You want a simple way to complete bookkeeping tasks. After all, the more organized your process, the faster you can record transactions and get back to business. To stay on track, you might consider using an accounting cycle. And to do that, you need to know the accounting cycle steps.

Read on to learn the accounting cycle definition and steps in accounting process.

- Accounting software that is easy to use

- Quick and accurate reporting

- Free USA-based expert support

What is the accounting cycle?

The accounting cycle is the process of recording your business’s financial activities consistently and accurately. An accounting cycle looks back in time at the end of a designated period (e.g., monthly, quarterly, or annually). There are several steps in the cycle, beginning when a transaction occurs and ending when you close your books.

You can use the accounting cycle to make accounting easier by breaking your bookkeeping responsibilities down into smaller, bite-sized tasks.

Follow the accounting cycle to:

- Manage your time

- Set goals

- Compare one cycle to another

- Reconcile bank statements

Use accounting software? You can program dates for your accounting cycle, and the software generates reports based on your selected dates.

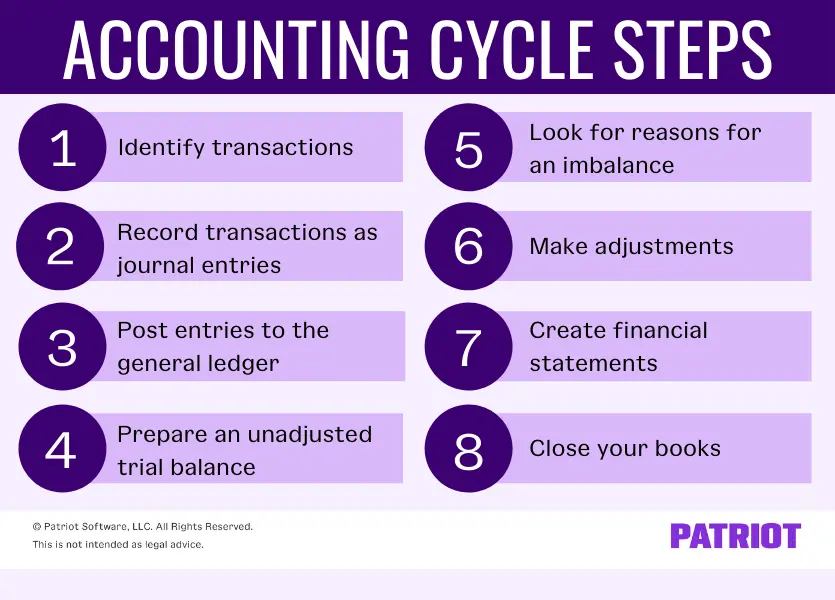

Accounting cycle steps

Usually, there are eight steps in full-cycle accounting. But depending on how you do your accounting, you might be able to modify, skip, or even add steps.

Many steps in the standard accounting cycle are meant for accrual accounting, where you use a double-entry accounting system (i.e., debits and credits). If you use accrual accounting, you can follow all the steps in the accounting cycle.

If you use a single-entry accounting system (i.e., cash-basis accounting), you can still use the accounting cycle to record entries, close your books, etc. But, you don’t need to follow the steps that require you to check entries for debits and credits.

The bottom line: Use the steps that help you stay organized and maintain accurate records. So, what are the steps in the accounting cycle? Get started here.

1. Identify transactions

What is the first step in the accounting cycle? The first step in the accounting cycle is to identify business transactions. Your business transactions are any financial activities where there is an exchange of money.

Examples of transactions include:

- Product sales

- Purchase returns

- Purchases

- Liability payments

Use source documents to identify business transactions, such as receipts and invoices. Save these kinds of financial documents to support your records. As you identify business transactions, decide which type of account they fall under.

Roadblock: If you don’t have a separate business bank account, this step will likely take longer. You’ll need to sort through business and personal expenses to identify your business transactions.

2. Record transactions as journal entries

Your journal is where you initially record business transactions. It is a running list of financial activities, like a checkbook. Track transactions in your journal chronologically as they happen.

To do this, create journal entries.

In accrual accounting, you record transactions when they take place, with or without the transfer of money. So, you must create two entries for each transaction: a debit for one account and a credit for another. The debit and credit should be equal.

If you use cash-basis accounting, record transactions when cash physically exchanges hands (i.e., when you receive money or pay). You do not need to make multiple entries.

3. Post entries to the general ledger

The general ledger is a record that sorts and summarizes all of your business transactions. Your general ledger consists of these five main account types:

- Assets

- Liabilities

- Equity

- Revenue / Income

- Expenses

When posting entries to your general ledger, organize transactions into these different accounts and subaccounts. For example, you could record a cash payment from a customer under your revenue account.

4. Prepare an unadjusted trial balance

You want accurate books. In fact, you need accurate books. That means your debit and credit entries must be equal. So, the next accounting cycle step is to create an unadjusted trial balance.

An unadjusted trial balance shows you whether your balances match. Make a note of each account balance. Add all the debit balances together and add all the credit balances together. If the two totals are not the same, move on to the next step…

5. Look for reasons for an imbalance

If your trial balance shows that there’s an imbalance in your books, use this step to work it out. Look for errors and identify adjusting entries so you can make adjustments and balance your books.

Adjusting entries: At the end of an accounting period, you might have incurred expenses but not paid for them yet. And, you might have earned income but not collected it yet. Use adjusting entries to recognize transactions that have occurred but have not been recorded.

For example, you earned interest on a bank account balance. You have not recorded the interest in your books, but it appears on your bank statement. Use an adjusted entry to recognize the interest in your books.

6. Make adjustments

If you need to make adjustments because of an imbalance, go ahead and make them during this step. To make adjustments, simply create new journal entries, if applicable.

Do an adjusted trial balance after making adjusting entries and before creating financial statements to see if the debits and credits match after making adjusting entries.

7. Create financial statements

Once your accounts are up-to-date, create financial statements. Financial statements compile your business’s financial information and show your financial health.

There are three main types of business financial statements:

- Income statements compare your profits and losses for the period

- Balance sheets determine progress by detailing assets, liabilities, and equity

- Cash flow statements show money coming into and out of your business

Use your financial statements to measure performance, make improvements, and set goals. You can also use statements to apply for loans or investments and negotiate terms with vendors.

8. Close your books

So, what is the last step in the accounting cycle? Ta-da, you’re here! The final accounting cycle step is to close your books.

Closing your books wraps up financial activities for the period. To close your books, you need to:

- Update accounts payable

- Reconcile accounts

- Review your petty cash fund

- Count inventory

…And so on.

When you close your books, you should get your accounting set up for the next period. Decide which processes are moving your business forward. Create a calendar for completing future tasks. File any financial documents from the last period and get rid of old documents that are no longer useful.

This article has been updated from its original publication date of September 5, 2017.

This is not intended as legal advice; for more information, please click here.