Hired your first employee? Check. Set a start date? Check. Ready to process payroll? Not quite yet. Before you can start paying your employees, there are a few steps you need to know and some terms to learn. This handy payroll 101 guide explains how to set up payroll the right way so you can breathe easier and get back to business.

- Register required employer accounts and gather employee tax, benefits, and bank information before running payroll, and complete I-9 and state new hire reporting.

- Classify workers correctly (W-2 employee vs. 1099 contractor), determine exempt vs. nonexempt status, set wages, pay frequency, and payment method.

- Calculate wages, withhold and deposit payroll taxes, file required forms, issue Form W-2 annually, and provide pay stubs where required.

- Decide how you’ll run payroll (manual, software, or full-service), set direct deposit lead times (typically 2–4 business days), and consider opening a separate payroll bank account.

- Keep payroll records for at least 3 years and tax records for at least 4 years.

Quick-start payroll checklist (8 steps)

- Get your EIN and any required state/local tax IDs.

- Verify worker status (employee vs. contractor) and determine FLSA exempt/nonexempt status for employees.

- Register for EFTPS, state unemployment, and new-hire reporting; secure workers’ compensation coverage.

- Collect employee paperwork: Form W-4, Form I-9, direct deposit authorization (if applicable), and benefits

elections. - Choose a pay schedule (e.g., biweekly) and payment method (e.g., direct deposit, pay card).

- Pick a payroll method (manual, software, or full service) and set up company/employee profiles; consider a dedicated payroll bank account.

- Track time, run payroll, review results, pay employees, and provide pay stubs.

- Deposit and file payroll taxes on time (Forms 941/944, 940), and send year-end forms (W-2/W-3, 1099-NEC).

Before you run payroll

Before running your first payroll, you have some preparation to do. Luckily, most of the tasks are ones you only have to do once.

Gathering payroll information

You need to gather some payroll information and register for accounts before running payroll. Each of these accounts is required to run payroll and pay taxes. Here are some things you need to register for:

- Employer Identification Number (EIN)

- Electronic Federal Tax Payment System (EFTPS) account

- State tax accounts (e.g., state unemployment insurance)

- New hire reporting account from the state

- Workers’ compensation coverage

This is not an all-inclusive list. Your state may require you to register for additional payroll-related accounts. Contact your state for more information.

In addition, plan for:

- Any required local tax IDs (city/county) if applicable.

- A dedicated payroll bank account to separate payroll funds and simplify reconciliation.

- Required workplace labor law posters (federal and state).

- Pay stub delivery method (paper or electronic) required by your state.

After you gather all your employer information, you also need to get paperwork and details from your employee to run payroll.

Each employee must fill out Form W-4, Employee’s Withholding Certificate. On the form, the employee enters information that affects how much federal income tax you withhold from their wages. Depending on where your business is located, your employee might also need to fill out a state withholding form.

Also complete Form I-9, Employment Eligibility Verification, within three business days of the

employee’s start date and keep it on file (do not submit it to a government agency). If using direct deposit, collect a direct deposit authorization and the employee’s bank details.

If you offer small business employee benefits, you need the benefits election information for each employee. You need to know how much you must withhold for the benefits and whether the deductions are pre-tax vs. post-tax.

Making payroll decisions

Have all of your employer and employee information sorted out? Good. Now that you know your employer accounts and employee withholding details, it’s time to make a few other payroll decisions.

Employee vs. independent contractor

Before anything else, decide whether each worker is a W-2 employee or a 1099 independent contractor. Employees are on payroll (you withhold/cover payroll taxes and provide W-2s). Contractors are not on payroll (no tax withholding; you may issue Form 1099-NEC if you pay $600+). Misclassification can trigger back taxes and penalties. When in doubt, review IRS guidelines or consult a professional.

