If you have nonexempt employees, you have to pay them overtime, or time and a half, for any hours worked over 40 during the workweek. Learn all about time and a half, who qualifies for overtime, and how to calculate time and a half when running payroll.

What is time and a half?

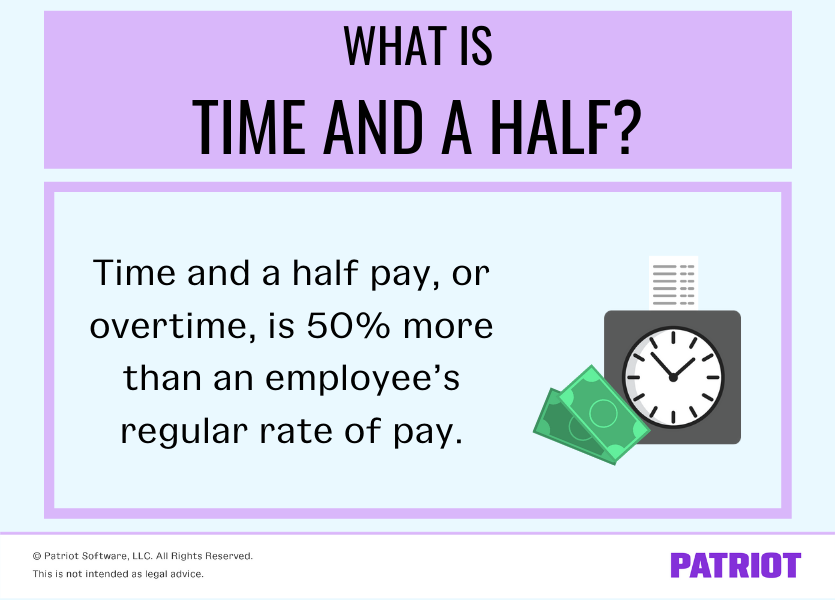

Time and a half is overtime compensation where certain employees receive 1.5 times their normal hourly wage for each hour worked beyond 40 hours in a workweek.

Time and a half may also be called overtime, overtime rate of pay, or an overtime premium.

The Fair Labor Standards Act (FLSA) regulates overtime. The FLSA requires that you pay time and a half to qualifying employees who work more than 40 hours in a workweek. But there are also overtime laws by state that may be stricter. For example, California requires that employers pay time and a half if nonexempt employees work more than eight hours in a workday.

How much is time and a half? Time and a half pay is 50% more than an employee’s regular rate of pay, or 1.5. For every hour of overtime an employee works, you must give them their regular rate of pay plus half of that.

To calculate an employee’s overtime rate of pay, multiply their regular rate by 1.5. Payroll software automatically calculates overtime based on hours worked.

Not all employees receive overtime pay. An employee’s ability to receive time and a half depends on whether they are exempt or nonexempt.

Who receives time and a half pay?

Only nonexempt employees receive time and a half. Exempt employees are exempt from the FLSA and its overtime pay requirements.

So, how do you know if an employee is exempt vs. nonexempt? Exempt vs. nonexempt varies depending on if the employee is hourly or salaried, the salary amount received, and the employee’s job duties.

Exempt employees:

- Make at least $35,568 annually ($684 per week)

- Receive a salary, AND

- Have job duties that are considered exempt

Nonexempt employees:

- Don’t make at least $35,568 annually

- Are not salaried AND/OR

- Do not have exempt job duties

An employee must meet all three requirements to be considered exempt. If an employee does not meet one or more of these requirements, they are nonexempt.

Exempt job duties include high-level responsibilities that directly affect the company’s overall operations, such as executive, administrative, professional, or computer-based duties.

Additionally, if you pay an employee an annual salary of $107,432 or more, they are exempt if they have at least one executive, administrative, or professional job duty.

There is also a test for employees who work in outside sales. If an employee’s primary duty is making sales, they are exempt. The employee must also regularly perform work away from your business. They do not have to meet salary exemption requirements to be exempt.

There’s a common misconception that paying an employee a salary means they’re exempt from overtime wages. You can have salaried nonexempt employees who are eligible for overtime pay.

Your state may have stricter overtime laws than the FLSA. Check with your state to learn about the overtime laws you need to follow.

How do you calculate time and a half?

If you have nonexempt employees, you must pay them time and a half (1.5 times) for any hours worked over 40 a week. Again, online payroll can handle this calculation for you. Or, you can calculate time and a half yourself.

