Do you receive most of your business income in cash? If so, you’re probably a cash-intensive business, which can put you under greater IRS scrutiny. Why? Because cash transactions do not leave a paper trail. So if you run a cash-intensive business, you need to keep detailed records.

Read on to learn the cash-intensive business definition, common examples, and the IRS cash-intensive audit process.

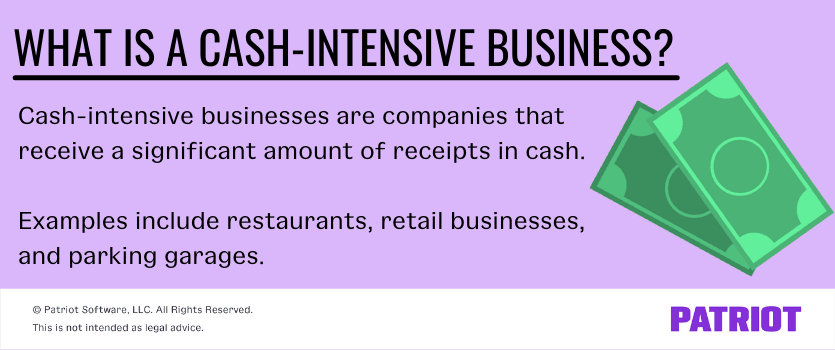

What is a cash-intensive business?

A cash-intensive company is one that receives a significant amount of cash receipts. So if you’re a business that handles a high volume of small-dollar transactions, you might be cash intensive. And if you are, you likely use a cash drawer, or register, to store currency, record transactions, and balance your till.

Cash-intensive business examples include:

- Restaurants

- Grocery or convenience stores

- Retail businesses

- Parking garages

- Vending machines

- Contract workers who receive payment in cash (e.g., construction or trucking)

Keep in mind that the above cash-intensive business list is not all-inclusive.

Although businesses can also accept debit or credit card, mobile wallet, or check payments, cash-intensive companies see high amounts of cash transactions.

What is the concern?

Receiving payments in cash can make it easier for individuals and businesses to engage in two forms of illegal activity:

- Unreported income

- Money laundering

Unreported income

Because of the lack of a paper trail, some cash businesses fail to report all transactions to the IRS.

To get away with this, some companies may misappropriate funds by pocketing cash before recording it, stealing money after recording it, or creating fraudulent disbursements.

Red flags of unreported income include:

- A company that is still in business despite repeated annual losses

- Individuals who maintain a cost of living that’s higher than reported income

- Significant differences between a business’s gross profit margin and the industry average

Money laundering

Running a cash business can also make it easier for a company to engage in money laundering. Money laundering (which is illegal!) is when someone disguises money from criminal activity as funds coming from a legitimate source.

For example, a criminal could use their cash-intensive restaurant as a front for illegal activities. How? They could make it look like the restaurant is receiving substantial cash payments when it’s really from illegal activity.

Red flags of cash-intensive business money laundering include:

- Higher-than-normal cash income compared to other similar businesses in the area (money laundering)

- More frequent transactions

IRS cash-intensive business audit process

The IRS provides a cash-intensive business audit guide so businesses can get an idea of what the audit process is like.

During a cash-intensive business audit, the IRS conducts a detailed interview, analysis, and evaluation.

Among other processes, the IRS:

- Interviews the individual or business to get an overall financial picture, understanding of operations, and overview of recordkeeping practices

- Finds out how the individual or business handles incoming and outgoing cash

- Asks about cash-on-hand that the individual or business has access to

- Inquires about mixing business and personal accounts

- Requests detailed financial information, including loans, accounts payable, and holdings in stocks

- Uses analytical tests to determine if the individual or business accurately reported income

- Tours the business to find out how it operates (and document each step)

- Compares cash register tapes from the day of the tour to the audit period

- Evaluates the individual’s or business’s internal controls

- Reconciles reported income on the tax return to books and records

- Tests the income recorded in accounting books by tying in the original documents (e.g., invoice)

- Analyzes bank accounts, business ratios, and e-commerce activity

- Evaluates facts and findings to corroborate or refute the individual’s or business’s claims

Additionally, the IRS has cash-intensive audit guide chapters for specific industries, including beauty shops, car washes, and convenience stores.

For more information on cash-intensive business audits, consult the IRS’ Audit Techniques Guide (ATG).

How to stay compliant

Whether you run a cash-intensive business or not, you need to keep up-to-date, accurate accounting records.

Stephen Light, CMO and Co-Owner of Nolah Mattress, advises:

Cash-intensive businesses of any size can stay ready for an IRS audit by being diligent about internal controls, such as making sure more than one person is taking care of financial bookkeeping; more eyes equals less opportunity for mistakes. Recordkeeping is far more difficult for cash-intensive businesses, but establishing internal controls early—making use of accounting software helps lessen the load—can save businesses from having to give endless oral testimony should the IRS choose to audit.”

To keep your cash-intensive business compliant and prepared in case of an IRS audit, you should:

- Record each transaction (i.e., the date, amount, and item or service)

- Stick to your accounting method (e.g., cash-basis, modified cash-basis, or accrual accounting)

- Use a cash drawer and balance it every day or after every shift

- File Form 8300 if a customer pays over $10,000 in cash in one transaction or two or more related transactions

- Separate personal and business funds (e.g., open a separate business bank account)

- Hang onto records, including:

- Cash receipts

- Copies of customer receipts

- Bank and credit card statements

- Invoices

- Bills

- Tax returns

- Forms W-2, 1099-MISC, and 1099-NEC

When in doubt, retain the record. Consider keeping digital records to stay organized and secure. And to streamline your accounting responsibilities, sign up for accounting software.

This is not intended as legal advice; for more information, please click here.