Once you send Forms W-2 to your employees, you don’t have to worry about the annual form until next year. Or, do you? If you don’t know how to fill out Form W-2, you may run into problems.

Your employees might come to you with questions about Form W-2. And, your employees may think you made a mistake if their W-2 Box 1 value is lower than what they believe they earned.

Ready to cut through the confusion? Read on to learn how to fill out Form W-2, box by box, and what it all means.

- Accurately report employee identification, wages, and taxes in the correct boxes to avoid errors and employee confusion.

- Understand differences between boxes: Box 1 (federal wages), Box 3 (Social Security wages), and Box 5 (Medicare wages).

- Follow best practices: verify employee info, double-check numbers, use payroll software, file and distribute by January 31.

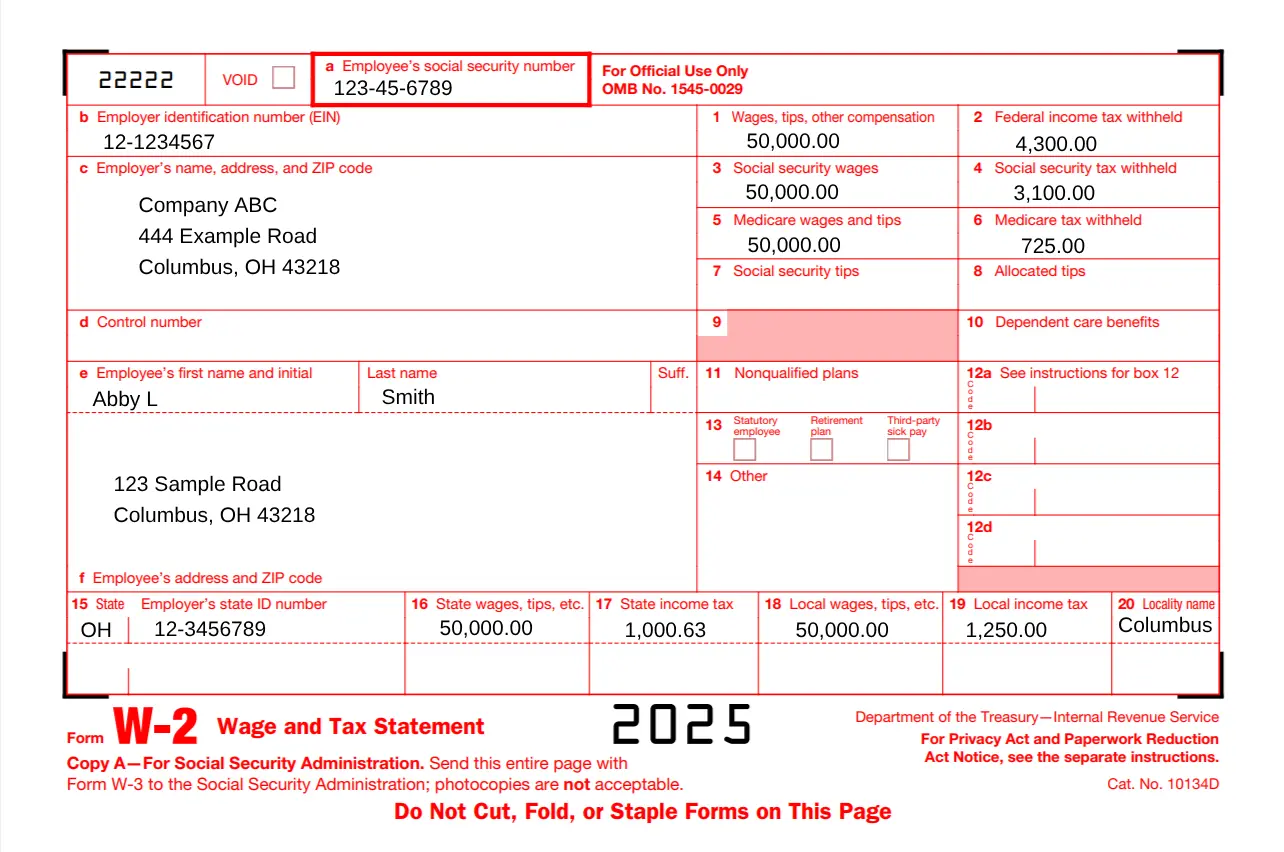

Example Form W-2

Before we dive into how to fill out Form W-2, here’s a simple sample of a Form W-2 for an employee who earns $50,000 annually.

How to fill out Form W-2

You might have your Form W-2 responsibilities down to a science. Input employee information; send copies to employees; file the form with the SSA and state, city, or local tax department; and repeat the following year.

Or, you just might spend hours gathering employee information and trying to decode the Wage and Tax Statement.

Whether you complete Forms W-2 on your own, use payroll software, or have a tax preparer, you should be semi-fluent in knowing how to fill out Form W-2.

As a generalization, Form W-2 boxes show identification, taxable wages, taxes withheld, and benefits information.

Boxes A-F are straightforward. They list identifying information about your business and employee. The numbered boxes, Boxes 1-20, can get a little more tricky.

