Your to-do list as a business owner seems to get longer every day. There’s one more item you’ll have to check off, and this one is part of federal law. You’re required to retain payroll records, sometimes for up to four years.

Don’t worry. This isn’t an impossible task. This article covers the agencies that require payroll records and how long to keep payroll records.

Quick answer: Keep IRS employment tax records for at least four years, FLSA payroll records for three years (two years for wage computation records), and EEOC personnel records for one year. Follow a longer timeline if state law is longer or a claim or audit is pending.

At-a-glance: How long to keep payroll records

- IRS employment tax records: Keep at least four years after the due date of the tax or the date you paid it, whichever is later.

- FLSA payroll records: Keep three years (e.g., payroll, agreements); wage computation records (e.g., timecards, schedules) keep two years.

- EEOC personnel records: Keep one year; if an employee is involuntarily terminated, keep for one year after termination. If a discrimination charge is filed, keep related records until final disposition.

- States: Follow the longer of federal or state rules (some states require four to five years).

- Form I-9 (not a payroll record but related): Keep three years after the date of hire or one year after termination, whichever is later; store separately from payroll files.

What are payroll records?

Payroll records is a broad term that covers all the documentation you use to track employee hours, salary, and any other information related to how they are paid.

Here are some (but not all) of the records you need to keep track of:

- Names, addresses, and Social Security numbers of all employees

- Workweek information (e.g., start and end dates)

- Hours worked each day/total hours worked each week

- How each employee is paid (e.g., hourly, salary)

- Pay rate

- Overtime earnings (if applicable)

- Additions to or deductions from wages

- Total wages paid each period

- Employee reported tips and allocated tips

- Payment dates and pay periods

- Forms W-2 and W-3

- Forms W-4 and W-5

- Form 941 or 944

- Form 940

- Records of benefits

- Copies of filed returns with confirmation numbers

There’s a chance that there are other payroll records you need to keep, like travel vouchers or receipts for employee reimbursements.

To be clear, payroll records can include records for employment taxes and records showing how you determined employee wages.

How long to keep payroll records

Three federal agencies require you to keep employment payroll records. There’s just one problem: different agencies have different records they want you to keep with different lengths of time for you to keep them.

Read on to see the breakdown.

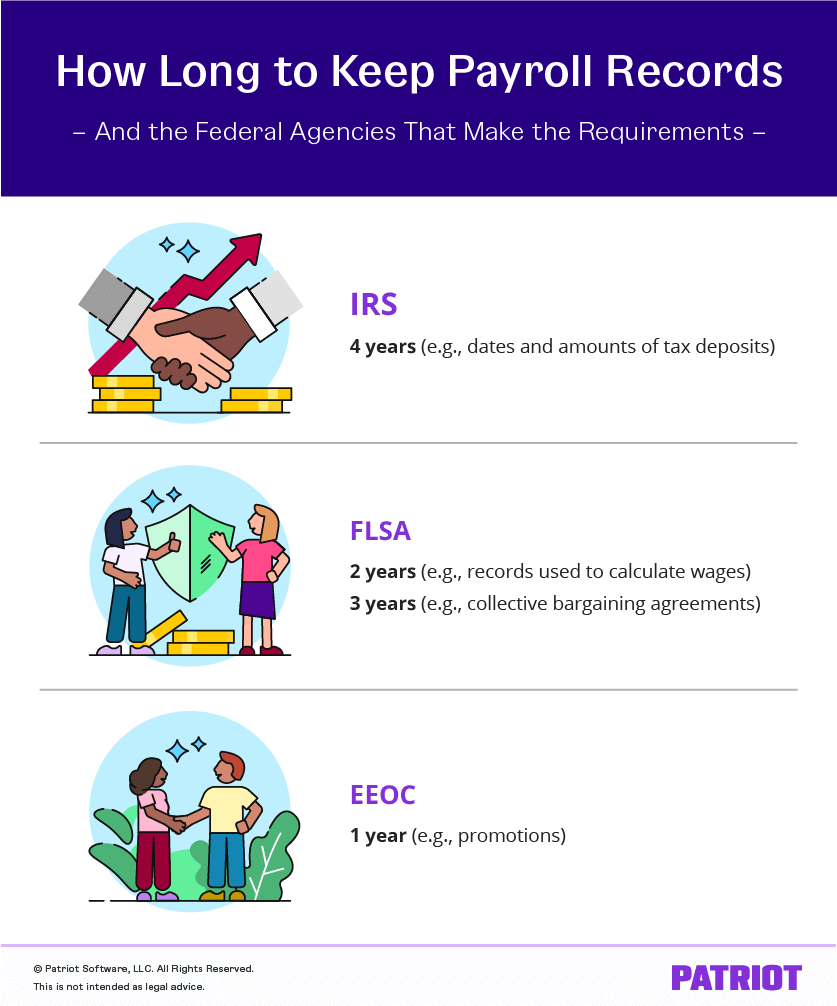

IRS

The IRS requires that you keep payroll records such as amounts and dates of wages, dates of employment, and dates and amounts of tax deposits.

Keep these records for four years after the due date of the tax or the date you paid it, whichever is later. This includes employment taxes like federal income tax withholding, FICA (Social Security and Medicare), and FUTA, plus returns, schedules, and deposit confirmations.

Examples of IRS employment tax records to retain:

- Forms W-4, W-2, and W-3

- Forms 941 or 944 and deposit confirmations

- Form 940 (FUTA) and state unemployment tax filings and credits documentation

- Reported tips, fringe benefits, adjustments/credits, and any correspondence with the IRS

Fair Labor Standards Act

The Fair Labor Standards Act (FLSA) requires that you keep identifying information on each employee as well as information about their hours and pay rate (e.g., employee gender and occupation, total hours worked each workweek and regular hourly pay rates).

