Procrastination can be costly. If you put off submitting your employer tax returns too long, you could

wind up with a failure-to-file penalty. And no employer wants that.

If you’re asking “What is it, how much could it cost, and how do I avoid it?”, you’re in the right place.

Want to avoid an IRS failure-to-file penalty? Read on to learn your employer depositing and filing responsibilities and what you need to know about an IRS failure-to-file penalty.

Key points at a glance

- Failure-to-file (FTF) penalty: 5% of unpaid tax per month (or part of a month), up to 25%.

- Failure-to-pay (FTP) penalty: 0.5% of unpaid tax per month (up to 25%); filing on time even if you can’t pay avoids the larger FTF.

- Failure-to-deposit (FTD) penalty (employment tax deposits): 2% (1–5 days late), 5% (6–15 days), 10% (over 15 days), 15% (over 10 days after an IRS notice).

- File Forms 941 (quarterly), 944 (if eligible, annually), and 940 (annually) on time; interest accrues on unpaid amounts and certain penalties.

- Relief may be available via reasonable cause, erroneous IRS advice, or First Time Abate (FTA).

- Practical tip: Use EFTPS for deposits, set reminders, and consider full-service payroll to automate filings and deposits.

Employer depositing and filing responsibilities

Being an employer comes with payroll responsibilities, including paying your employees, collecting and contributing payroll taxes, and reporting it all to government agencies.

Long story short, you must deposit and report taxes to the IRS and state and local governments.

Depositing responsibilities

Employers are generally responsible for withholding and/or contributing:

- Federal, state, and local income taxes

- Social Security and Medicare taxes (aka FICA tax)

- Federal and state unemployment taxes

- State-specific taxes

After you withhold and contribute employment taxes, set the funds aside until you deposit them with the IRS and your state and local governments.

Deposit federal income, Social Security, and Medicare taxes according to your deposit schedule (monthly or semiweekly). Your deposit schedule is based on a four-quarter lookback period. And, deposit federal unemployment taxes quarterly.

Check with your state to find out when your state and local tax deposits are due.

- Use EFTPS (Electronic Federal Tax Payment System) to make timely, trackable federal deposits.

- De minimis rule: If your total Form 941 tax for the quarter is less than $2,500, you may be allowed to pay with the return instead of making periodic deposits. Check IRS rules to confirm eligibility for your situation.

Filing responsibilities

In addition to depositing taxes, you must report them (along with employee wages) on payroll reports. Report payroll taxes to the IRS using Forms:

Form 941, Employer’s Quarterly Federal Tax Return, is a form employers must file four times throughout the year to report employee wages, tips, and payroll taxes withheld. The quarterly tax return is due:

- April 30 (Quarter 1)

- July 31 (Quarter 2)

- October 31 (Quarter 3)

- January 31 (Quarter 4)

If you deposited all taxes on time and in full for the quarter, you have 10 extra calendar days to file

Form 941.

Some small businesses with a tax liability of $1,000 or less for the year can file an annual version of this form: Form 944, Employer’s Annual Federal Tax Return. Form 944 is due annually by January 31.

Use Form 940, Employer’s Annual Federal Unemployment Tax Return, to report your federal unemployment tax liability. Submit Form 940 to the IRS by January 31 each year.

If you deposited all FUTA tax when due, you can file Form 940 by February 10.

You may also need to use state and local payroll reports for non-federal deposits. Check with your state and locality for more information on due dates.

What is a failure-to-file penalty?

Failure-to-file (FTF) happens if you fail to file a tax return to the IRS by the due date. Any taxpayer can incur a failure-to-file penalty by failing to submit individual, employer, or business tax returns.

Employers can incur a failure-to-file penalty if they do not submit employer tax returns (e.g., Form 941) by the deadline. The IRS also charges interest on penalties, which is an additional amount due.

The IRS also charges interest on unpaid amounts and may charge interest on certain penalties, which is an additional amount due.

If the IRS assigns a failure-to-file penalty, you will receive an IRS notice or letter telling you why and what you need to do.

IRS failure-to-pay penalty vs. failure-to-deposit vs. failure-to-file

A failure-to-file penalty isn’t the only cost the IRS might assign for payroll tax-related tardiness. Taxpayers can also get a failure-to-deposit (FTD) penalty or a failure-to-pay (FTP) penalty.

So, what’s the difference?

- Failure to file (FTF): Penalty taxpayers get if they do not file a return on time.

- Penalty rate: 5% per month (or part of a month) on the unpaid tax shown on the return, up to 25%.

- Failure-to-deposit (FTD): Penalty employers get if they do not deposit employment taxes on time, in the right amount, or in the right way.

- Penalty rate: 0.5% per month (up to 25%); may be reduced while you’re in an approved installment agreement.

- Failure-to-pay (FTP): Penalty taxpayers get if they do not pay the tax they report on their tax return by the due date.

- Penalty rate: 2% (1–5 days late), 5% (6–15 days), 10% (more than 15 days), and 15% if over 10 days after an IRS notice.

If both FTF and FTP apply for the same month, the FTF portion is reduced by the FTP amount for that

month.

The IRS might assign one or multiple types of penalties.

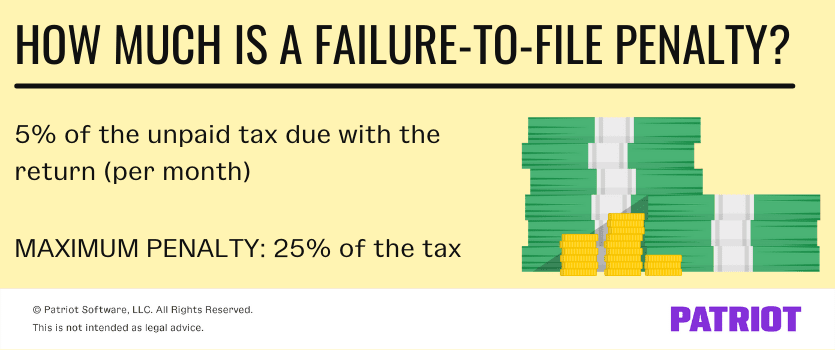

How much is a failure-to-file penalty?

