If you paid a person that is not an independent contractor during the tax year, you might need to file Form 1099-MISC. So, what is Form 1099-MISC?

What is Form 1099-MISC?

Form 1099-MISC, Miscellaneous Information, is an information return businesses use to report miscellaneous payments.

Before 2020, business owners also reported nonemployee compensation on Form 1099-MISC. But now, business owners must use Form 1099-NEC to report nonemployee compensation.

Form 1099-MISC recipients

File Form 1099-MISC for each person you have given the following types of payments in the course of your business during the tax year:

- At least $10 in royalties or broker payments in lieu of dividends or tax-exempt interest

- At least $2,000 (beginning in tax year 2026; was previously $600 or more) in the following:

- Rents

- Prizes and awards

- Other income payments

- Cash from a notional principal contract to an individual, a partnership or an estate

- Any fishing boat proceeds

- Medical and health care payments

- Crop insurance proceeds

- Cash payments for fish

- Payments to an attorney

- Section 409A deferrals

- Nonqualified deferred compensation

Again, do not use Form 1099-MISC to report nonemployee compensation. Instead, use Form 1099-NEC for independent contractor payments. And as always, don’t use a 1099 form for W-2 employees.

Check out the IRS 1099 instructions for a list of payments that you should report on Form 1099-MISC.

Filling out Form 1099-MISC

When filling out Form 1099-MISC, include:

- Your name, address, and phone number

- Your TIN (Taxpayer Identification Number)

- Recipient’s TIN

- Recipient’s name and address

- Your account number, if applicable

- Amount you paid the recipient in the tax year

For more information about filling out Form 1099-MISC, check out the IRS’s Instructions.

Filing Form 1099-MISC

After you finish filling out Form 1099-MISC, make sure you send the correct copies to the IRS and the recipient. You must also send Form 1096, Annual Summary and Transmittal of U.S. Information Returns, to the IRS. Form 1096 is a summary form of IRS Forms 1099-MISC.

You can either mail or e-File Forms 1099-MISC. You must e-File if you need to file 250 or more information returns throughout the year.

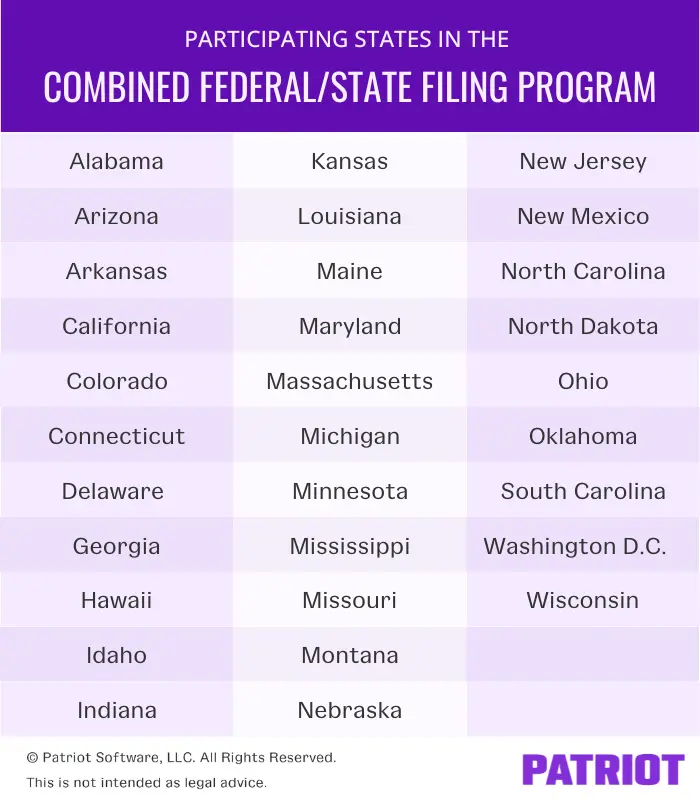

If your state participates in the Combined Federal/State Filing Program (CF/SF), the IRS will send your e-Filed 1099 forms to your state.

Check out a list of states that participate in CF/SF below:

Form 1099 due date

You are responsible for distributing and filing Form 1099-MISC by the correct due date.

If you are filing a paper form, your Form 1099-MISC due date is March 1. If you file the form electronically, your due date is March 31. You must send the recipient their copy no later than February 1.

Form 1099-MISC copies

You must distribute multiple copies of Form 1099-MISC to various recipients. Here’s a breakdown of where you need to send each copy of Form 1099-MISC:

- Copy A: The IRS

- Copy 1: State tax department, if applicable

- Copy B: Recipient (vendor)

- Copy 2: Recipient (vendor)

- Copy C: Keep in your business records

Where to get Form 1099-MISC

You can view a sample of Form 1099-MISC on the IRS’s website. However, the sample is only for viewing. Do not print and/or file Form 1099-MISC from the IRS’s website.

Order official 1099-MISC forms either online from the IRS or from another authorized retailer. Make sure the forms you order are for the correct tax year.

Form 1099-MISC errors

Nobody’s perfect, so if you make a mistake on Form 1099-MISC, don’t worry. Instead, make sure you correct the error as soon as possible.

There are two types of errors you can make:

- Type 1

- Type 2

Type 1 errors include things like incorrect money amounts, codes, or checkboxes. Type 2 errors include a missing or incorrect TIN or payee name.

How you fix the issue depends on whether the error is a Type 1 or Type 2 error. Be sure to learn how to issue a corrected Form 1099 so you can quickly fix the error.

If you need to make a correction to an e-Filed Form 1099-MISC, check out IRS Publication 1220. If you made a mistake, you would either need to make a One-transaction Correction or a Two-transaction Correction.

Looking for an easy way to track vendor payments? Patriot’s accounting software lets you streamline the way you record payments, expenses, and income. Start your free trial today!

This article was updated from its original publication date of October 13, 2011.

This is not intended as legal advice; for more information, please click here.