As a small business owner, you have a lot on your plate at all times. You do your best to keep your accounts, finances, and books in order. But sometimes, things just slip your mind.

At some point or another, you might spend more than what you have in your account. When this happens, you have non-sufficient funds. Read on to learn what are non-sufficient funds, what to do if you have them, and how to avoid insufficient funds.

What are insufficient funds?

Non-sufficient or insufficient funds occur when someone doesn’t have enough money in their account to cover a transaction or payment. In most cases, if you spend more than what you have in your account, you will be charged an NSF fee from your bank. An NSF charge amount can vary depending on the amount of insufficient funds in bank account and banking institution.

In addition to paying your own bank NSF fees, the payee might also owe fees to their bank because of your insufficient funds (e.g., NSF check).

You might deal with insufficient funds when you use checks, pay with your debit card, or make ACH payments (e.g., direct deposit).

Say you purchase a new computer for $300 but only have $250 in your checking account. Because you are spending $50 more than what is in your account, you have insufficient funds.

The most common cause for NSF is automatic withdrawals. Many business owners try to automate as many processes as possible, including payments. Automatic withdrawals can be easy to forget about after you set them up.

As a business owner, you should avoid having non-sufficient funds. Not only are NSF fees costly to your small business, but having low or non-sufficient funds can damage your business’s reputation.

What to do if you have insufficient funds

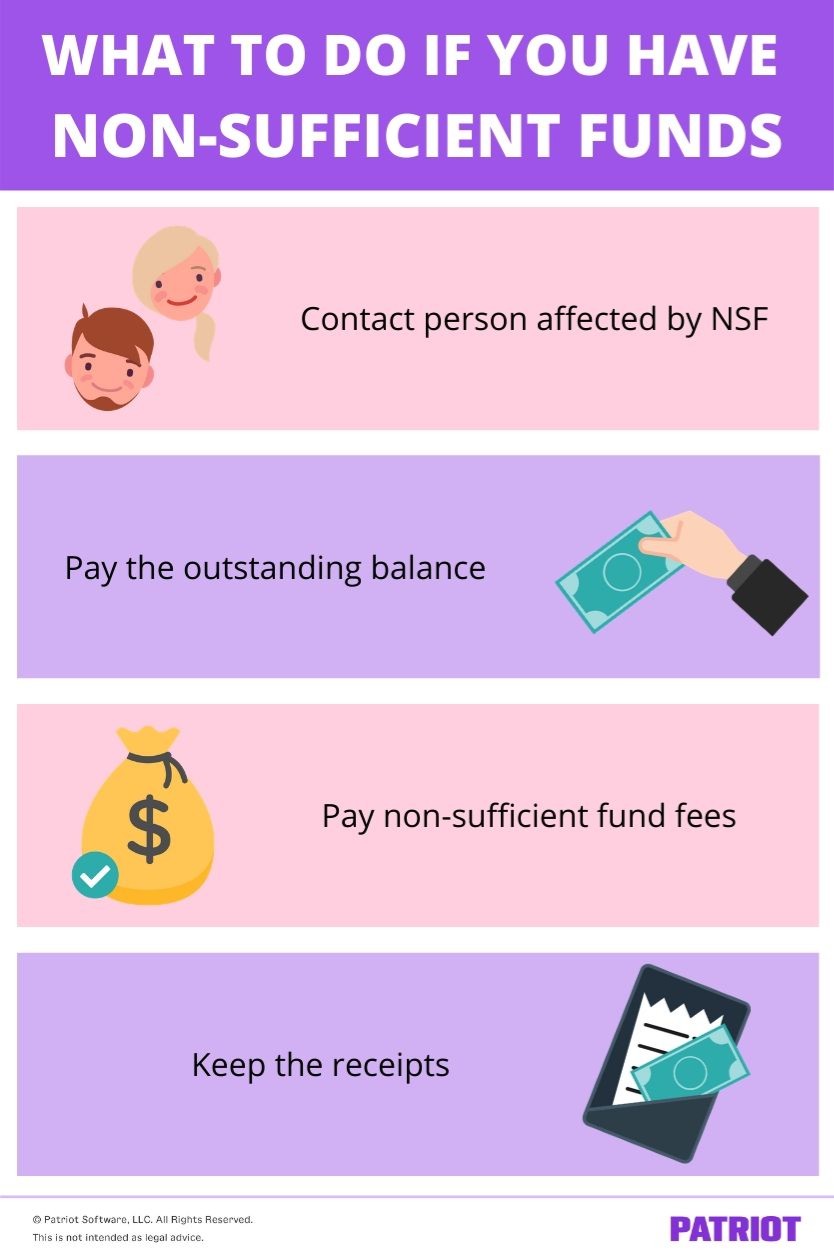

If you have non-sufficient funds, don’t panic. Instead, follow the checklist below to ensure you tidy up any NSF issues:

