Employers, this one’s for you. After withholding payroll taxes from your employees’ wages (and contributing the employer share), you need to deposit the taxes with the IRS. But that’s not all. You must also report the taxes on either Form 944 or 941. So, what’s the difference between Form 944 vs. 941?

Read on to learn the difference between the two forms so you can use the correct one for your business.

But first … a word about payroll taxes

When you have employees, you are responsible for all things payroll, including taxes. Your federal tax responsibilities include:

- Federal income tax (withholding)

- Social Security tax (withholding and contributing)

- Medicare tax (withholding and contributing)

- Federal unemployment tax (contributing)

Keep in mind that there are also a number of state and local taxes you may be responsible for (e.g., state and local income taxes).

After withholding and contributing federal taxes, you must report them to the IRS.

Use Form 940, Employer’s Annual Federal Unemployment (FUTA) Tax Return to report federal unemployment tax. For federal income, Social Security, and Medicare taxes, use Form 944 or 941.

Form 944 vs. 941

Forms 941 and 944 are the two forms that employers use to report employee wage and payroll tax information to the IRS. Employers who use Form 941, Employer’s Quarterly Federal Tax Return, report wages and taxes four times per year. Employers who use Form 944, Employer’s Annual Federal Tax Return, report wages and taxes once per year.

Do not file both forms. You must use either Form 941 or 944. However, you do not get to choose between using Form 941 or 944. The IRS decides which form you must use to report wage and tax information.

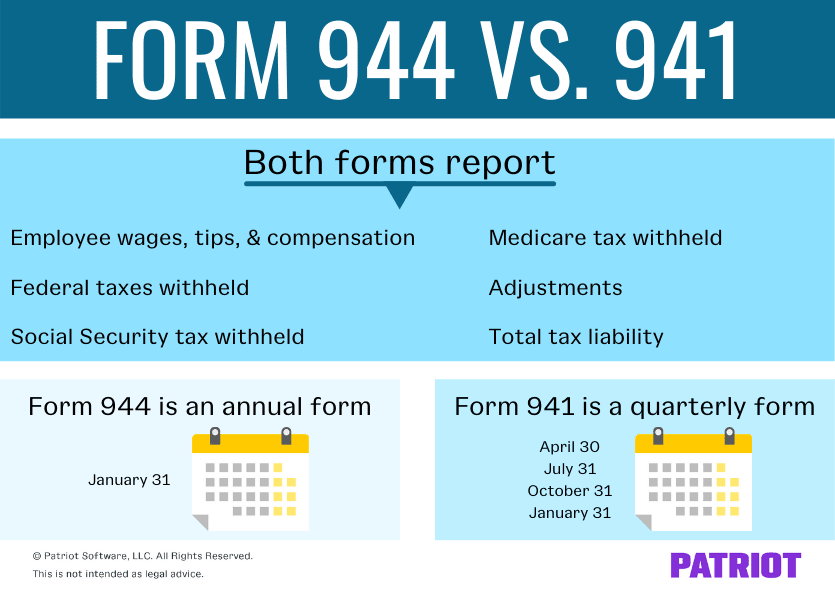

Both Forms 944 and 941 ask for the same main information. The difference boils down to how often you need to report it (i.e., quarterly or annually).

Here is some of the information you must report on both forms:

- Employer information (e.g., Employer Identification Number, name, and address)

- Wages, tips, and compensation you paid employees

- Federal income tax withheld

- Social Security tax withheld

- Medicare tax withheld

- Adjustments

- Total tax liability

Because of emergency COVID-19 relief measures, 2020 and 2021 Forms 941 and 944 also have areas for employers to report:

- Paid sick leave wages

- Paid family leave wages

- Social Security tax deferrals (employer and/or employee shares)

- Employee Retention Credit wages

Now that you know some of the similarities between the forms, it’s time to dive into the difference between 941 and 944.

Form 941

Most employers use Form 941 for reporting. Again, this is the form employers use to report wage and tax information quarterly.

File Form 941 if you have employees and the IRS does not tell you to file Form 944.

Send Form 941 to the IRS even if you don’t have taxes to report (simply enter 0 on the lines). Do not send Form 941 to the IRS if you filed a final return, are a seasonal employer, or handle farm or household employee payroll.

