Offering a retirement plan comes with a host of benefits, including generous 401(k) tax credits, while also serving as a potent tool for recruiting and retaining top talent. There are also unique benefits that come from integrating your 401(k) plan with your payroll provider.

However, plans are most effective when they help employees save for their golden years without adding to their daily stressors. Fortunately, there are several retirement plan features that can make saving easier for employees, increase participation, and boost recruitment.

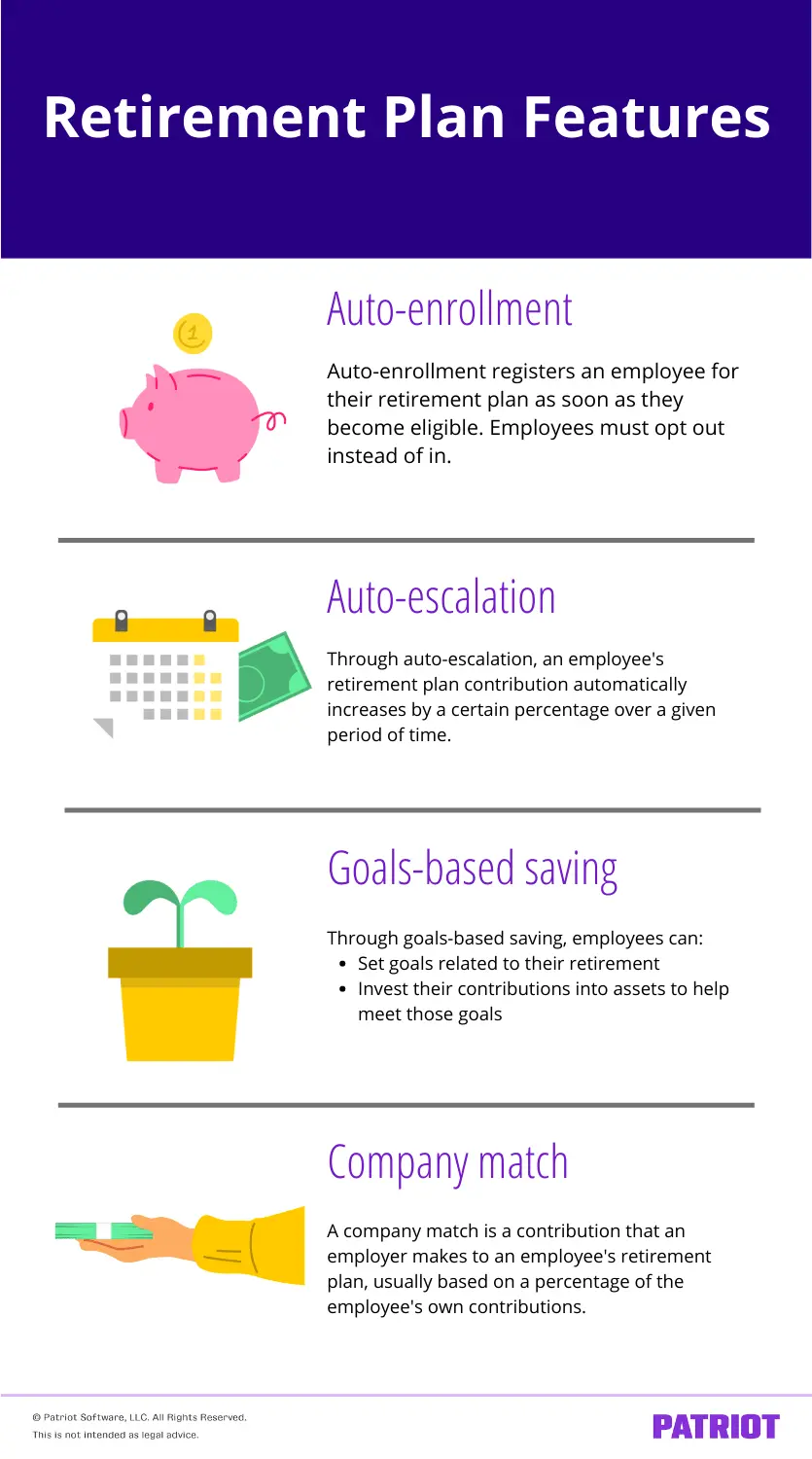

- Auto-enrollment signs employees up automatically, increasing participation while allowing opt-out if they prefer.