A good chunk of nonexempt employees receive hourly wages instead of a salary. However, because nonexempt employees can be salaried, you must know how to calculate time and a half for both salaried and hourly employees.

Keep in mind that, like regular wages, you must withhold and remit taxes on overtime pay after you calculate it. You can use payroll services to streamline this process.

How to calculate time and a half for hourly employees

Let’s say you have a nonexempt hourly employee who earns $12 per hour. During the last workweek, the employee worked 45 hours (40 regular hours + 5 overtime hours).

How to calculate time and a half for hourly employees (with example):

- Calculate the employee’s regular earnings

To find the employee’s regular earnings, multiply their regular pay rate ($12) by 40 hours.

$12 X 40 = $480 in regular wages - Find the time and a half pay rate

Next, calculate the employee’s time and a half pay rate. Multiply 1.5 by the employee’s regular rate of pay.

1.5 X $12 = $18 per hour of overtime - Multiply the time and a half rate by the number of overtime hours

Multiply the time and a half rate from Step 2 ($18) by the number of overtime hours the employee worked during the week.

$18 X 5 = $90 of overtime pay - Add together the regular and overtime wages

Add the employee’s regular wages and overtime pay together to find the employee’s total wages.

$480 regular wages + $90 overtime pay = $570 in gross wages

If your employee has multiple pay rates for different jobs within your company, you must calculate weighted overtime for their wages.

How to calculate time and a half for salaried employees

When it comes to calculating time and a half for salaried employees, there are two methods you can use.

The method you use depends on if the employee receives a salary that covers a fixed number of hours or if they receive a salary that covers all worked hours (aka fluctuating workweek).

1. How to calculate time and a half for salary employees with fixed hours

For a salaried employee with fixed hours, use these steps:

- Calculate the employee’s regular hourly rate

- Calculate the employee’s regular earnings

- Find the time and a half pay rate (1.5 x Regular Hourly Wage)

- Multiply the overtime rate by the number of overtime hours

- Add together the regular and overtime wages

Say your salaried employee earns $1,000 per week. You expect the employee to work 34 hours this week, but they wind up working 45.

Find the employee’s regular hourly rate. Divide the employee’s salary by the number of hours you expected the employee to work (34 hours).

$1,000 / 34 hours = $29.41

Calculate the employee’s regular wages using the rate from above. Multiply the hourly rate by 40 to get the employee’s total regular wages.

$29.41 X 40 hours = $1,176.40

Next, find the employee’s overtime rate by multiplying their regular hourly rate by 1.5.

$29.41 X 1.5 = $44.12

Multiply the employee’s overtime hours by the overtime rate of $44.12.

$44.12 X 5 hours = $220.60

Finally, add together the salaried employee’s regular and overtime wages to get their total gross pay for the period.

$1,176.40 + $220.60 = $1,397

Your employee’s gross wages for the period are $1,397.

2. How to calculate time and a half for salary employees with all hours worked

Calculate all hours worked the same way you would calculate fluctuating workweek overtime. Employees who work a fluctuating workweek work a different number of hours from week to week.

Say your employee earns $1,000 a week and their salary covers all hours worked, no matter how many hours they work. The employee worked 48 hours this week.

Calculate the employee’s regular hourly rate by dividing the weekly salary by the total number of hours worked.

$1,000 / 48 hours = $20.83

Because you already accounted for the overtime hours once in the regular hourly rate, you must multiply the regular rate of pay by 0.5 instead of 1.5.

$20.83 X 0.5 = $10.42

Multiply your employee’s overtime hours (8 hours) by their overtime hourly rate ($10.42).

$10.42 X 8 hours = $83.36

As usual, add together the employee’s overtime and regular wages to get their total gross pay for the period.

$1,000 + $83.36 = $1,083.36

Your employee earned $1,083.36 in gross wages for the period.

Time and a half pay FAQs

Time and a half is overtime compensation paid to certain employees who work overtime hours, typically hours beyond 40 in a workweek.

Time and a half is 1.5 times an employee’s regular hourly wage, or 50% more than their regular wages.

No. Only nonexempt employees are eligible to receive time and a half pay.

Multiply the employee’s regular hourly wage by 1.5.

The Fair Labor Standards Act (FLSA) regulates time and a half at the federal level.

Yes. Several states have overtime laws that are stricter than the FLSA.

Yes.

This article was updated from its original publication date of November 23, 2014.

This is not intended as legal advice; for more information, please click here.