Form 944

Some employers can use Form 944 for wage and tax reporting. Again, this is the form employers use to report this information annually. Use this if the IRS tells you to; otherwise, use Form 941.

Only the smallest employers can file Form 944. This includes employers with an annual liability of $1,000 or less for Social Security, Medicare, and federal income taxes.

If you are a new employer, you may be able to request to file Form 944 when applying for your Employer Identification Number (EIN). Indicate if you expect your employment tax liability to be $1,000 or less on your EIN application form.

Submit Form 944 to the IRS even if you don’t have taxes to report (enter 0 on the lines). Do not send Form 944 to the IRS if you filed a final return.

What can you do if the IRS didn’t tell you to file Form 944 but you think you qualify? You can request to file Form 944. Either call the IRS at (800-829-4933) or send a written request. If the IRS accepts your request, they will contact you.

Want to file Form 941 instead? If the IRS tells you to file Form 944, you can request to file Form 941.

941 vs. 944 filing requirements

You might be wondering what the difference between 941 and 944 is when it comes to the filing process. IRS Form 944 vs. 941 filing requirements include:

- How to file

- Due dates

- Payments

- What to do if you make a mistake

How to file Forms 941 and 944

You can e-File or mail Forms 941 and 944. The IRS encourages electronic filing.

You can e-File using the IRS’s e-Filing system, either by submitting the forms yourself or having a tax professional file on your behalf.

If you decide to mail Form 941 or 944, where you send it depends on two factors:

- What state your business is in

- Whether you’re sending the form with or without payment

You can view the mailing addresses in the Instructions for Form 944 and the Instructions for Form 941.

If you opt for full-service payroll software, like Patriot, your provider files Form 941 or 944 on your behalf.

IRS Form 944 vs. 941: Due dates

To avoid penalties, accurately report employee wage and tax information on either Form 944 or Form 941 by their due dates. So, when are Forms 944 and 941 due?

Submit Form 941 to the IRS by:

- April 30 (Quarter 1)

- July 31 (Quarter 2)

- October 31 (Quarter 3)

- January 31 (Quarter 4)

Submit Form 944 to the IRS by:

- January 31 (Quarters 1 – 4)

If the due date falls on a weekend or holiday, your employer tax return is due the following business day.

Payments

You can pay your Forms 941 or 944 tax liability with an electronic funds transfer. But, when do you make payments?

Form 941

If you’re a Form 941 filer, pay your tax liability either monthly or semiweekly. Your deposit schedule depends on your tax liability during a four-quarter IRS lookback period.

You are a monthly depositor if you reported $50,000 or less in taxes during the lookback period. Monthly deposits are due:

- On the 15th day of the following month after running payroll

You are a semiweekly depositor if you reported more than $50,000 in taxes during the lookback period. Semiweekly deposits are due:

- The following Wednesday after running payroll (if payday falls on Wednesday, Thursday, or Friday)

- The following Friday after running payroll (if payday falls on Saturday, Sunday, Monday, or Tuesday)

Form 944

Although you can only file Form 944 if you owe $1,000 or less annually in employment taxes, you might go over. This impacts when the money is due.

When you owe your tax liability depends on the amount:

- Less than $2,500 annually: Pay your tax liability when you file your return

- $2,500 or more for the year (but less than $2,500 for the quarter): Deposit by the last day of the month after the end of a quarter

- $2,500 or more for the quarter: Deposit monthly or semiweekly, depending on your deposit schedule

What to do if you make a mistake

Mistakes happen, even on government forms. If you realize you made a mistake on Form 941 or 944, use the form’s corrected version.

File Form 941-X, Adjusted Employer’s Quarterly Federal Tax Return or Claim for Refund, to correct mistakes on Form 941.

File Form 944-X, Adjusted Employer’s Annual Federal Tax Return or Claim for Refund, to correct mistakes on Form 944.

Looking for a better way to run payroll and file employment tax returns? With Patriot’s Full Service Payroll, we’ll handle the forms you need to file (and the taxes you owe) on your behalf. You just enter your employees’ work hours and run the payroll. Get your free trial today!

This article has been updated from its original publication date of August 12, 2019.

This is not intended as legal advice; for more information, please click here.