A failure-to-file penalty is 5% of the unpaid tax due with the return for each month (full or partial) a taxpayer doesn’t file a return. The maximum FTF penalty is 25% of the tax.

So, your IRS late filing penalty amount depends on:

- How late the return is

- The amount of the unpaid tax due with the return

Keep in mind that the 5% penalty per month only applies to failing to file. There is also a penalty for not paying payroll taxes.

For more information, check out IRS Publication 15, Employer’s Tax Guide.

Example:

- Your Form 941 shows $6,000 of tax due that you didn’t pay by the due date, and you file two months late.

- FTF = 5% x $6,000 x 2 months = $600 (capped at 25% overall).

- If you also didn’t pay, FTP may apply at 0.5% per month. In months both apply, the FTF portion is reduced by the FTP amount for that month.

Can you get a failure-to-file penalty removed?

In some cases, you can get a failure-to-file tax return penalty removed or reduced. You can apply for a penalty reduction or removal if you:

- Have reasonable cause

- Received erroneous advice from the IRS

Reasonable cause: You can send a signed statement to the IRS explaining why your returns were late. Examples of “reasonable cause” include natural disaster, serious illness, and inability to obtain records. After you send your statement, the IRS will review it and notify you if they accept your reason. Keep in mind that penalty reduction or removal does not apply to interest.

Erroneous advice from the IRS: If you wrote to the IRS asking for advice on an issue and received erroneous advice from the IRS, you can file Form 843, Claim for Refund and Request for Abatement, along with documentation, to ask the IRS to remove the penalty. To qualify, all of the following statements must be true:

- You wrote to the IRS and asked for advice on a specific issue

- You gave the IRS complete and accurate information

- The IRS responded and gave you a specific course of action to take

- You followed the IRS’s written advice

- The IRS penalized you for following their written advice

For more information on asking for penalty removal or reduction, check out IRS Notice 746.

First Time Abate (FTA): You may also qualify for a one-time administrative waiver of certain penalties (including FTF) if:

- You have a clean filing and payment history for the prior three years,

- You filed all required returns, and

- You’ve paid, or arranged to pay, any tax due.

You can request FTA by calling the IRS or by sending a written request; include your EIN, tax period, and the specific penalty you’re requesting relief for.

If you already missed a deadline: What to do now

- File as soon as possible. This stops additional FTF months from accruing. File even if you can’t pay in full.

- Pay what you can now. Reduces penalties and interest calculated on the unpaid balance.

- Consider a payment plan. An approved installment agreement can reduce the FTP rate while the plan is in effect.

- Review your deposit records. Correct any missed or underpaid deposits promptly (FTD penalties escalate with time).

- Ask for penalty relief. If you qualify, request reasonable cause relief or First Time Abate.

How to avoid an IRS failure-to-file penalty

You have enough on your mind without having to worry about a failure-to-file penalty. So, how can you prevent it in the first place? You can:

- Get organized

- Set a calendar

- Use full-service payroll

- File even if you can’t pay. Filing on time avoids the larger FTF penalty; arrange a payment plan if needed.

- Automate deposits via EFTPS and verify your deposit schedule based on your lookback period.

- Add internal checks (e.g., monthly reconciliation) to prevent last-minute surprises.

Get organized and set a calendar so you don’t forget to file your employer tax return and deposit taxes by the due date.

Or, you can use full-service payroll so you don’t have to worry about depositing or filing taxes, period. Full-service payroll calculates and collects payroll taxes, remits them to the correct tax agencies, and files your employer tax return so you don’t have to.

Explore Patriot’s Full Service Payroll

Patriot’s Full Service Payroll can help you:

- Automate payroll tax calculations and withholdings

- Deposit federal, state, and local taxes accurately and on time

- E-file required returns (e.g., Forms 941/944 and 940)

- Stay current with changing deadlines and rules

Reducing manual touchpoints lowers the risk of missed filings and late deposits that trigger FTF, FTP, and FTD penalties.

FAQs

Generally, no. File by the due date (end of the month after the quarter). If you deposited all taxes on time and in full, you have 10 extra calendar days to file.

The FTF penalty is based on the unpaid tax shown on the return. If there’s no unpaid tax, the FTF penalty is typically $0. Other penalties (e.g., for missed deposits or information returns) may still apply.

FTF (5% per month) is much larger than FTP (0.5% per month). If you can’t pay, file on time and arrange payment to avoid the bigger FTF penalty. When both apply in the same month, the FTF portion is reduced by the FTP amount for that month.

Interest accrues on unpaid taxes (and, in some cases, on penalties) from the original due date until paid, compounding daily at the federal rate.

Yes. For certain unpaid employment taxes, the IRS may assess the Trust Fund Recovery Penalty against responsible individuals who willfully fail to collect or pay. This is separate from the FTF penalty for late returns.

2% (1–5 days late), 5% (6–15 days), 10% (over 15 days), and 15% if over 10 days after an IRS notice. Deposit timely via EFTPS to avoid escalating rates.

Call the IRS or send a written request identifying your EIN, the tax period, and the penalty. You generally need a clean compliance history for the prior three years, all returns filed, and tax paid or arranged to be paid.

This article has been updated from its original publication date of October 25, 2021.

This is not intended as legal advice; for more information, please click here.