- Contact person affected by NSF

- Pay the outstanding balance

- Pay NSF fees

- Keep receipts

1. Contact person affected by NSF

First things first, make sure you contact the affected person as soon as possible if you have insufficient funds. Clarify that you are aware of the funds and that you’re going to make things right. This assures the individual that you’re not intentionally withholding their payment.

2. Pay the outstanding balance

Pay the affected individual the amount that you owe them. If they were charged an NSF fee by their bank, make sure you reimburse them for the charge, too.

3. Pay NSF fees

Again, if you have non-sufficient funds, you will likely have to pay a fee to your bank. Check with your bank to see whether you owe any NSF fees. If you do owe the bank fees, be sure to pay them right away to avoid interest charges.

4. Keep receipts

Anytime you have non-sufficient funds or issues with payment, document your proof of payment to the bank and payee. Ask for and keep receipts as a record of your payments.

Be sure to keep any NSF receipts in your records. If there are any disputes in the future, use the receipts to prove you settled the NSF issue.

What to do if a customer has non-sufficient funds

Say the shoe is on the other foot and you have a customer with non-sufficient funds. What do you do?

When a customer’s check bounces or their payment doesn’t go through due to NSF, you need to take a few actions. First things first, contact the bank and customer.

As soon as you find out the customer has insufficient funds, contact your bank. Explain the situation and find out what options you have.

In some cases, it might be a fluke that the customer has non-sufficient funds. If you think this is the case, ask the bank if they can try depositing the check again. If there aren’t sufficient funds, ask the bank if they can do an enforced collection (e.g., future money the customer deposits goes to you).

You’ll also want to reach out to the customer directly. In some cases, you might be able to resolve the situation by solely contacting the customer.

When you reach out, explain the situation offer different payment methods (e.g., credit card). If you can’t reach the customer via phone, try sending them a letter detailing the reason why you’re contacting them, the NSF total, any fees, and your contact information.

If you can’t resolve the customer’s NSF issue by contacting the bank or customer, you might need to get help from an outside source. If you can’t resolve a customer’s NSF and get paid, consider getting help from the local police department or district attorney. You can also hire a collection agency or go to small claims court.

Non-sufficient fund fees

Non-sufficient fund fees vary depending on your bank and location. Some states and banks might have higher fees than others.

Insufficient fund fees typically range between $27-$35. The recipient of a check or insufficient payment may also have to pay an NSF fee between $20-$40. In some cases, the payee might have to pay a percentage of the bounced amount or check (e.g., 20%).

Banks typically have options and safeguards in place in case your account balance falls below zero. Many banks offer overdraft protection. That way, if you do have insufficient funds, the transaction will still go through. However, you will still be responsible for paying an overdraft fee.

Overdraft vs. NSF fees

So at this point you’re probably wondering, what’s the difference between overdraft and NSF fees?

Banks charge NSF fees when they return payments, such as checks. Overdraft fees only occur when a bank accepts a payment that overdraws an account.

Basically, if your bank refuses the check or payment, you will likely incur an NSF fee. If the bank accepts the check or pays the seller, your account balance will be negative and you will owe an overdraft fee.

How to avoid non-sufficient funds

Having non-sufficient funds isn’t a good look for any business owner. But, forgetting or miscalculating account funds can happen to the most seasoned entrepreneur.

Luckily, there are plenty of precautions you can take to steer clear of having non-sufficient funds.

Here are a few ways you can avoid NSF and costly insufficient fund fees:

- Create a budget and stick to it

- Monitor your bank accounts regularly (e.g., weekly)

- Keep a list of automated charges

- Organize your funds

- Track purchases and deposits

- Keep extra cash in your accounts

Consider also setting up a business cash reserve to cover unexpected insufficient funds and fees. That way, you have some backup cash in case your account suffers from insufficient funds.

Need help keeping track of your business’s income and expenses? Patriot’s accounting software has you covered with a simple way to streamline your books. Try it for free today!

This article has been updated from its original publication date of October 19, 2015.

This is not intended as legal advice; for more information, please click here.