When you start a company, there are several business structures. Two popular types of business structures are an S corporation and LLC. Are you choosing between these structures? Find out the key differences between S Corp vs. LLC and learn which is best for you.

S Corp vs. LLC

Many business owners decide between starting an S Corp or LLC. According to the National Association of Small Business, 35% of small businesses are LLCs, and 33% are S corporations. That’s a pretty tight race.

So, what’s the difference between LLC and S Corp? What are their advantages and disadvantages? Get the answers to these questions and more by checking out our S corporation vs. LLC Q&A below.

What is an S Corp?

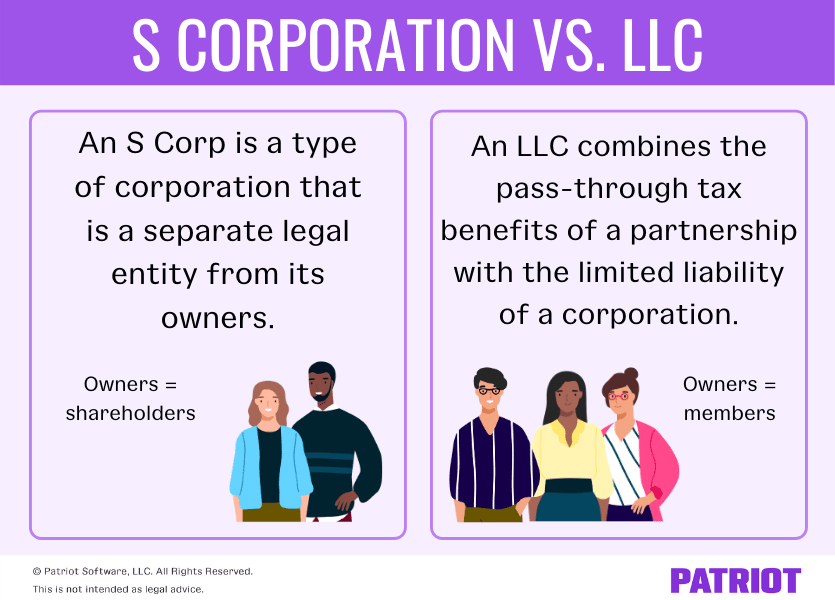

What is an S Corp? An S Corp, or S corporation, is a type of corporation that is a separate legal entity from its owners.

If you own an S Corp, you can receive both wages and distributions.

To become an S Corp, your business must first register as a C corporation or LLC and then elect S Corp status using Form 2553.

Many business owners decide to become an S Corp because of the perk of limited liability.

What is an LLC?

What is an LLC? A limited liability company (LLC) combines the pass-through tax benefits of a partnership (which we’ll get to later) with the limited liability of a corporation.

An LLC can be either a single-member or multi-member business. Like an S corporation, an LLC is a separate entity from its owners.

An LLC is a popular structure for business owners because of its flexibility.

What are the requirements to start an S Corp or LLC?

S corporation requirements: According to the IRS, you can only structure your business as an S Corp if you meet all of the following:

- Your business is in the United States

- You have only allowance shareholders (e.g., individuals, certain trusts, and estates)

- This does not include partnerships, corporations, or non-resident alien shareholders

- There are no more than 100 shareholders (owners)

- You have only one class of stock

- The business is not an ineligible corporation (i.e., certain financial institutions, insurance companies, and domestic international sales corporations)

- All owners are U.S. citizens or permanent U.S. residents

LLC requirements: Each state has its own set of rules for forming and operating a limited liability company. Some businesses are not allowed to form an LLC because of government regulations (e.g., companies in the insurance industry). Check your state’s laws to see if your business can be an LLC.

S Corp vs. LLC: What’s the difference?

There are three main ways that S corporations and LLCs differ. They include:

- Taxes

- Management structure

- Shareholder/member structure

Taxes

LLC: Limited liability companies use pass-through taxation. With pass-through taxation, the business itself does not pay income taxes. Instead, the owners report business income and pay taxes on their personal tax returns. The tax falls onto the owners, resulting in additional tax forms.

Single-member LLCs are taxed as sole proprietorships. The owner of a single-member LLC must report the business’s profits and losses by attaching Schedule C to their personal tax return.

On the other hand, multi-member LLCs are treated like partnerships when it comes to taxes. Owners report business income and pay taxes on their personal tax returns. And, each owner must attach Schedule K-1 to their return to show the LLC’s profits and losses. The LLC must also send Form 1065 to the IRS.

An LLC can choose to be taxed as an S corporation instead by filing Form 2553. LLCs can also choose to be taxed as a corporation by filling out Form 8832 and sending it to the IRS. However, an LLC taxed as a corporation does not get pass-through tax benefits.