- Auto-escalation raises contributions annually, helping employees boost savings steadily until reaching a set cap.

- Company match boosts employee savings with employer contributions, improving recruitment and offering potential tax credits.

Retirement plan features

From auto-enrollment to a company match, here are some of the top retirement plan features that can simplify things for both employers and employees.

1. Auto-enrollment

Auto-enrollment is an increasingly popular feature to include in one’s plan. Vestwell’s Report found that 31% of employers who made a change to their plan in 2023 introduced auto-enrollment.

So, what’s the big deal with auto-enrollment? Auto-enrollment registers an employee for their retirement plan as soon as they become eligible. That way, employees can opt out of plans instead of opting in.

Keep in mind that auto-enrollment plan features might frustrate or surprise some employees. Talk with your team about adding an auto-enrollment plan feature so they know to opt out, if desired.

2. Auto-escalation

Through an auto-escalation plan, an employee’s contribution to their retirement plan automatically increases by a certain percentage over a given period of time. Generally, this starts at the beginning of each year.

So what does this look like in action? Take the example of an employee who contributes 3% of their salary to their retirement plan. With a standard auto-escalation plan, their contributions increase by 1% each year until reaching their plan’s escalation cap, which is typically 10% – 15% of their salary. So in the first year, they would contribute 3% of their salary, then 4% in the next year, then 5%, and so on, until capping out at 10%.

| Year of Participation | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| % of Salary Contributed | 3% | 4% | 5% | 6% | 7% | 8% | 9% | 10% | 10% |

Like auto-enrollment, auto-escalation can help employees build their retirement savings without needing to monitor their contributions daily.

3. Goals-based saving

Through goals-based saving, employees can:

- Set goals related to their retirement

- Invest their contributions into assets that can help meet those goals

Generally, employees will answer questions regarding their compensation, retirement aims, income goals, and risk tolerance. Then, the goals-based saving plan allocates their contributions into investments tailored to meet their unique goals.

Goals-based saving plans also automatically update due to response to shifting market conditions or to changes the employee provides.

It’s important to note: goals-based saving accounts can come with an additional fee. This fee is levied because of the additional services provided by the goals-based plan. Before signing up for goals-based saving, one should be aware of their financial situation and ensure that opting into this feature aligns with your goals and expectations.

4. Company matches & contributions

The “company match” is one of the most popular retirement plan features. Essentially, a company match is a contribution made by an employer to an employee’s retirement plan, usually based on a percentage of the employee’s own contributions.

Say an employer offers a 50% company match, up to 4% of an employee’s salary. Under this plan, if an employee contributed 4% of their salary to their retirement plan, the employer would contribute an additional 2% of the employee’s salary, for a “total” contribution of 6%. However, if the employee had contributed 5% of their salary to their retirement plan, the employer would still make a 2% contribution, because their contributions only match up to 4% of the employee’s salary.

Varying plan types have different rules for company matches. As always, consult with an accountant or trusted advisor before making a change to your retirement plan benefit.

Make retirement plans even easier with Vestwell

Patriot and Vestwell have partnered to offer affordable retirement plans for small businesses across the United States. Vestwell’s digital retirement platform directly integrates with Patriot’s payroll software, making it easier for you to offer and administer a company-sponsored 401(k). By combining technology with best-in-class retirement plans, Vestwell has created custom programs for Patriot customers that are affordable and easy to set up and use.

Additionally, some benefits may also come with sizable tax credits for the businesses offering them. If you are an employer interested in setting up a 401(k) account for your business, you can explore our partnership with Vestwell here.

This is not intended as legal advice; for more information, please click here.