Do your employees use company-owned or leased vehicles for personal reasons? If so, you need to know how to handle reporting personal use of company car for wage and tax purposes.

Read on to learn:

- What is personal use of company car?

- How to calculate personal use of company vehicle value

- How to report personal use of company car and handle taxes

- Personal use of company vehicles is taxable noncash fringe benefit; include its fair market value in employee income and withhold taxes.

- Use valuation methods (general, cents-per-mile, commuting, lease value) to calculate personal use value and exclude working condition benefits.

- Report and withhold properly: include PUCC on Form 941/944 and W-2; keep detailed mileage records and follow withholding options and deadlines.

What is personal use of company car?

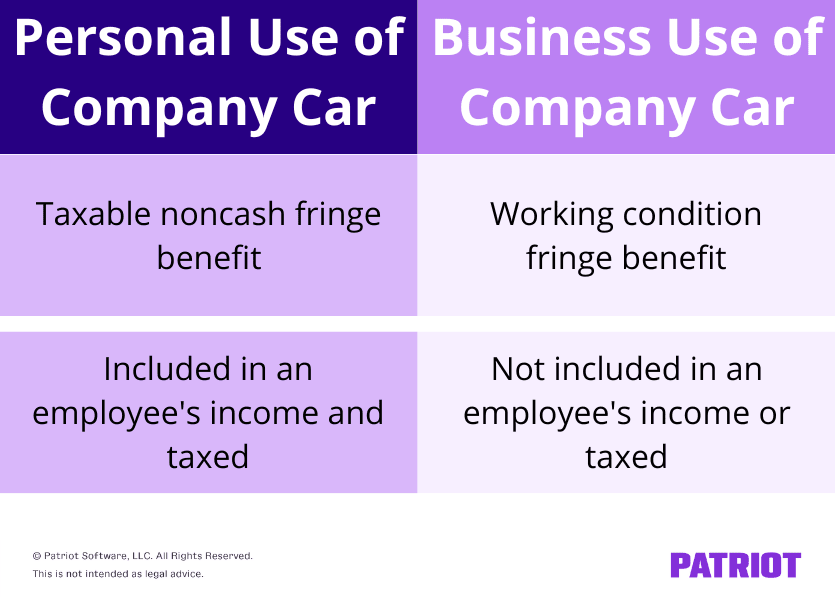

Personal use of a company car (PUCC) is when an employee uses a company vehicle for personal reasons. Driving a company vehicle for personal use is a taxable noncash fringe benefit (aka benefit you provide in addition to wages). As a result, you generally must include the value of using the vehicle for personal reasons in the employee’s income and withhold taxes.

If the employee uses the company car strictly for business purposes, treat the usage differently. Business use of a company car is considered a working condition fringe benefit. A working condition fringe benefit means the value of using the vehicle isn’t included in the employee’s income or taxed because the employee needs it to perform their job.

So, what’s considered personal use of a company car? PUCC includes:

- Commuting to and from work

- Running a personal errand

- Vacation or weekend use

- Use by a spouse or dependent

If an employee does use a company car for one of the above purposes, determine its value and include it in the employee’s compensation for tax purposes.

Exceptions

In some cases, an employee’s personal use of a company car is exempt from inclusion in wages and taxes.

Exceptions include:

- De minimis fringe benefits

- Qualified nonpersonal use vehicle

- Demonstration vehicles

De minimis fringe benefits

De minimis means too small for consideration. If an employee’s PUCC is so small that it would be unreasonable or administratively impracticable (e.g., infrequent and brief side trips) to track, you can exclude it.

Qualified nonpersonal use vehicle

If a company vehicle has a special design that makes personal use unlikely, exclude personal use from employee wages.

Qualified nonpersonal use vehicles include:

- Marked police, fire, and public safety officer vehicles

- Unmarked vehicles used by law enforcement officers, if the use is officially authorized

- Ambulances

- Hearses

- Delivery trucks with only a driver’s seat, or the driver plus a folding jump seat

- Moving vans

- School buses

- Passenger buses seating at least 20 people

- Animal control vehicles

- Construction or specially designed work vehicles (e.g., dump trucks, cement mixers, forklifts, garbage trucks)

- Refrigerated trucks

- Qualified utility repair vehicles

- Trucks with a loaded weight over 14,000 pounds

- Tractors and other special-purpose farm vehicles

You can get more information about the qualified nonpersonal use vehicle exception in Publication 15-B.

Demonstration vehicles

Do not include personal use of a demonstration vehicle if the employee is a full-time automobile salesperson or sales manager within the sales area of the dealership.

To qualify for this exception, you must substantially restrict the employee’s PUCC:

- No one else can use the vehicle

- The employee cannot take vacation trips in it

- There is no storage of personal items

Personal use is limited to the greater of either a 75-mile radius of the dealership or the employee’s actual commuting distance.