Owners of an LLC are considered self-employed. Because of this, members must also pay self-employment taxes (Social Security and Medicare taxes) to the IRS. Owners are responsible for estimating, paying, and reporting taxes.

S Corp: Like LLCs, S corporations also don’t have to worry about double taxation. Profits and losses are passed through directly to the owner’s personal income without being subject to corporate tax rates. Only the owners, or shareholders, of an S Corp are taxed.

An S Corp is only taxed at the personal level, but shareholders are not personally liable for the S Corp’s losses.

With an S corporation, shareholders receive a salary and the business pays their payroll taxes. The payroll taxes can be deducted as a business expense from the company’s taxable income. Any leftover profits go to shareholders in the form of dividends.

File Form 1120-S, U.S. Income Tax Return for an S Corporation, if your business is structured as an S Corp. Individual owners receive Schedule K-1, showing distributions from the corporation.

Management structure

LLC: The members (owners) of an LLC are able to choose whether owners or certain managers run the business. When multiple members manage an LLC, the business operates more like a partnership.

S corporation: S corporations must have a board of directors and corporate officers. An S Corp’s board of directors oversees management and is in charge of business decisions. Corporate officers (e.g., CEO, CFO, etc.) manage the day-to-day business operations.

Shareholder/member structure

S Corp: S Corps can’t have more than 100 shareholders total, and all shareholders must be U.S. citizens. Although S corporations aren’t allowed to set up subsidiaries, they can issue one class of stock.

LLC: LLCs can have an unlimited number of members. These members can include non-U.S. citizens or residents. And, LLCs are allowed subsidiaries with no restrictions. However, LLCs cannot issue stock.

What are the pros and cons of S Corps and LLCs?

Like anything, there are pros and cons to forming an LLC or S Corp. Take a look at the advantages and disadvantages of each below.

LLC pros:

- Limited liability (members are not personally responsible for business debts)

- Pass-through taxation

- Can be managed by members

- Easy to establish

- Ability to change tax structure (e.g., S Corp election)

- No limit on number of members

- Subsidiaries with no restrictions

- Non-U.S. citizens or residents can be members

LLC cons:

- Pay self-employment taxes (15.3%)

- File additional tax forms

- More difficult to raise money

- Cannot issue stock

- Limited life (dissolve or reform your LLC if an owner joins or leaves)

S Corp pros:

- Limited liability for shareholders and management

- Pass-through taxation

- Don’t have to worry about double taxation

- Shareholders receive a salary and can receive dividends

- Don’t have to pay self-employment taxes (15.3%) on dividends

- Perpetual existence (business still exists even if the owner leaves or dies)

S Corp cons:

- Limited ownership (no more than 100 shareholders)

- More requirements for formation

- Limited to one class of stock

- Ongoing fees (e.g., franchise tax fees)

- U.S. citizens and permanent residents only

How to start an LLC or S Corp

Starting an LLC: To start an LLC, follow the steps below:

- Decide which state to form your LLC in if you do business in multiple states

- Select your LLC’s name (if you haven’t already)

- Choose a registered agent (i.e., individual or company that agrees to accept legal papers on behalf of the LLC)

- Prepare an operating agreement (i.e., guidelines for your LLC)

- File articles of organization with your state

When it comes to filing articles of organization, most states have a form you can fill out. Typically, you also need to pay a filing fee to become an LLC.

Keep in mind that each state’s rules for starting an LLC may differ. Check with your state for more information about forming a limited liability company.

Starting an S Corp: To form an S corporation, first start an LLC or corporation. Then, file Form 2553, Election by a Small Business Corporation, to elect S Corp status. You must meet the S corporation requirements to form an S Corp (e.g., one class of stock, fewer than 100 shareholders, etc.).

You need the following information to fill out Form 2553:

- Business name and address

- Employer Identification Number (EIN)

- Date incorporated

- State of incorporation

- Date you want S Corp to start (aka election date)

- Tax year information

- Contact information for officer or legal representative for the company

- Shareholder information (e.g., name, SSN, stock owned, etc.)

- Signature

Mail or fax your completed form to the IRS. You cannot e-File Form 2553. You must file Form 2553 no later than two months and 15 days after the beginning of the tax year when you want the S Corp election to take effect.

Whether it’s an S Corp, an LLC, or another type of business structure, you need an easy way to track your business’s income and expenses. With Patriot’s accounting software, you can streamline the way you record transactions and get back to what matters most … your business. Try it for free today!

This article has been updated from its original publication date of January 14, 2021.

This is not intended as legal advice; for more information, please click here.