When you sell goods to customers, you likely collect and remit sales tax to the government. And when you purchase products, you typically pay sales tax. But, how do you record these tax collections and payments in your accounting books? Sales tax accounting.

You should understand accounting for sales tax to maintain organized and accurate records. That way, you can easily record sales tax in your books.

Read on to learn:

- What is sales tax? (Overview)

- What is sales tax accounting?

- Accounting for sales tax collected from customers

- Accounting for sales tax paid on purchases

What is sales tax? (Overview)

Sales tax is a pass-through tax tacked onto consumer purchases.

When customers buy from you, you do not pay sales tax. Customers pay sales tax. You simply collect and remit it to your state or local government (it passes through you). Sales tax is not part of your business’s profits.

When you buy goods subject to sales tax, the seller collects the tax from you. They then remit it to the proper government.

Who’s responsible for collecting/paying sales tax?

You might be wondering, do I have to charge sales tax? As a seller, you’re responsible for collecting sales tax if you have sales tax nexus (e.g., a business presence) in the state. Likewise, as a buyer, you must pay sales tax if the seller has sales tax nexus.

The majority of states impose sales tax, but there are some exceptions. The following states do not have a state sales tax (but may have local sales tax laws):

- Alaska

- Delaware

- Montana

- New Hampshire

- Oregon

Some goods, like raw materials, may be sales tax exempt. If you sell raw materials to another business that then sells them to customers, you generally won’t collect sales tax from the business. That business will collect sales tax from its customers.

Calculating sales tax

How do you calculate sales tax? Sales tax is a percentage of a consumer’s total bill. States, counties, and cities set sales tax rates.

You can use the sales tax formula to calculate sales tax:

Sales Tax = Sales X Sales Tax Rate

Let’s say your state has a sales tax rate of 5%. The customer’s total bill is $400. You must collect $20 in sales tax ($400 X 0.05) and charge the customer a total of $420 ($400 + $20).

What is sales tax accounting?

Sales tax accounting is the process of recording sales tax in your accounting books.

If your business has a physical presence in a state with a sales tax, you must collect sales tax from customers. Then, record the collected sales tax in your books. If a seller charges you a sales tax, record the sales tax expense in your books.

You can record the sales tax by creating journal entries. The sales tax journal entry you record depends on whether you:

- Collected sales tax from customers

- Paid sales tax to vendors

1. Accounting for sales tax collected from customers

Collected sales tax is not part of your small business revenue. When you collect sales tax from customers, you have a sales tax liability.

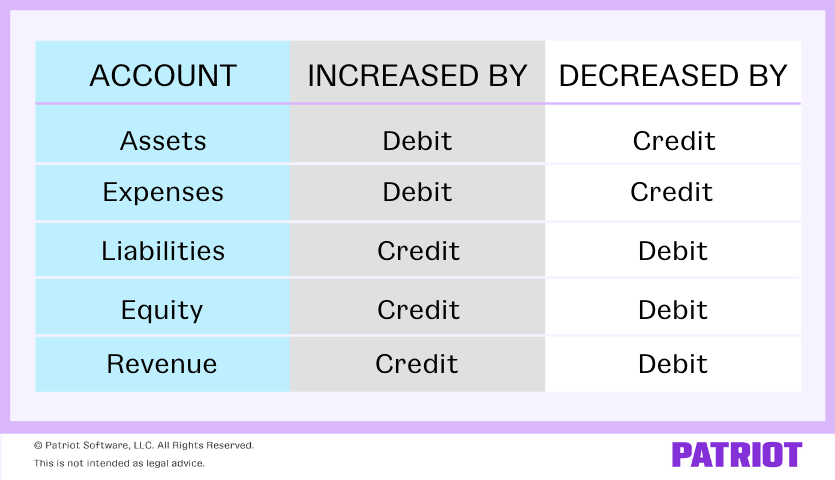

You must remit your sales tax liability to the government. As a result, collected sales tax falls under the liability category.

Liabilities are increased by credits and decreased by debits, as shown in this chart:

For organized records, create a Sales Tax Payable account. This represents sales tax money you collected from customers but have not yet remitted to the government. You owe this money to the government.

When you collect sales tax from customers, you increase the corresponding liability account, which is your Sales Tax Payable account. And because you collect the sales tax, you also must increase your Cash account. Your Cash account is increased by debits.

Because sales tax is lumped into the total amount your customers pay, you will include the sales tax as part of the total sales revenue in your accounting books, too. To do this, credit your Sales Revenue account.

To record received sales tax from customers, debit your Cash account, and credit your Sales Revenue and Sales Tax Payable accounts.

Your sales tax payable journal entry should look something like this:

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| X/XX/XXXX | Cash | Collected sales tax | X | |

| Sales Revenue | X | |||

| Sales Tax Payable | X |

When you remit the sales tax to the government, you can reverse your initial journal entry. To do this, debit your Sales Tax Payable account and credit your Cash account. This reduces your sales tax liability.

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| X/XX/XXXX | Sales Tax Payable | Remitted sales tax | X | |

| Cash | X |

Example

Let’s say you sell $5,000 worth of goods to a customer, which is subject to a 5% sales tax. First, determine how much sales tax you need to collect by multiplying the sales by the sales tax rate.

$5,000 X 0.05 = $250

Collect an additional $250 for sales tax. In total, collect $5,250 ($5,000 + $250) from your customer. Record both your sales revenue of $5,000 and your sales tax liability of $250 in your accounting books.

Debit your Cash account for the total amount the customer paid you. Then, credit your Sales Revenue account the purchase amount before sales tax. And, credit your Sales Tax Payable account the amount of the sales tax collected.

Take a look at the following journal entry:

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| X/XX/XXXX | Cash | Collected sales tax | 5,250 | |

| Sales Revenue | 5,000 | |||

| Sales Tax Payable | 250 |

After remitting the sales tax of $250, create a new journal entry to decrease your Sales Tax Payable and Cash accounts:

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| X/XX/XXXX | Sales Tax Payable | Remitted sales tax | 250 | |

| Cash | 250 |

2. Accounting for sales tax paid on purchases

When you purchase goods and pay sales tax on those goods, you must create a journal entry. In this case, the sales tax is an expense, not a liability.

Generally, your total expense for the purchase includes both the price of the item(s) and the sales tax. You don’t need to call out the sales tax you paid in a sales tax expense entry. It’s just part of your overall purchase expense.

Decrease your Cash account and increase the corresponding expense (e.g., Supplies) account. Because expenses are increased through debits, debit an expense account and credit your Cash account.

Your journal entry should look like this:

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| X/XX/XXXX | Expense | Purchased goods | X | |

| Cash | X |

Example

You purchase new business supplies for $1,000. The supplies are subject to a sales tax of 4%, which is $40 in sales tax ($1,000 X 0.04). Your total bill is $1,040 ($1,000 + $40), which includes the amount of the supplies and the 4% sales tax.

To record your journal entry, debit your Supplies account and credit your Cash account:

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| X/XX/XXXX | Supplies | Purchased goods | 1,040 | |

| Cash | 1,040 |

Looking for an easy way to maintain your small business’s accounting books? Patriot’s online accounting software offers a simple way to track income and expenses. And, we provide free, USA-based support. Get your free trial now!

This article has been updated from its original publication date of October 4, 2018.

This is not intended as legal advice; for more information, please click here.