Running a business means spending money. And, starting a business means spending money before you begin earning money. That’s where the saying, “You have to spend money to make money,” comes from, after all. The idea of spending money to earn money comes into play with sunk costs. So, what is a sunk cost?

Sunk cost meaning

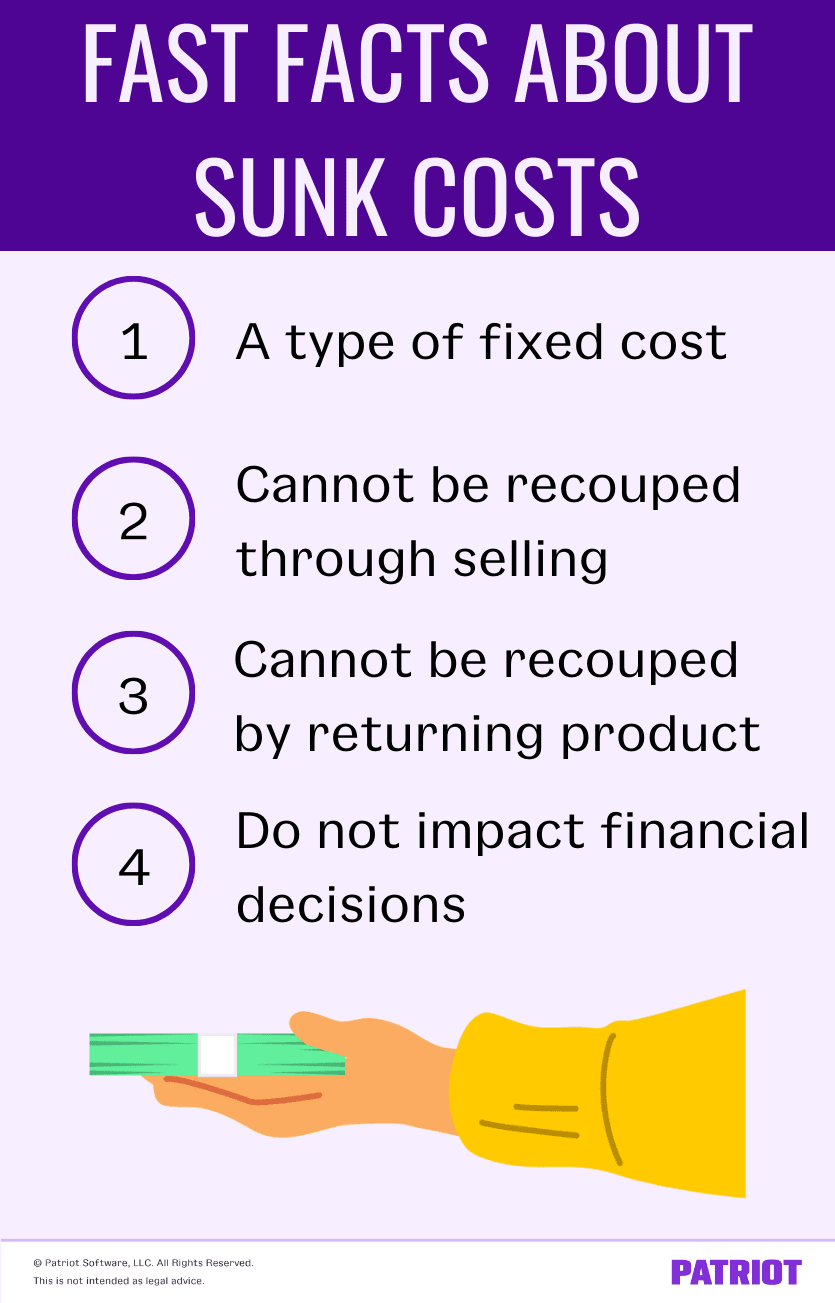

The sunk cost definition is money your business already spent and cannot recover. With sunk costs, a business cannot sell what it purchased to recoup the costs.

For example, purchasing a machine to manufacture goods is a sunk cost because the business cannot resell the machine to recover the full cost of purchasing it.

Sunk costs do not impact financial decisions. So, do not include sunk costs in future decision-making for the business.

Fixed costs vs. sunk costs

All sunk costs are fixed costs of doing business. But, not all fixed costs are sunk costs. So, what’s the difference between a fixed cost and sunk cost?

