Employers are responsible for paying state unemployment (also called SUI or SUTA) taxes when running payroll. Your SUI rate can vary widely by state, industry, and other factors. So, what’s your SUTA tax rate?

Luckily, your state typically assigns a unique SUI tax rate to your business, which takes out the guesswork. However, new employers can generally expect a standard new employer SUTA tax rate.

Read on to learn 2026 new employer tax rates by state, plus 2026 employer tax rate ranges for experienced employers.

- Employers pay state unemployment (SUTA/SUI) taxes; rates vary by state, industry, and employer experience.

- New employers often receive a standard state-assigned SUTA rate; some states use different rates by industry.

- SUTA is typically employer-only; Alaska, New Jersey, and Pennsylvania require employee contributions too.

- States set taxable wage bases and rate ranges; your assigned rate depends on factors like claims and industry.

- Register with your state for an employer account to get your SUTA rate and report and pay quarterly.

What are SUTA taxes?

State unemployment tax, along with federal unemployment tax, is a tax that’s a percentage of employee wages. These taxes fund unemployment programs and pay out benefits to employees who lose their jobs through no fault of their own.

Generally, unemployment taxes are employer-only taxes, meaning you do not withhold the tax from employee wages. However, some states (Alaska, New Jersey, and Pennsylvania) require that you withhold additional money from employee wages for state unemployment taxes.

We’ll calculate, collect, file, and remit your payroll taxes for you. Ready to get back to business?

Each state sets a different range of tax rates. Your tax rate might be based on factors such as:

- Industry

- How many former employees received unemployment benefits

- Experience

States also set wage bases for unemployment tax. This means you only contribute unemployment tax until the employee earns above a certain amount.

| A Tax of Many Names! |

|---|

| State unemployment taxes can be referred to as SUTA tax, state unemployment insurance (SUI) tax, or reemployment tax. |

You pay SUTA tax to the state where the work is taking place. If your employees all work in the state your business is located in, you will pay SUTA tax to the state your business is located in. But if your employees work in different states, you will pay SUTA tax to each state an employee works in.

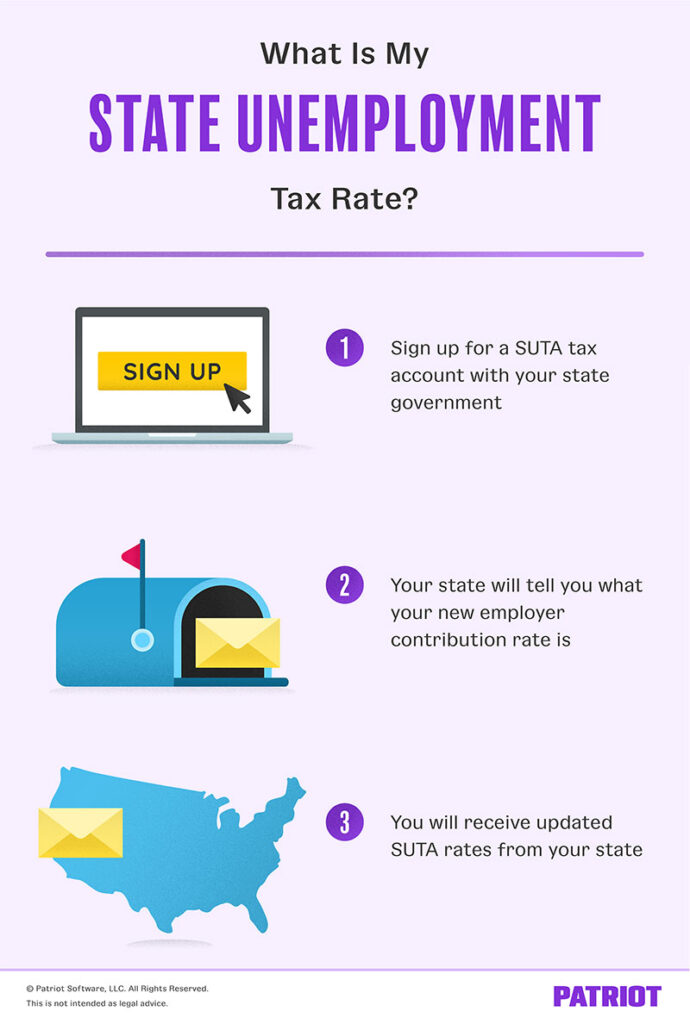

How to get your SUTA tax rate

When you become an employer, you need to begin paying state unemployment tax. To do so, sign up for a SUTA tax account with your state.

