Attention Oregon employers! Specifically, attention employers in Eugene, Oregon. Do you know about the Eugene-specific payroll tax? Learn all about the Eugene Community Safety Payroll tax and whether or not you need to withhold and remit it to the city.

What is the Eugene Community Safety Payroll Tax?

The Eugene Community Safety Payroll (CSP) tax is a special payroll tax that both employees and employers have to pay. And, self-employed individuals must pay CSP tax.

The Eugene CSP tax provides long-term funding for community safety services. The Community Safety Payroll tax went into effect on January 1, 2021.

Currently, the Eugene CSP tax is not permanent. After seven years, the Eugene city council must allow the public to vote on whether or not to keep the Eugene community tax.

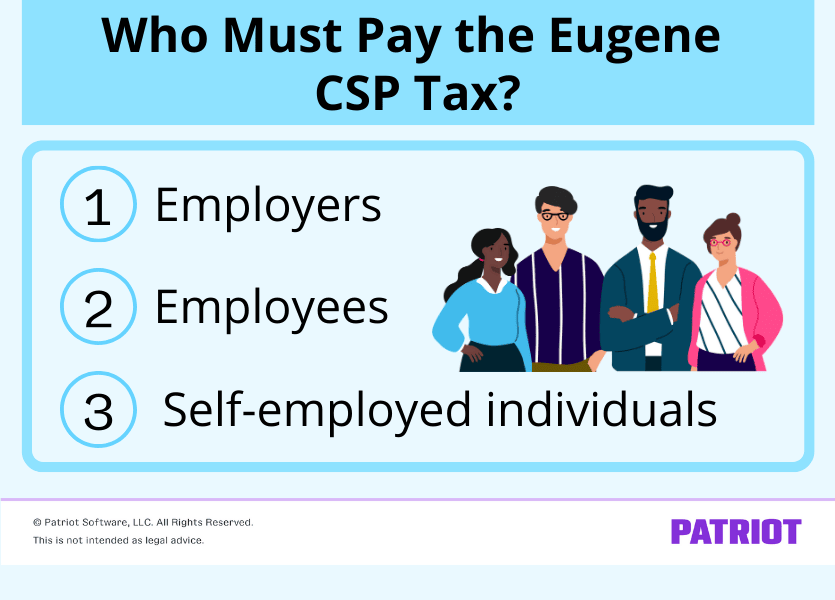

Who must pay the Eugene CSP tax?

As mentioned, both employees and employers must pay the tax as well as self-employed individuals. Take a look at who is responsible for paying the Eugene CSP tax and what wages are taxed:

- Employer: Applied to total wages paid by an employer with a physical address in the Eugene city limits.

- Employee: Applied to total wages paid to an employee working for an employer located in the Eugene city limits.

- Self-employed: Applied to the net earnings from self-employed individuals with a physical address in the Eugene city limits.

Employers are responsible for paying the employer payroll tax as well as withholding and remitting the employee payroll tax portion. Self-employed individuals are responsible for paying the self-employment Eugene payroll tax.

In addition, nonprofit 501(c)(3) organizations are subject to both the employer and employee payroll tax.

Who is exempt?

According to the city of Eugene, public employers are exempt from the employer payroll tax because intergovernmental taxation is prohibited.

Wages earned at minimum wage are exempt from the employee payroll tax (even if the employee receives overtime pay).

Also, wages earned from the following jobs are not subject to the Eugene payroll tax:

- Domestic service in a private home

- Casual labor not in the course of the employer’s trade or business

- Seasonal labor in connection with the planting, cultivating or harvesting of agricultural crops

Wages that are not subject to withholding under Oregon Revised Statute (ORS) Chapter 316 are also exempt from the Eugene CSP tax.

What is the tax rate?

The Eugene CSP tax rate depends on if you’re an employer, an employee, or a self-employed individual.

For employers, the tax rate varies depending on how many employees you have. Here are the employer rates:

- Employers with 1 – 2 employees: 0.0015, or 0.15% for the first $100,000 of wages paid (e.g., salaries, fees, tips, bonuses, etc.)

- Employers with more than 2 employees: 0.0021 (or 0.21%) of total wages paid

For employees, the tax rate is determined using annualized income tax rate charts divided by pay period, based on the hourly wage rates provided in the ordinance. The employee payroll tax is applied to total wages, after pre-tax deductions. Here are the employee rates between July 1, 2025 and June 30, 2026:

- Employees who make more than $31,304 per year: 0.0044, or 0.44% of total wages

- An employee who earns less than $31,304 per year: Exempt from the Eugene employee payroll tax

For more information, check out the City of Eugene’s tax rate charts.

When is the tax due?

Pay the employer and employee Eugene payroll tax on a quarterly basis. Quarterly returns and payments are due on or before the last day of the month following the end of the quarter.

| Quarter | Due Date |

|---|---|

| Quarter 1 (January – March) | April 30 |

| Quarter 2 (April – June) | July 31 |

| Quarter 3 (July – September) | October 21 |

| Quarter 4 (October – December) | January 31 |

What are the penalties for filing or paying late?

For any tax not paid by the due date of the return, you will owe a 5% late-payment penalty.

If you file your return more than 30 days after the due date (including an extension for the self-employment tax return), you will receive a 20% late-filing penalty.

If you do not file your return for 12 consecutive quarters (three years for annual returns), you may be subject to a 100% penalty.

Employers who knowingly fail to withhold and deduct the Eugene payroll tax could be subject to a penalty of $250 per employee, up to $25,000 for each tax period. This penalty is in addition to other penalties or interest.

Interest is charged on any unpaid tax if you don’t pay the tax by the quarterly due date. The interest period begins the day after the tax is due on all unpaid tax until the tax is paid.

How to register online for Eugene CSP tax

If you are an employer or self-employed individual with a physical address in the Eugene city limits and subject to the CSP tax, register with the city online. To register, follow the steps below:

- Go to the MUNIRevs website

- Select “New User”

- Complete the user profile to set up your account

- Register your business or businesses

After you register online, you’ll be able to file tax returns and make payments electronically. For more information about the new payroll tax, check out the City of Eugene’s website.

Calculating Eugene CSP tax: Example

Say you only have one employee, and you pay them $37,000 per year. As a reminder, employers with only one or two employees have a CSP employer tax rate of 0.15% (on the first $100,000 wages paid). And, employees who make more than $31,304 per year have an employee rate of 0.44% of total wages.

Your employee works 40 hours per week and gets paid weekly. Take a look at how much you and your employee would pay into the Eugene CSP tax each week.

First, find the employee’s weekly gross wages by multiplying their hourly rate by the number of hours they work in the period.

Employee gross wages = $37,000 / 52 weeks

Employee gross wages = $711.54

Next, find how much you need to withhold in Eugene CSP tax from the employee’s wages.

$711.54 X 0.0044 = $3.13 for employee payroll tax

Finally, calculate how much you need to pay in CSP tax as an employer.

$711.54 X 0.0015 = $1.07 for employer payroll tax

Each week, withhold $3.13 from employee wages and set aside $1.07 for the employer portion of the Eugene CSP tax.

Calculating payroll taxes can be tricky. With Patriot’s online payroll software, you don’t have to worry about computing payroll taxes yourself. And, we offer free, USA-based support. Get your free trial today!

This article has been updated from its original publication date of December 28, 2020.

This is not intended as legal advice; for more information, please click here.