Fixed costs: A set cost of doing business that does not change regardless of an increase or decrease in production. Fixed costs are independent of business practices and are expenses the business must pay. You can completely recover a fixed cost through selling (e.g., reselling a machine for the purchase price).

Sunk costs: A set cost that does not change no matter how much production increases or decreases. Unlike fixed costs, you cannot recover sunk costs through reselling or returning the purchase.

Sunk costs vs. relevant costs

Again, sunk costs are irrelevant to future business decisions because you already spent and cannot recover the funds. But, how are sunk costs not relevant costs? After all, sunk costs are an expense you pay and should consider, right? Well, not exactly.

Relevant costs are all of the expenses that play a role in your decision-making process. And, future costs are also relevant costs because they are expenses your business will incur in the future that can impact your current decisions (e.g., product pricing). Consider your relevant costs with the potential revenue of the expense when making financial decisions.

Sunk costs are the expenses you already incurred and do not play a role in purchases you plan to or will make.

Sunk cost fallacy

Have you ever made a business decision that you thought might not be profitable, but you pressed on because you’d already invested time and money into it? You’re not alone.

The sunk cost fallacy is when individuals or businesses follow through on a decision even when they know the expense may be higher than the potential benefits. And, the reasoning behind the fallacy is that the individual or business already spent time, money, and effort, so they want to see it through.

The sunk cost fallacy can result in wasted expenses, time, and energy, regardless of whether the business follows through or abandons the project.

Avoid the sunk cost fallacy by monitoring the outcomes of your financial decisions and stopping projects that no longer show benefit. Do not compound sunk costs by continuing to spend money on investments or financial decisions with a negative financial outcome.

Sunk cost examples

Sunk costs are a normal part of operating a company. Take a look at some sunk cost examples in business.

Example 1

You decide to create an advertising campaign and add funds to your budget. As part of the campaign, you spend $2,000 advertising on a local radio station. The $2,000 you spend on advertising is a sunk cost.

Why are the funds spent on advertising a sunk cost if the marketing campaign brings new customers and sales? Because the business cannot directly recover the $2,000 spent on the advertisements. The advertiser does not return the money to the business directly, so the profits from sales do not count as recovered funds.

Example 2

Your business sells baked goods, and you decide to start working on new products. You purchase the materials to begin experimenting with recipes. But as you experiment, you do not sell the experimental baked goods and label the new products as testers for customers to taste.

Experimenting with new recipes is a part of research and development. You spend $100 on materials for one potential new product, and nobody purchases the product. After a test run, the customer feedback is that the new product is not something you should sell.

The $100 you spent to test out the new product is a sunk cost because there is no return on investment when you decide not to sell the product. And, you cannot return the purchased materials or resell the materials to recoup the funds.

Example 3

Perhaps the most common sunk cost example is the expense of having employees. The wages you pay to employees are sunk costs as soon as you pay out the funds. All wages are sunk costs, including:

- Sign-on bonuses

- Overtime

- Paid time off (PTO)

- Commission

- Standard bonuses

And, the costs of doing payroll are also sunk costs. So, payroll taxes, federal unemployment (FUTA), and state unemployment (SUTA) taxes are all sunk costs, too.

Include any benefits, such as health insurance or retirement contributions, in the sunk costs.

Example 4

You decide to purchase new office equipment for your business, including desks, computers, and chairs. The company you purchase the equipment from has a 90-day return policy. After the 90-day return policy expires, the equipment is now a sunk cost for the business.

On days one through 90, the equipment is simply a fixed cost because you can return the items and recover the entirety of the funds you spent. However, on day 91, the equipment automatically becomes a sunk cost if you do not return the items. If you resell the equipment for a lower cost than the purchase price, the difference between the original cost and the resell cost is the sunk cost.

Example 5

Say your employees frequently travel as part of their work for your business. You decide to purchase a company car to better track travel expenses. You purchase the car for $15,000 and have monthly payments of $200.

The monthly payments of $200 are the sunk cost in the vehicle, not the $15,000. Why? Because only the amount you actually spent on the vehicle is a sunk cost, and you can still resell the vehicle.

This is not intended as legal advice; for more information, please click here.