Taxes are a big part of running a business, and they can take a toll on your bank account. But sometimes, you can receive an income tax refund for your business. If you do, you need to know how to record a journal entry for income tax refund in your books.

Should your business make a journal entry for income tax refund?

The IRS or state issues a tax refund if you overpay on your taxes. Refunds only occur when you remit more taxes to the government than you or your business owe. But, do you need to record an income tax refund in your business accounting books? The answer: It depends.

Your business structure determines if you need to record a journal entry for an income tax refund. Only certain business entities need to record journal entries for income tax refunds.

Business entities that do not need to record an income tax refund as a journal entry include:

- S corporations

- Sole proprietorships

- Partnerships

- LLCs*

S Corps, partnerships, and sole proprietorships all have pass-through taxation. With pass-through taxation, the owner includes business income on their personal income tax return. The business does not directly pay the taxes, and the owner receives any refunds rather than the company. Because the owner receives a refund and not the business, do not record the journal entry in the business’s books.

*If you have an LLC, you may file your taxes as an S Corp, sole proprietorship, partnership, or C Corp. So if you have an LLC, how you are taxed determines if you must record a journal entry for income tax refunds. For example, an LLC taxed as a corporation must record an entry for refunds.

So, what type of business does need to have a journal entry for a business income tax refund? C corporations.

C corporations (and business entities taxed as C Corps) are the only business entity that has to record a journal entry for income tax refunds issued by the government. Why? Because C corporations and entities taxed as C Corps are the only businesses that directly pay federal income tax to the government with double taxation

An LLC taxed as a C Corp and C Corps both use double taxation instead of pass-through taxation. C Corps pay taxes on their annual earnings. When the corporation pays out dividends to shareholders, the dividends have tax liabilities. The shareholders pay taxes on the dividends they receive. So, the income is taxed twice (hence, double taxation).

If your business is a C corporation (or is taxed as one) and you overpay business income taxes throughout the year, the government issues your business a refund check. Document the income tax refund you receive in your business’s books. But, how does the government issue a tax refund?

- Log in anytime, anywhere to record transactions

- Track your expenses, income, and money

- Automatically import bank transactions

How the government issues tax refunds

Typically, taxes are a cost of doing business. When you owe taxes, you have liabilities on your balance sheet until you remit the taxes. If the government issues a refund to you, the refund is an asset (aka a receivable). Let’s dive into a few reasons why you may receive a refund.

Tax credits

Your business may receive business tax credits that reduce your tax liability. Tax credits lower your tax liability by subtracting the credit from the total amount of taxes you owe.

For example, say your tax liability is $1,000, and you have a tax credit of $500. With the $500 tax credit, you only owe $500 to the government.

In some cases, your tax credit may be larger than your tax liability. If this happens, you may be subject to a refund if the tax credit is refundable. For example, you have a $1,000 refundable tax credit and a $500 tax liability. You would receive a $500 refund.

Tax installments

Throughout the year, your business may make monthly or quarterly payments to the government. When you file your business tax returns, the IRS applies your payments to the balance you owe.

If you do not remit enough taxes to the government based on your tax filings, you owe the government the difference. For example, your returns show a tax liability of $1,000. You paid $200 per quarter. Your tax bill is $200 because you only paid $800 ($200 X 4 quarters) for the year.

Overpaying your taxes throughout the year could result in a tax refund. For example, you pay $300 each quarter, and your tax returns show a tax liability of $1,000. The government owes you a refund of $200 because you paid $1,200 ($300 X 4 quarters) instead of $1,000 for the year.

If you receive a refund for your business, record the income tax refund journal entry in your books.

How to record tax refund in accounting

Again, record taxes as liabilities in your books before paying them. Mark a refund as a receivable (aka an asset) when you receive the refund. When using double-entry bookkeeping, there are two steps for recording an income tax refund.

Step 1: Record the original tax payment

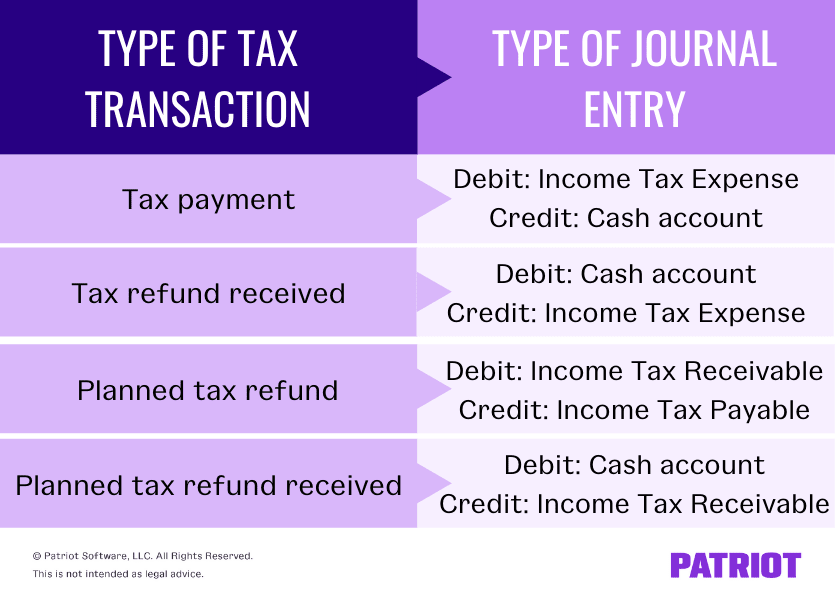

When you remit the tax payment to the government, record the payment in your general ledger. Use debits and credits to show you paid the taxes:

- Debit your Income Tax Expense account

- Credit your Cash account

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| XX/XX/XXXX | Income Tax Expense | Remit Tax Payment | X | |

| XX/XX/XXXX | Cash | X |

Debit your Income Tax Expense account to increase your expenses and show that you paid the tax. Credit your Cash account to reduce your assets. This shows that you have less cash after paying the tax expense.

Step 2: Make an accounting entry for the income tax refund

Receive your income tax refund? Great! Enter the refund amount into your general ledger to reverse the tax payment transaction.

Use the following entries to show you received an income tax refund:

- Debit your Cash account

- Credit your Income Tax Expense account

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| XX/XX/XXXX | Cash | Received income tax refund | X | |

| XX/XX/XXXX | Income Tax Expense | X |

Debiting your Cash account increases your assets and shows that you received the refund. Crediting your Income Tax Expense account reverses your original entry, decreasing your expenses.

Journal entry for anticipated refund

What if you know you are getting a refund but have not received it yet? You can record that in your books, too. To show a future refund:

- Debit your Income Tax Receivable account

- Credit your Income Tax Payable account

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| XX/XX/XXXX | Income Tax Receivable | Refund anticipated | X | |

| XX/XX/XXXX | Income Tax Payable | X |

Debit your Income Tax Receivable account to increase your assets and show that you expect to receive a refund in the future. Credit your Income Tax Payable account to reverse the original entry of paying the taxes.

After you receive the anticipated refund, record a second journal entry to move the refund to your Cash account. To record the refund you received:

- Debit your Cash account

- Credit your Income Tax Receivable account

Your journal entry should look like this:

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| XX/XX/XXXX | Cash | Refund received | X | |

| XX/XX/XXXX | Income Tax Receivable | X |

This article has been updated from its original publication date of September 28, 2017.

This is not intended as legal advice; for more information, please click here.