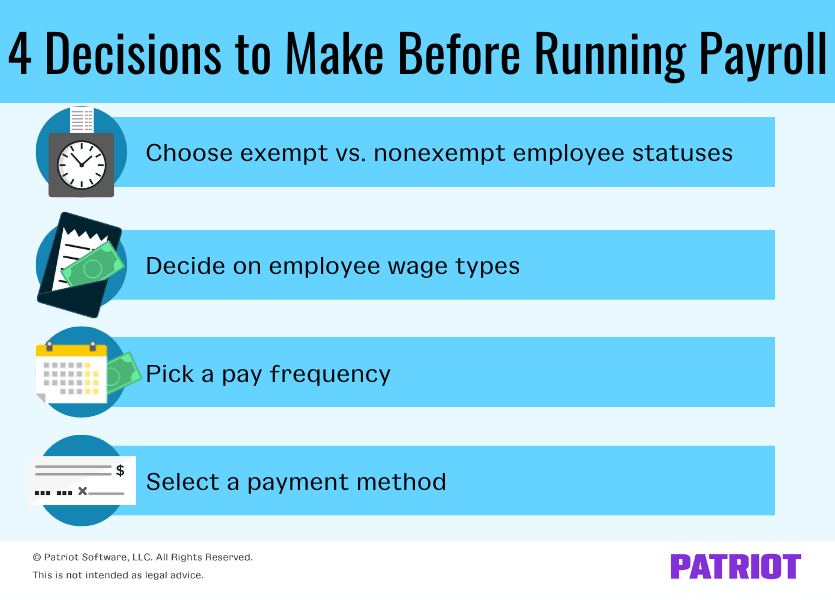

Exempt vs. nonexempt

First, determine if an employee is exempt vs. nonexempt from overtime wages. To be exempt under federal guidelines, an employee must fall under one of the following exemptions:

- Executive, administrative, or professional exemption

- Computer exemption

- Outside sales exemption

- Highly compensated employee exemption

If the employee does not meet one of the above exemption types, the employee is generally nonexempt, and you must pay the employee overtime wages for overtime hours worked. Some states require stricter criteria than the federal government. Check with your state for more information.

Employee wages

After determining if an employee is exempt or nonexempt, decide if you will pay an employee a salary vs. hourly wages. If your employee is exempt, you must pay the employee a salary. But if your employee is nonexempt, you can choose whether you pay a salary or an hourly wage.

Also, decide if your employee will earn other wages, such as tips or commissions.

Pay frequency

Pick a pay frequency. The pay frequency determines your payroll cutoff and how often you pay your employee. Common frequencies include weekly, biweekly, semimonthly, and monthly.

Again, your state may have more information about how often you must pay employees. Learn the pay frequency by state rules or check with your state directly.

Payment method

Do you know how you will pay your employees and how often? Now it’s time to select how you will give the employee their paychecks.

You can pay your employee with a written or printed check, direct deposit, cash, or payroll card. If you use direct deposit, you will need extra information to complete your payroll, such as your business’s bank account number and routing number. If you decide to use direct deposit to pay your employees, collect their banking information, too.

Keep in mind:

- Direct deposit typically requires running payroll 2–4 business days before payday.

- If you use pay cards, confirm fee disclosures and state rules.

- Some states require providing pay stubs with specific details (e.g., hours, rates, deductions).]

Setting up a payroll system for small business

Once you get all the necessary information and make your payroll decisions, it’s time to start setting up payroll. When setting up payroll for your new business, you can either hire an employee or accountant, do payroll by hand, or use payroll software for startups. Payroll software can reduce payroll costs compared to hiring someone. And, software is less exhaustive than doing payroll by hand. When choosing a payroll system, make sure to compare costs, features (like payroll automation), and support. You can use payroll analytics to monitor your expenses throughout the year.

Consider opening a dedicated payroll bank account to isolate payroll funds and simplify tax deposits

and reconciliations.

With Patriot, you can choose Basic Payroll (you run payroll and handle tax filings) or Full Service Payroll (we calculate, file, and deposit federal, state, and local payroll taxes for you).

Add all your payroll information (e.g., employee withholding and payment info) to whatever system you use. That way, you are prepared the first time you need to run payroll.

After completing how to set up payroll for small business, you are ready to run payroll.

Once you understand payroll setup, explore our best payroll software for small businesses comparison to choose software that simplifies your process.

- Enter employee hours

- Review payroll entries and approve

- Pay your employees

Running payroll 101

When you reach the end of a pay period, it’s time to run payroll. How you run payroll depends on what payroll method you use. Despite the differences, there are generally three steps of running payroll.

How to run payroll

- Gather information, enter hours, and make calculations

First, gather and calculate hours worked. You need to know how many hours your employee worked during the pay period. Consider using time and attendance software for small business to help with employee attendance management.

You also need to know your employee’s hourly wage or pay period salary. Using that information, calculate the employee’s earnings. Ensure you include overtime wages and any other earnings (e.g., commission).

Under federal law, overtime for nonexempt employees is generally 1.5x the regular rate for hours over 40 in a workweek. Some states have daily overtime or different thresholds; check your state rules.

After calculating the employee’s gross wages earned, subtract taxes and other deductions ( we’ll get to that later).

If you use payroll software, the software will automatically calculate your employee’s wages and withholdings. - Approve payroll

When the calculations are done, double-check the results for accuracy. This step is easy to skip over, but you shouldn’t.

If you do manual payroll calculations, make sure you did the math correctly. If you use payroll software, check to make sure you entered the numbers correctly (e.g., 40 hours instead of 400).

When you are approving payroll, look over the paycheck totals. The net pay and the withholdings should be the same or similar to previous paychecks.

Check to ensure that all withholdings are deducted from the employee’s paycheck before approving payroll.

If you pay by direct deposit, run payroll far enough in advance (often 2–4 business days before payday) for ACH processing. - Pay your employee

After you approve payroll, you need to get the wages to your employee. Use the payment method you chose earlier to distribute the wages (e.g., direct deposit).