Keep records concerning payroll, collective bargaining agreements, as well as sales and purchase records for at least three years. Keep records used to calculate wages for two years.

Wage computation records commonly include timecards or timesheets, work and time schedules, piecework or commission records, and any documentation used to determine straight-time and overtime pay. For exempt employees, the FLSA still requires basic payroll and pay basis records (e.g., salary, workweek, additions/deductions), but it does not require tracking daily and weekly hours. For minors, include date of birth (if under 19) with your records.

Equal Employment Opportunity Commission

The Equal Employment Opportunity Commission(EEOC) requires that you keep detailed employment records (e.g., applications and any records dealing with promotions, demotions, or terminations).

Keep records concerning employment (hiring, promotion, demotion, or termination) for one year after the record was created; if an employee is involuntarily terminated, keep for one year from the date of termination. If someone files a discrimination charge under Title VII, the ADA, or GINA, retain all related records until the final disposition of the charge.

State requirements

Some states may require that you hold on to payroll records a bit longer. For example, California and Arizona require four years, while Montana requires you to keep records for five. New York generally requires employers to retain payroll records and wage statements for up to six years.

To make things a bit more complicated, states might also have different requirements on what type of records you need to keep. Check with your state for specifics.

As a rule of thumb, follow the longer retention period when federal and state rules differ.

- Cloud-based payroll software

- Robust payroll reports

- Free USA-based support

Payroll recordkeeping compliance checklist

Identify which laws apply (IRS, FLSA, EEOC, state, and local).

- Map each record type to a retention period (e.g., payroll vs. wage calculation vs. personnel actions).

- Separate storage for sensitive files (Form I-9, medical, EEO) from payroll.

- Standardize timekeeping for nonexempt employees and record all hours worked.

- Centralize payroll tax returns, deposit confirmations, and agency correspondence.

- Configure role-based access, encryption, and automated backups.

- Maintain an audit trail.

- Determine a schedule for eliminating old records.

- Conduct periodic internal audits to verify completeness and retention windows.

- Keep a calendar of payroll tax due dates and filings (Forms 941, 944, 940, W-2, and W-3).

Special cases and audit-readiness

Terminated employees: Retain records per the applicable agency’s timeline (e.g., IRS four years; EEOC one year after termination if involuntary; FLSA three years for payroll records and two years for wage computations), or longer if a claim, audit, or investigation is pending.

Centralized recordkeeping: If you maintain records offsite or centrally, the Department of Labor can require you to make them available within 72 hours of notice.

Minors and youth employment: Keep required identifying details (including birth date if under 19) and time records consistent with FLSA retention rules. When in doubt, choose the longer retention period (four years or more), especially for tax and wage-related documents.

Storing payroll records

It’s up to you how you store your payroll records. You can use hard copies in locked filing cabinets if you’d like. But, storing payroll records online can help protect them from getting lost or damaged.

Electronic vs. paper: practical tips

Ensure records are accurate, legible, and retrievable for the full retention period.

Protect sensitive data (e.g., SSNs) with role-based access, encryption, and secure backups.

Keep a clear retention schedule and document destruction policy; pause destruction if litigation or an audit is pending.

If you scan paper records, confirm the images are complete and can be reproduced on request.

Payroll solutions offered by Patriot Software

Patriot Payroll® helps you keep compliant, organized records without the manual hassle:

- Secure, cloud-based storage and role-based access to protect sensitive data

- Built-in payroll reports (tax filings, wages, deductions, hours) that align with IRS and FLSA record types

- Exportable filings and deposit confirmations for audit-readiness

- Optional HR add-on to track personnel actions (e.g., promotions, terminations) for EEOC compliance

Get started with Patriot Payroll to simplify recordkeeping, ensure compliance, and reduce risk.

FAQs: Payroll recordkeeping requirements

Keep employee identifiers (name, address, SSN), workweek and hours, pay basis and rates, straight-time and overtime earnings, wage additions/deductions, total wages, pay dates/periods, tips, tax forms (W-4, W-2/W-3), employment tax returns (941/944), deposit confirmations, and benefit records. Include FUTA Form 940 and any IRS and DOL correspondence.

Under FLSA, wage computation records like timesheets and schedules should be kept at least two years. Many employers keep pay stubs and summaries for three to four years to align with other records.

Retain Forms I-9 for three years after the date of hire or one year after termination, whichever is later. Store I-9s separately from payroll files to limit access to sensitive identity documents.

Keep 1099-NEC, payment records, and related tax documentation at least four years for IRS purposes. FLSA timekeeping rules do not apply to independent contractors.

Yes, if your electronic copies are accurate, complete, secure, and remain accessible for the full retention period. Wait to get rid of paper documents if there’s an audit, charge, or litigation hold.

Preserve all related records (pay, personnel, communications) until the charge is fully resolved, even if that extends beyond standard timelines.

Yes. Keep basic payroll information (e.g., name, address, occupation), pay basis, total wages paid, and workweek details for exempt employees, even if you do not track their daily and weekly hours.

Acknowledge promptly, gather requested documents (e.g., payroll journals, timecards, tax returns, deposit confirmations), and ensure availability within required timeframes.

Interested in a better way to handle payroll and HR tasks? Sign up for Patriot Software to get a free trial of our payroll software and HR software add-on today.

This article has been updated from its original publication date of June 1, 2011.

This is not intended as legal advice; for more information, please click here.