As a business owner, there are a lot of things to pay attention to when running your company. Payroll, hiring, bookkeeping … the list goes on and on. And, that list includes monitoring all of your business records. So, what are the most important business records to track?

Business records to track

Do you know how long to keep business records? The IRS requires you to keep several records for a certain amount of time (e.g., tax records).

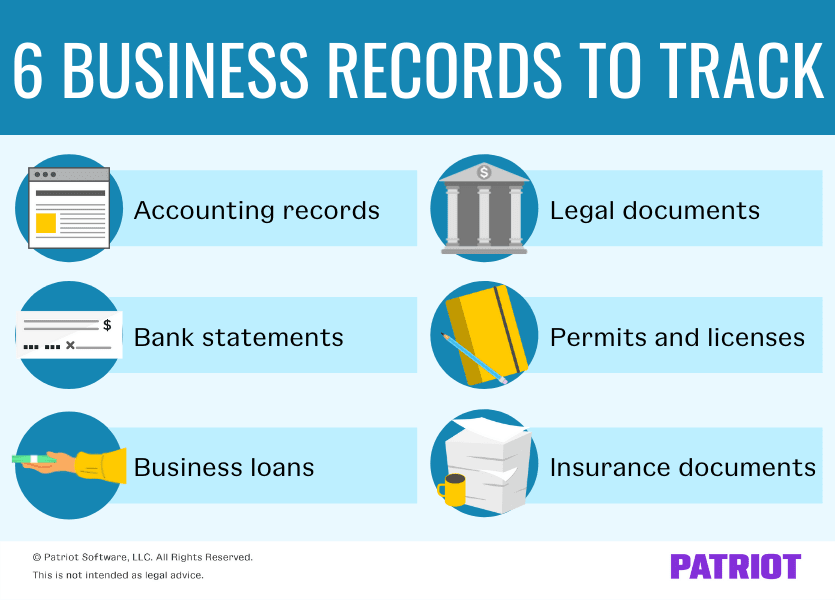

But, what are the types of record keeping you should keep an eye on even if you are not required to keep them? There are six business records to monitor:

- Accounting records

- Bank statements

- Business loans

- Legal documents

- Permits and licenses

- Insurance documents

1. Accounting records

You document all of your business’s transactions in your accounting records. The necessary accounting records for business include all of the information about your income, equity, and expenses. From your financial accounting records, you can compile the data into financial statements and compute small business ratios.

You must track your accounting records to:

- See your business’s financial health

- Measure your company’s profitability over time

- Analyze patterns to make better financial decisions

- Determine if you have enough capital to cover your expenses

- Understand if your current budget is successful

Monitor your financial records at regular intervals (e.g., monthly or quarterly). And, verify that you track every expenditure and source of income. Without all of the accounting data, your records are incomplete and give inaccurate information. Keep all receipts and copies of invoices to back up your records.

The federal government requires you to keep financial documents that show your income and expenses. Use your accounting records to file your business income tax returns.

After you file your tax return, keep your tax records. Why? Because the IRS requires you to keep these records for a specific amount of time. If you do not file a return, you must keep the tax records indefinitely. Check with your accountant, state, or the IRS to confirm how long you must keep individual records.

Track your expenses and income, generate financial reports, make unlimited payments to vendors, and so much more!

2. Bank statements

Your bank statements detail all of your accounts with the bank. The accounts may include your checking, savings, investment, and credit card records. And, you can reconcile your bank accounts with the accounting records you must track.

Compare your bank statements to your financial records and review them for potential mistakes. If your bank statements do not match your accounting records, there may be an error in your books.

Bank statements help you track your business’s progress, too. And, you use your bank statements to file your taxes.

3. Business loans

Do you have a business loan? If so, tracking your loan is crucial. You want to track things like:

- Amount of the original loan

- Loan approval date

- Disbursement date

- Expected pay-off date

- Loan payment due dates

- Interest rate changes (if applicable)

Keep all documents for the loan somewhere you can easily access them. If you decide to pay off the loan sooner or need an extension, provide the documentation to the loan provider.

Track business loan repayments in your books. Debit the loan account to decrease the liability in your books and credit the cash account for the payments.

The goal of tracking your business loan is to ensure you do not miss payments and manage risks. And, you can increase your chances of receiving loans in the future through responsible loan repayment plans. Not missing payments and paying off the entire loan as outlined in the loan agreement helps increase your business credit score. And, a higher business credit score tells lenders that you are a responsible borrower with lower risk.

4. Legal documents

The legal documents your business has depend on your business structure. For example, incorporated companies (e.g., C corporation) must maintain their articles of incorporation. Other legal documents include partnership agreements for partnerships or a DBA (aka doing business as) for sole proprietorships.

You must maintain all legal documents proving you own your business. Keep these documents somewhere safe in case you need to provide proof of ownership.

Remember that tracking your legal documents is different than tracking financial records. You must know where you store your documents so you can easily pull them whenever you need them.

5. Permits and licenses

State and local governments may require you to obtain various permits or licenses to operate your business. And depending on your business’s industry, you may need to apply for and receive industry-specific permits or licenses.

For example, businesses that sell food or beverages may need to obtain a health permit to sell those items. And if you decide to sell alcohol at your business, you need to apply for a liquor license.

Track your permits and licenses because you may need to periodically renew them. And, keep an eye out for any changing laws for the permits or licenses your business has. If a law changes where you must post or how often you need to renew a permit or license, comply promptly to avoid penalties or fines.

6. Insurance documents

There are various types of insurance policies you may need to purchase when running a business. Examples of the types of insurance you may purchase include:

- Business liability insurance

- Renters insurance

- Auto insurance

- Workers’ compensation insurance

- Business income insurance

- Professional liability insurance

- Cyber insurance policies

But to use your insurance, you need to provide proof of insurance. Keep track of where your insurance policies are. That way, you can have your insurance policy number and other identifying information handy if you need to file a claim.

Insurance policies can help protect your company in the event of:

- Natural disasters (e.g., flooding)

- Lawsuits

- Employees getting sick or injured while working

- Data breaches

- Car accidents

- Damage to your place of business (e.g., fire)

Consider keeping copies of your insurance policies in a location where they cannot be damaged. For example, you may store records digitally in the cloud or physically in a fireproof lockbox. Also, ask your insurance provider if they offer a digital account for you to download or view your insurance online instead of paper documents.

This article has been updated from its original publication date of April 8, 2016.

This is not intended as legal advice; for more information, please click here.