If you want Form W-2 explained, dive into each box’s purpose below.

W-2 Box A: Employee’s Social Security number

Box A shows your employee’s Social Security number. Social Security numbers are nine digits that are formatted like XXX-XX-XXXX.

If your employee applied for a Social Security card and has not received it, don’t leave the box blank. Instead, write “Applied For” in Box A on the Social Security Administration copy. When the employee receives their SS card, you must issue a corrected W-2.

W-2 Box B: Employer Identification Number (EIN)

Box B shows your Employer Identification Number. EINs are nine-digit numbers structured like XX-XXXXXXX.

The number you enter in Box B is the same on every employee’s Form W-2. The IRS and SSA identify your business through your unique EIN.

Do not use your personal Social Security number on Forms W-2. If you do not have an Employer Identification Number, apply for an EIN before filing Form W-2. Then, mark “Applied For” in Box B.

W-2 Box C: Employer’s name, address, and ZIP code

Box C further identifies your business by listing your company’s name and address. Use your business’s legal address, even if it’s different than where your employees work.

Your employees may wonder whether the address is incorrect if it’s different than their work address. Verify your legal business address and ensure your employee it is accurate.

W-2 Box D: Control number

Box D might be blank, depending on whether your business uses control numbers or not.

A control number identifies Forms W-2 so you can keep records of them internally. If you don’t use control numbers, leave this box blank.

W-2 Boxes E and F: Employee’s name, address, and ZIP code

Box E shows the employee’s first name, middle initial, and last name. Reference the employee’s SSN to enter their name correctly.

Enter the employee’s address in Box F.

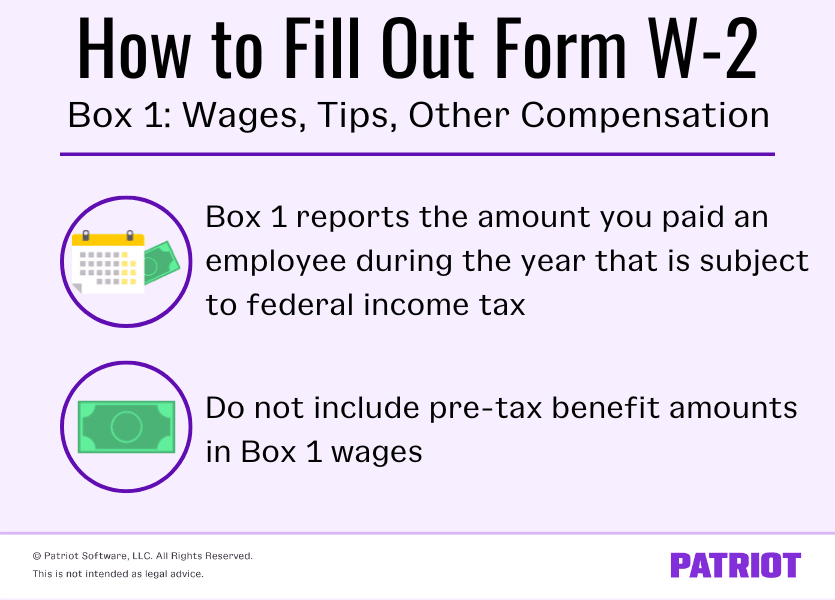

W-2 Box 1: Wages, tips, other compensation

Box 1 reports an employee’s wages, tips, and other compensation. This is the amount you paid the employee during the year that is subject to federal income tax.

Payments not subject to federal income tax include pre-tax retirement plan contributions, health insurance premiums, and commuter benefits.

The wages you report in Box 1 might be higher or lower than other wages on Form W-2. This is not necessarily a mistake.

For example, an employee’s Box 1 wages can be lower than Box 3 wages. Some pre-tax benefits are exempt from federal income tax but not Social Security tax.

W-2 Box 2: Federal income tax withheld

Box 2 shows how much federal income tax you withheld from an employee’s wages and remitted to the IRS.

Federal income tax withholding is based on the employee’s taxable wages and filing status.

If your employee has a question about their refund amount or why they owe taxes, instruct them to Box 2. The IRS compares what the employee paid throughout the year in federal income taxes to their total liability.

W-2 Box 3: Social Security wages

Box 3 shows an employee’s total wages subject to Social Security tax. Do not include the amount of pre-tax deductions that are exempt from Social Security tax in Box 3.

The number in Box 3 should not be higher than the Social Security wage base, which is $176,100 for tax year 2025.

If you must report Social Security tips (Box 7), the total of Boxes 3 and 7 must be less than the Social Security wage base.

W-2 Box 4: Social Security tax withheld

Box 4 reports how much you withheld from an employee’s Social Security wages and tips.

The employee portion of Social Security tax is 6.2% of their wages, up to the SS wage base. Box 4 cannot be more than $10,918.20 ($176,100 X 6.2%) for 2025.

W-2 Box 5: Medicare wages and tips

Enter how much the employee earned in Medicare wages and tips in Box 5.

An employee’s Box 5 value is generally the same as Box 4’s amount. However, there is no Medicare wage base. If the employee earned above the Social Security wage base, the number in Box 5 is higher than Box 3.