You can get more information about the personal use exemption for demonstration vehicles in Publication 15-B.

How to calculate personal use of company vehicle value

So, how exactly do you calculate the value of an employee’s personal use of a company car? You can use one of the following methods to determine the value of PUCC:

- General valuation rule

- Cents-per-mile rule

- Commuting rule

- Lease value rule

The general valuation rule is the most commonly used method for determining the value of fringe benefits. However, you can use one of the special valuation rules (cents-per-mile, commuting, or leave value) for determining PUCC value.

Remember not to include the working condition benefit in the PUCC value. Again, working condition benefit is the vehicle use that the employee uses for business reasons.

You can learn more about each of these rules in IRS Publication 15-B.

General valuation rule

Under the general valuation rule, calculate the value of PUCC using the fair market value (FMV).

The PUCC’s fair market value is the price the employee would pay a third party to buy or lease the benefit in the same geographic area and under the same or comparable terms.

Cents-per-mile rule

Under the vehicle cents-per-mile rule, determine the employee use of company vehicle value by using the standard mileage reimbursement rate.

To find an employee’s PUCC value under the cents-per-mile rule, multiply their personal miles driven by the IRS standard mileage rate.

For 2026, the standard mileage rate is 72.5 cents per business mile drive. The rate includes the costs of maintenance, insurance, and fuel.

To use this rule, you must meet the following conditions:

- You expect the employee to regularly use the vehicle for business throughout the year

- At least 50% of the total mileage each year must be for business

- The vehicle is generally used each workday to transport at least three employees to and from work, in an employer-sponsored commuting pool

- Employees meet the mileage test

- The vehicle is driven by employees at least 10,000 miles per year (business and personal combined)

- The vehicle is primarily used by employees

You cannot use the cents-per-mile rule for a vehicle if its value on the first day of use exceeds an amount set by the IRS. These values change every year.

If you use the cents-per-mile rule for a vehicle, you must use the rule for all following years. However, you can use the commuting rule if the vehicle qualifies. And if the vehicle no longer qualifies for the cents-per-mile rule, you can use another rule.

Commuting rule

Does an employee use a company vehicle to commute to and from work? If so, you might opt for using the commuting valuation rule.

Under the commuting rule, the PUCC value is $1.50 for a one-way commute, per employee. You can use this rule if you:

- Provide the vehicle to the employee for use in your business and require them to commute in it for non-compensatory business reasons

- Establish a written policy that prevents the employee from using the vehicle for other personal reasons other than de minimis personal use

- Ensure the employee using an automobile for commuting isn’t a control employee. A control employee is a:

- Corporate officer earning at least $145,000 in 2026

- Director

- Worker whose pay is $290,000 or more in 2026

- Worker who owns a 1% or more equity, capital, or profits interest in your business

- Highly compensated employee (5% owner at any time during the previous year or received more than $160,000 in pay for the preceding year)

Special note: There is also an unsafe conditions commuting rule that you might be able to use. Like the regular commuting rule, the value is $1.50 for a one-way commute. The unsafe conditions commuting rule applies if the employee would ordinarily walk or use public transportation and you only allow the employee to use the vehicle for commuting. For more information, see IRS Publication 15-B.

Lease value rule

Under the lease value rule, determine the PUCC value by finding the vehicle’s annual lease value. Exclude any amount the employee uses for business purposes. So, you would multiply the annual lease value by the percentage of personal miles (out of total miles) driven.

To use the lease value rule, follow these steps:

- Determine the value of the vehicle on the first day you made it available to any employee for personal use

- Find the annual lease amount on the Annual Lease Value Table in Publication 15-B. Reference the fair market value on the left. Use the corresponding annual lease on the right

- Calculate the employee’s percentage of personal miles driven by dividing the employee’s personal miles driven by total miles driven

- Calculate the FMV of the employee’s personal use by multiplying the annual lease value (Step 2) by the percentage of personal miles driven (Step 3)

If you provide fuel to the employee, add 5.5¢ per personal use mile.

See it in action: Let’s say you have an employee who drove 30,000 total miles, of which 5,000 are personal miles. The FMV of the vehicle is $17,500. Using the Annual Lease Value Table, you find that its lease value is $4,850. The employee’s percentage of personal miles is 17% (5,000 / 30,000). So, the employee’s PUCC value is $824.50 ($4,850 X 0.17).

How to handle taxes and reporting

When withholding and reporting taxes for personal use of a company vehicle, follow the rules for withholding from and reporting on non-cash fringe benefits.

Pro tip: Have employees keep detailed records, such as mileage, business purpose, and time and place of travel. That way, you have the records to back up wage and tax reporting.

