decreased by debits. The following chart shows how each account is affected by debits and credits:

Double-entry bookkeeping reduces the chance of errors because you must balance the entries. Some businesses are required to use double-entry bookkeeping.

What are the risks of single-entry bookkeeping?

Single-entry bookkeeping is the simplest way to organize your accounting records. But single-entry bookkeeping is not the best fit for some businesses. Think about your business’s size, industry, and specific needs before choosing a method.

The risks of single-entry bookkeeping include:

- Inaccurate books: Single-entry accounting only records transactions once, increasing the risk of common accounting errors because there is no matching system like with double-entry.

- Lack of information: Single-entry bookkeeping shows less information about your business’s financial health. On the other hand, double-entry bookkeeping provides a detailed record of all the money coming in and going out of your business.

- Difficult tracking: Assets and liabilities are more difficult to track with single-entry bookkeeping than double-entry bookkeeping.

Who uses single-entry bookkeeping?

Again, consider the risks of single-entry bookkeeping before deciding between single-entry and double-entry accounting. Additionally, keep IRS rules in mind.

You may consider the single-entry method if you:

- Make less than $5 million in annual gross sales or have less than $1 million in gross receipts for inventory sales, according to the IRS

- Are a small business that operates as a sole proprietorship, partnership, S Corp, or LLC

- Collect customer payments at the point of sale

- Operate a service business

Alternatively, consider the double-entry method if you:

- Make more than $5 million in annual gross sales or have more than $1 million in gross receipts for inventory sales

- Operate as a corporation or a partnership with a C Corp partner

- Send invoices or let customers buy on credit

- Have inventory

- Easy onboarding with startup wizard

- Patented Dual-Ledger Accounting

- Free USA-based support

New businesses or companies with a low number of transactions and uncomplicated financial tracking needs may be able to use single entry, but consult your accountant if you have more questions.

Need a simple way to keep your small business books? Patriot’s online accounting software is easy-to-use and made for small business owners and their accountants. We offer free, USA-based support. Try it for free today.

This article is updated from its original publication date of June 2, 2017.

This is not intended as legal advice; for more information, please click here.