You can register as an employer online using your state’s government website. You might also be able to register for an account by mailing a form to your state. Each state has a different process for obtaining an account. Check your state’s government website for more information.

To register for an account, you need to provide information about your business, such as your Employer Identification Number. When you register for an account, you will obtain an employer account number.

Intimidated by the thought of state registration? For state tax registration made simple, try our partner, CorpNet.

Once registered, your state tells you what your SUI rate is. Your state also tells you what your state’s wage base is.

Many states give newly registered employers a standard new employer rate. The state unemployment insurance rate for new employers varies.

Some states split new employer rates up by construction and non-construction industries. For example, new employers receive a SUTA rate of 1.25% in Nebraska, but all new construction employers receive a SUTA rate of 5.4%.

If you live in a state that doesn’t use a standard new employer rate, you must wait for your state to assign you your starting rate.

Your state will eventually change your new employer rate. The amount of time depends on the state. You may receive an updated SUTA tax rate within one year or a few years. Most states send employers a new SUTA tax rate each year.

Generally, states have a range of unemployment tax rates for established employers. Your state will assign you a rate within this range. For example, the SUTA tax rates in Arizona range from 0.03% – 8.36%.

SUI tax rate by state

So, how much is unemployment tax? Here is a list of the non-construction new employer tax rates for each state and Washington D.C.

Note that some states require employees to contribute state unemployment tax.

We’ll be updating our chart as more states release their SUTA tax rate information. Stay tuned!

| State | New Employer Tax Rate 2026 | Employer Tax Rate Range 2026 | Taxable Wage Base 2026 |

|---|---|---|---|

| Alabama | 2.7% | 0.59% – 6.19% | $8,000 |

| Alaska | 1.5% standard rate 0.50% employee share | 1.50% – 5.90% (including employer share and employee share of 0.50%) | $54,200 |

| Arizona | 2.0% | 0.03% – 8.36% | $8,000 |

| Arkansas | 0.2% – 5.1% | $7,000 | |

| California | 3.4% | 1.5% – 6.2% | $7,000 |

| Colorado | 3.05% | 0.72% – 10.85% (+ Support Surcharge and Solvency Surcharge) | $30,600 |

| Connecticut | 1.9% | 1.10% – 9.90% | $27,000 |

| Delaware | 1.0% | 0.3% – 5.4% | $14,500 |

| D.C. | The higher of 2.7% or the average rate of all employer contributions in the preceding year | $9,000 | |

| Florida | 2.7% | 0.1% – 5.4% | $7,000 |

| Georgia | 2.7% | ||

| Hawaii | 2.4% | 5.6% maximum | $64,500 |

| Idaho | 1.0% standard rate (including the 0.03% workforce rate, 0.97% UI rate, and 0.0% admin rate) | 0.208% – 5.4% (including the workforce rate, UI rate, and admin rate) | $58,300 |

| Illinois | 3.35% for most employers; 3.45% for new employers in Administrative Support & Waste Management, plus undetermined NAICS | 0.75% – 7.05% | $14,250 |

| Indiana | 2.5% | ||

| Iowa | 1.0% | 0.0% – 5.4% | $20,400 |

| Kansas | 1.75% | 0.0% – 6.95% | $15,100 |

| Kentucky | 2.7% | 0.3% – 9.0% | $12,000 |

| Louisiana | Varies | 0.09% – 6.2% | $7,000 |

| Maine | 2.54% (including the 0.14% CSSF rate and 0.17% UPAF rate) | 0.31% – 6.6% (including assessments) | $12,000 |