- Run payroll in 3 steps

- Easily add PUCC as a money type in your account

- Enjoy free USA-based support

“Paying” the benefit

When an employee uses a company vehicle for personal use, they immediately get that benefit. But, using the benefit and being paid for it are different.

You may treat the benefit as being paid on a pay period, monthly, quarterly, semiannual, annual, or another basis. This is when you include the fair market value in the employee’s wages. You must pay the employee for the benefit at least annually.

You can change the payment period at any time. The fair market value for all personal use benefits in a calendar year must be recorded by December 31 of that year.

Keep in mind that you don’t have to use the same payment schedule for all employees. You might use a monthly basis for one employee but a quarterly basis for another.

Also, you don’t have to tell employees or the IRS about the frequency you choose to include the benefit value in employee wages.

Let’s say you include the benefit value semiannually in employee wages. An employee uses a company vehicle for personal use during the first half of the year. But you don’t include the benefit value in the employee’s wages until the very end of the first half of the year. This is when you consider the benefit “paid” to the employee.

If you want until the end of the year to include the entire benefit amount in the employee’s wages, the employee might not have enough wages to cover the taxes. If this happens, you are liable for uncollected Social Security and Medicare taxes, in addition to your own share.

Special accounting rule

There is a special accounting rule that can help with paying and reporting benefits.

You can treat benefits provided in November and December (or a shorter period during those two months) as being paid during the next year. This gives you extra time to value the personal use of a company vehicle.

There are some restrictions:

- This only applies to benefits provided in November and December, not all the benefits you treat as paid during these months. For example, you can’t roll over personal use of a vehicle that occurred in July.

- You must notify your employees that you are using this special accounting rule. You have the time between the last paycheck of the calendar year and when employees receive their Forms W-2 to tell them.

- If you use the special accounting rule for one employee’s personal use of a vehicle, you must use the rule for all employees. But, you don’t have to use the rule for other fringe benefits.

- You must use the same ending date in November and December for all employees. But, you don’t have to use the same ending date for all fringe benefits.

- If you use the special accounting rule, your employees must use the special accounting rule on their tax returns.

If you choose to use the special accounting rule, benefits shifted to the next year must use the valuation rules for the next year. For example, if the cents-per-mile rate increases, you need to use the new cents-per-mile rate when calculating the value of the benefits.

Withholding taxes

There are two methods for withholding:

- You can add the fair market value of the employee’s personal use to their wages. Calculate withholdings on the total wages as you normally would.

- Treat the amount as supplemental wages. Withhold federal income tax on the amount at the applicable supplemental flat tax rate of 22%. You might also have to pay a state supplemental rate. Withhold FICA (Social Security and Medicare) tax as normal.

With either method, subtract the benefit amount from the employee’s wages after you calculate the withholdings. If you don’t subtract the benefit amount, you’d essentially be paying the employee twice for the vehicle use. The employee would receive the value of the benefit when they use the vehicle, and they’d receive the value again in their wages. It’s important to subtract the benefit amount so you don’t give the benefit value twice.

You can choose not to withhold federal income tax on an employee’s personal use of an employer-provided vehicle. You can also choose to withhold federal income tax for some employees’ personal use, but not for others.

If you decide not to withhold federal income tax, notify affected employees in writing by January 31 of the year you make your decision, or within 30 days after the employee first gets the vehicle, whichever is later. If you change your mind about withholding, you must notify employees in writing again.

Even if you don’t withhold federal income tax, you must still withhold FICA tax. Deposit the taxes according to deposit rules and your frequencies.

Reporting

Report the value of personal use of a company vehicle on Form 941 and the employee’s Form W-2.

PUCC on Form 941 (or 944)

You use Form 941 (or Form 944) to report employee wages, federal income tax withholding, and withholdings and contributions for FICA taxes. Form 941 is a quarterly form, and Form 944 is an annual form.

Report the fair market value of an employee’s personal use on Form 941 in the quarter it is considered paid. You must report the fair market value of the benefit for a year no later than the fourth quarter Form 941 for that year.

Use Form 944 instead of Form 941? Report the fair market value of an employee’s PUCC on Form 944.

PUCC on W-2 form

Report the value of the personal use of the company vehicle on the employee’s Form W-2. Include the amounts in Boxes 1, 3, and 5. Also, report the amounts you withheld in Boxes 2, 4, and 6.

If you choose not to withhold federal income tax, you must still include the fair market value of the benefit in Box 1.

If you treat all employee use of a vehicle as personal use, include the total benefit amount in Boxes 1, 3, and 5. Also, report the benefit amount in Box 14 or a separate statement to the employee.

This article has been updated from its original publication date of December 29, 2017.

This is not intended as legal advice; for more information, please click here.