Navigating through the waters of health insurance coverage is tricky. You might be wondering, Do employers have to offer health insurance? Although the Affordable Care Act (ACA) requires employers with 50 or more full-time equivalent employees to provide health insurance, no employer has to offer excepted benefits.

But, many employers do offer excepted benefits.

What does this all mean? Should you jump on board and offer excepted benefits to your crew? To make that kind of decision, you need to know what is an excepted benefit and what the new Excepted Benefit HRA is.

What are excepted benefits?

Excepted benefits under ACA are types of coverage that are not included in a traditional health insurance plan.

The Affordable Care Act requires that a traditional health insurance plan covers the following health benefits:

- Ambulatory patient services

- Emergency services

- Hospitalization

- Pregnancy, maternity, and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Rehabilitative and habilitative services and devices

- Laboratory services

- Preventive and wellness services

- Pediatric services, including oral and vision care for children

As you can see in the above list, there are a few benefits not included (e.g., vision coverage for adults).

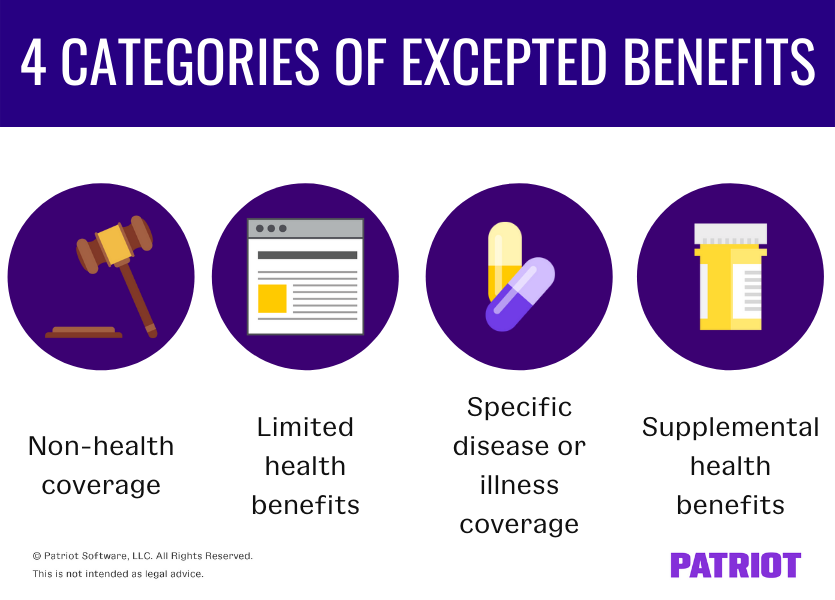

There are four categories of excepted benefits, according to the Department of Labor:

- Non-health coverage

- Limited health benefits

- Specific disease or illness coverage

- Supplemental health benefits

Non-health coverage

The first category of excepted benefits under ACA include benefits that are not considered health care coverage.

These benefits are add-ons to regular health insurance coverage. Typically, these benefits pay out wage replacement and may incidentally cover medical care coverage after an accident or extended illness or injury. However, they do not cover general health care costs for employees who get sick.

Examples of coverage included under this category of excepted benefits include:

- Accident-only coverage (e.g., automobile or accidental death and dismemberment insurance)

- Disability insurance

- Workers’ compensation insurance

Limited health benefits

Limited health benefits are offered separately from traditional health care plans. These benefits are not required under the ACA and include:

- Dental coverage

- Vision coverage

- Long-term care benefits (e.g., nursing home)

Specific disease or illness coverage

The third category of excepted benefits covers types of benefits that are specific to a certain type of illness or disease. This type of coverage has no coordination with benefits under a group health plan.

Examples of this category of excepted benefits include:

- Coverage for a specific disease or illness (e.g., cancer insurance)

- Hospital indemnity (insurance that pays the holder if they are hospitalized)

Supplemental health benefits

The last type of excepted benefits category includes separate insurance policies that are supplemental to Medicare or Armed Forces health care coverage.

In rare circumstances, this category may also include separate insurance policies that are supplemental to a group health plan.

Excepted Benefit HRA

Since January 2020, employers can choose to offer employees an Excepted Benefit HRA. If you offer it, your employees must enroll during open enrollment.

An Excepted Benefit HRA is one of two types of HRAs with the other being the Individual Coverage HRA (ICHRA).

Whereas the ICHRA is an alternative to traditional group-term health insurance, the Excepted Benefit HRA is something employers can offer in conjunction with traditional health insurance.

Can you offer the Excepted Benefit HRA?

If you want to offer employees the Excepted Benefit HRA as part of your employee benefits package, you must also offer them a traditional health insurance plan.

However, the employee does not have to enroll in the traditional health insurance plan to enroll in the Excepted Benefit HRA. You just have to offer it.

What do Excepted Benefit HRAs cover?

Excepted benefit HRAs cover things not included in a traditional health insurance plan, including:

- Dental coverage

- Vision coverage

- Short-term, limited-duration insurance (STLDI)

- Copays, deductibles, and other expenses not covered by a primary health insurance plan

2026 Excepted benefit contribution limit

Employers contribute to an Excepted Benefit HRA. But, you can only contribute up to a certain amount for each employee.

For 2026, the annual contribution limit for an Excepted Benefit HRA is $2,200.

Excepted Benefit HRA vs. regular HRA

So, what’s the difference between an Excepted Benefit and HRA that reimburses excepted benefits?

Unlike regular HRAs, Excepted Benefit HRAs can reimburse employees for medical care expenses that are not considered excepted benefits.

If you have employees, you need a reliable way to run payroll. Patriot’s online payroll uses a simple three-step process. Plus, we offer free setup and support to get you going and help you along the way. Explore our award-winning software with your free trial today!

This article has been updated from its original publication date of November 11, 2019.

This is not intended as legal advice; for more information, please click here.