| Maryland | 1% – 2.6% | 0.3% – 7.5% | $8,500 |

| Massachusetts | 2.13% | ||

| Michigan | 2.7% | 0.06% – 12.2% If an employer has a filing delinquency, the max rate will be 12.2% + a penalty rate of 3%. | $9,000 If employer has a filing delinquency, their wage base will be raised to $9,500. |

| Minnesota | Varies | Maximum of 8.9% | $44,000 |

| Mississippi | 1.0% (1st year), 1.1% (2nd year), 1.2% (3rd year) | ||

| Missouri | 1.0% for nonprofits and 2.376% for mining, construction, and all other employers | $9,000 | |

| Montana | Varies | 0.00% – 6.12% (plus an AFT rate) | $47,300 |

| Nebraska | 1.25% | 0.0% – 5.4% | $9,000 for most employers $24,000 for employers assigned the maximum rate |

| Nevada | 2.95% | 0.25% – 5.4% | $43,700 |

| New Hampshire | 2.7% less the current quarter trust fund reduction | ||

| New Jersey | 2.8% (including the 0.1175% Workforce Development and Supplemental Workforce Funds) until June 30, 2026 Employee rate of 0.425% (including the 0.0425% Workforce Development and Supplemental Workforce Funds) | $44,800 | |

| New Mexico | 1.0% or the industry average rate, whichever is greater | $34,800 | |

| New York | 4.1% (including the RSF rate of 0.075%) | $17,600 | |

| North Carolina | 1.0% | 0.06% – 5.76% | $34,200 |

| North Dakota | 1.03% (positive-balanced employers) or 6.09% (negative-balanced employers) | ||

| Ohio | 2.85% | 0.4% – 10.1% | $9,500 |

| Oklahoma | 1.5% | 0.2% – 5.8% | $25,000 |

| Oregon | 2.4% | 0.9% – 5.4% | $56,700 |

| Pennsylvania | 3.822% | 1.419% – 10.3734% | $10,000 |

| Rhode Island | 1.21% (including the 0.21% Job Development Assessment) | 0.9% – 9.4% | $30,800 (or $32,300 for negative-balanced employers) |

| South Carolina | 0.21% (including 0.06% Contingency Assessment) or 1%, whichever is higher | 0.06% – 5.46% (including 0.06% Contingency Assessment) | $14,000 |

| South Dakota | 1.2% UI plus an Investment Fee of 0.55% | $15,000 | |

| Tennessee | 2.7% for the first 3 years of the account | ||

| Texas | 2.7% or the industry average rate, whichever is greater | $9,000 | |

| Utah | Varies | 0.1% – 7.1% | $50,700 |

| Vermont | 1.0% for most employers (exceptions for out-of-state employers in certain industries) | $15,400 | |

| Virginia | 2.5% (plus add-ons) | ||

| Washington | Varies | ||

| West Virginia | |||

| Wisconsin | 3.05% for new employers with payroll < $500,000 3.25% for new employers with payroll > $500,000 | 0.05% – 12.0% | $14,000 |

| Wyoming | Varies | Maximum rate of 8.5% | $33,800 |

For some states, this SUTA tax rate includes other taxes. Contact your state for more information on included and additional assessments.

For more state-specific information, use our New Employer Information by State for Payroll page.

How to pay unemployment tax to your state

You must report your SUTA tax liability to your state and make payments. Generally, you need to make quarterly payments. Use your employer account number to report and deposit your SUTA tax liability.

Contact your state for more information about reporting and depositing SUTA tax.

Let Patriot’s payroll services handle your payroll calculations, tax filings, and deposits. We’ll deposit your payroll taxes and file the appropriate forms with federal, state, and local agencies. Get started with a free trial!

This article has been updated from its original publication date of July 16, 2018.

This is not intended as legal advice; for more information, please click here.