Provide a pay stub with required details where mandated by state law.

Payroll taxes

As an employer, you must withhold and contribute to employment taxes. The main taxes you need to know about include:

- Social Security and Medicare taxes

- Federal, state, and local income taxes

- Federal and state unemployment taxes

Each tax has its own rate and rules. Check them out in the chart below:

| Tax | Tax Rate | Wage Cap | Who Pays? |

|---|---|---|---|

| Social Security Tax | 6.2% (Employee) 6.2% (Employer) | $184,500 (2026) | Employee Employer |

| Medicare Tax | 1.45% (Employee) 0.9% (Additional Medicare tax, employee only) 1.45% (Employer) | No wage cap (Additional Medicare tax withholding starts at: $200,000) | Employee Employer (Only the employee owes additional Medicare tax) |

| Federal Income Tax | Varies based on employee’s income and withholding adjustments | No wage cap | Employee |

| State and Local Income Tax | Varies by state and locality (Does not apply to all states and localities) | No wage cap | Employee |

| Federal Unemployment Tax (FUTA tax) | 6% (0.6% with tax credit) | $7,000 | Employer |

| State Unemployment Tax/Insurance (SUTA tax) | Varies by state | Varies | Employer In some states, both employee and employer |

Note: Tax rates and wage bases can change annually. Verify current figures with the IRS and your state

before each new tax year.

In some years, FUTA credit reduction states may increase your effective FUTA rate; check the IRS list

annually.

After you withhold the taxes, you have to deposit them on a regular basis. There are also forms you need to fill out as an employer. Here is what you need to know about depositing and filing payroll taxes:

| Tax | Deposit Frequency | How to Deposit | Form to File | Filing deadline |

|---|---|---|---|---|

| Social Security, Medicare, and Federal Income Tax | Monthly or semiweekly (Depends on a lookback period) | Electronic funds transfer using EFTPS, a tax professional, or a payroll tax filing service | Form 941 (Quarterly) OR Form 944 (Annual), if applicable | Quarterly: April 30 July 31 October 31 January 31 Annually: January 31 |

| State and Local Income Tax | Varies | Varies | Varies | Varies |

| Federal Unemployment Tax (FUTA tax) | Quarterly, due on: April 30 July 31 October 31 January 31 | EFTPS, a tax professional, or a payroll service | Form 940 | January 31 |

| State Unemployment Tax/Insurance (SUTA tax) | Varies | Varies | Varies | Varies |

Check the IRS website and your state tax website for more information about employment taxes.

New employers are often monthly depositors for federal income tax and FICA until their lookback

history is established.

Recordkeeping and compliance essentials

- Keep payroll records for at least 3 years and employment tax records for at least 4 years.

- Retain I-9s for 3 years after hire or 1 year after termination, whichever is later.

- Display required federal and state labor law posters.

- Report new hires to your state (timelines vary; commonly within 20 days or sooner).

- Maintain signed direct deposit authorizations and benefits deduction authorizations.

- Store records securely and limit access to sensitive employee data.

Form W-2

At the end of every year, you must send Form W-2, Wage and Tax Statement, to your employees and the federal and state governments. Form W-2 summarizes what you paid your employee during the year. The form also lists how much you withheld for each tax.

You must send Form W-2 to the employee, the Social Security Administration (SSA), and your state government (if required) by January 31 each year. Also, send Form W-3, Transmittal of Wage and Tax Statement, with the copy of Form W-2 you send to the SSA.

If you paid independent contractors $600 or more, send Form 1099-NEC to recipients and file with the IRS by January 31 (Form 1096 is required if filing by paper).

FAQs

EIN, EFTPS, state tax accounts (including unemployment), workers’ comp, employee W-4, Form I-9, direct deposit authorization (if used), and benefits elections. Some locations require local tax IDs.

Sole proprietors and most single-member LLC owners generally do not run payroll for themselves. S corporation owners who perform services typically must take reasonable wages via payroll.

Common schedules are biweekly or semimonthly. Your state may set minimum pay frequency rules; pick a schedule that meets cash flow needs and compliance requirements.

Typically 2–4 business days before payday. Your payroll provider will specify cutoff times.

Exempt employees (meeting specific duties and salary tests) are not owed overtime. Nonexempt employees are generally owed 1.5x for hours over 40 in a workweek (state rules may vary).

It’s not required, but a separate payroll bank account helps segregate funds, simplify reconciliations, and reduce errors.

You could owe back taxes, penalties, and interest. Use IRS guidelines or seek advice if unsure.

Yes! Full-service providers (like Patriot’s Full Service Payroll) calculate, file, and deposit taxes on your behalf; basic software helps you run payroll while you handle filings.

This article has been updated from its original publication date of March 13, 2017.

This is not intended as legal advice; for more information, please click here.