For example, the employee earned $180,000. The employee’s Social Security wages, (Box 3) should show $160,200 while Box 5, Medicare wages and tips, displays $180,000.

W-2 Box 6: Medicare tax withheld

Box 6 displays how much you withheld from an employee’s wages for Medicare tax. The employee share of Medicare tax is 1.45% of their wages.

The amount in Box 5 multiplied by the Medicare tax rate should equal Box 6. But if the employee earned above $200,000 (single), their tax liability should be greater.

If you paid an employee above $200,000 (single), you should have also withheld the additional Medicare tax rate of 0.9% from their wages above $200,000.

W-2 Box 7: Social Security tips

If your employee earned tips and reported them, enter the amount in Box 7. Also, include these tip amounts in Boxes 1 and 5.

Again, the total of Boxes 7 and 3 should not be more than $176,100 for 2025.

W-2 Box 8: Allocated tips

Report the tips you allocated to your employee in Box 8, if applicable. Allocated tips are amounts that you designate to tipped employees. Not all employers have to allocate tips to their employees.

Do not include the amount in Box 8 in Boxes 1, 3, 5, or 7. Allocated tips are not included in taxable income on Form W-2. Employees must use Form 4137 to calculate taxes on allocated tips.

W-2 Box 9: (Blank)

Leave Box 9 blank.

W-2 Box 10: Dependent care benefits

Did you give an employee dependent care benefits under a dependent care assistance program? If so, include the total amount in Box 10.

Dependent care benefits under $5,000 are nontaxable. Benefits over $5,000 are taxable. If you gave an employee more than $5,000, report the excess in Boxes 1, 3, and 5.

W-2 Box 11: Nonqualified plans

Box 11 reports employer distributions from a nonqualified deferred compensation plan to an employee.

Include the distribution amounts in Box 1, too.

W-2 Box 12: Codes

There are several W-2 Box 12 codes you may need to put on an employee’s Form W-2. If applicable, add the codes and amounts in Box 12.

These codes and values may lower the employee’s taxable wages.

Let’s say an employee elected to contribute $1,000 to a 401(k) retirement plan. You would write D | 1,000.00 in Box 12.

W-2 Box 13: Checkboxes

Box 13 should not include values. Instead, mark the boxes that apply. There are three boxes within Box 13:

- Statutory employee

- Retirement plan

- Third-party sick pay

For example, if you entered Box 12 code D to show the employee’s retirement contributions, also check the ‘Retirement plan’ box.

W-2 Box 14: Other

Report amounts and descriptions in Box 14 such as vehicle lease payments, state disability insurance taxes withheld, and health insurance premiums deducted.

W-2 Box 15: State | Employer’s state ID number

Like Box B, Box 15 identifies your business’s employer ID number. But, Box 15 is state-specific. Mark your state using the two-letter abbreviation. Then, include your state EIN.

Some states do not require reporting. Leave Box 15 blank if you have no reporting requirement with your state.

Contact your state if you do not have an employer’s state ID number and need one.

W-2 Box 16: State wages, tips, etc.

Box 16 shows an employee’s wages that are subject to state income tax. If the employee works in a state with no state income tax, leave Box 16 blank.

An employee’s Box 16 amount may differ from Box 1. This is not necessarily a mistake. Some wages are exempt from federal income tax and not state income tax.

W-2 Box 17: State income tax

Report how much you withheld for state income tax in Box 17. If you did not withhold state income tax, leave Box 17 blank.

W-2 Box 18: Local wages, tips, etc.

If your employee’s wages are subject to local income tax, include their total taxable wages in Box 18. Leave this box blank if the employee works in a locality with no income tax.

The amount you list in Box 18 might differ from Boxes 1 and 16.

W-2 Box 19: Local income tax

Report any local income tax withheld from the employee’s wages in Box 19. Leave this box blank if it is inapplicable.

W-2 Box 20: Locality name

Box 20 should show the name of the city or locality.

- Electronic or printable W-2s

- Free USA-based support

- Easy onboarding with our setup wizard

Filling out W-2 form best practices

You must know how to fill out Form W-2 if you paid employees during the year. Streamline the process and ensure accuracy by following these best practices:

- Use online payroll to generate Forms W-2

- Verify employee information is correct

- Double-check your numbers

- Give yourself plenty of time

- Send W-2 forms to employees and the SSA by January 31

- Keep copies of Forms W-2 for your records

- Make sure to use the current year’s W-2 form

FAQs

Form W-2 summarizes the total wages an employee receives during the year, along with their federal, state, and local payroll tax withholding.

Social Security wages (Box 3) are the total employee wages subject to Social Security tax.

Employers are responsible for creating W-2s, distributing them to employees, and filing with the appropriate tax agencies (Social Security Administration, plus state and local governments).

Box 1 shows the total wages paid to the employee while Box 3 shows the total wages subject to Social Security tax.

Boxes 1 and 3 may be different because the employee contributed to a retirement plan or an adoption assistance program, or the employee earned above the Social Security wage base.

This article has been updated from its original publication date of February 20, 2019.

This is not intended as legal advice; for more information, please click here.