Depending on your business’s location, you may need to pay or remit certain state-specific taxes. One type of state tax your business should be aware of is gross receipts tax (GRT). Read on to learn about gross receipts tax and whether or not you’re responsible for remitting it to your state.

What is a gross receipts tax?

What is gross receipts tax, anyways? Before we can get to that question, you have to know what gross receipts are.

Gross receipts include your business’s total revenue without deductions like operating expenses and discounts. Basically, gross receipts are the total amount of revenue your business collects during the year.

Gross receipts tax is a tax some businesses must pay on their gross receipts. Unlike sales tax, gross receipts tax is not typically paid by the consumer (e.g., at the point of sale). However, GRT can be imposed on consumers in some areas.

Some states levy gross receipts tax instead of corporate income tax. However, some states have both types of taxes. Like corporate income tax, gross receipts tax generally varies from state to state. If your state imposes a gross receipts tax, you are responsible for paying a GRT rate (e.g., 0.23%) on your business’s revenue.

In short, your business’s GRT liability typically depends on:

- Your state

- Type of business

- How much revenue your company earns

Although not common, some states (e.g., New Mexico) impose gross receipts tax on customers at the point of sale (similar to sales tax). And other states, like Hawaii, impose a tax similar to GRT called general excise tax (GET) on every transaction.

States with gross receipts tax

At this point, you’re probably wondering, What are the states with gross receipts tax? Glad you asked…

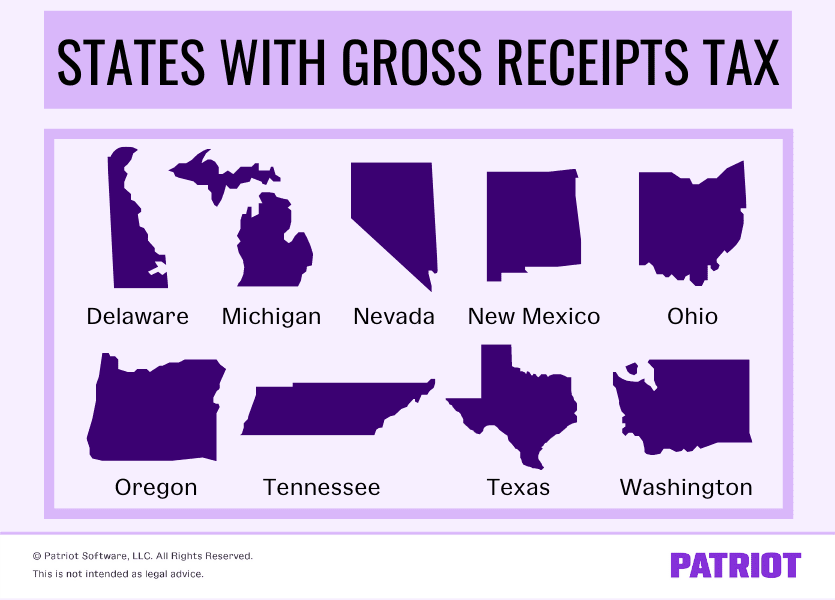

Unlike some other types of taxes, not every state requires businesses to pay GRT. In fact, only nine states impose some kind of GRT. The states that levy gross receipts tax include:

- Delaware

- Michigan

- Nevada

- New Mexico

- Ohio

- Oregon

- Tennessee

- Texas

- Washington

Keep in mind that the above list may expand over time. More states are considering imposing gross receipts tax.

Again, gross receipts tax rates and rules can vary depending on the state. To get the scoop on what each of the states require, keep reading.

Delaware

According to Delaware’s Division of Revenue, any company that is “engaged in business” in the state must have a business license and pay GRT. You must pay the tax if you sell goods or provide services in Delaware. Depending on the business’s activity, gross receipts tax rates can range from 0.0945% to 0.7468%.

If your business does not have a physical presence within the state (e.g., sends orders to customers in Delaware via mail), you are not responsible for paying GRT.

Delaware gross receipts tax is due either monthly or quarterly, depending on your lookback period. If you’re a monthly filer, your GRT is due on or before the 20th day of each month. Quarterly filers must remit their GRT to the state on or before the last day of the first month following the close of the quarter.

You can file the Delaware Gross Receipts Tax form online. Or, you can print and mail a paper form to the state. Log into your Delaware account online to access and print your paper form.

Michigan

The Michigan Business Tax (MBT) imposes a 4.95% business income tax and a modified gross receipts tax rate of 0.8%.

Any business that has substantial nexus (or presence) in Michigan is subject to the modified gross receipt tax if:

- They have a physical presence in Michigan for more than one day during the tax year OR

- If the taxpayer actively solicits sales in Michigan and has gross receipts of $350,000 or more

A taxpayer whose gross receipts are less than $350,000 does not need to pay the Michigan gross receipts tax.

To register for the MBT, use the Michigan Treasury Online portal.

For more information about the Michigan Business Tax, check out the state’s FAQs and website.

Nevada

The Nevada Department of Taxation states that all businesses with gross revenue exceeding $4,000,000 in the taxable year are required to pay Nevada gross receipts tax, or Commerce Tax. Certain entities, such as nonprofits, are exempt from the tax. Check out Nevada’s website for a complete list of exempt entities.

Your Nevada GRT rate depends on what business category your company falls under (NAICS code). Most businesses have a rate between 0.05% and 0.3%. Retail trade companies have a tax rate of 0.111%.

To register for the Nevada Commerce Tax, fill out a Nexus Questionnaire and mail it to the Nevada Department of Taxation.

The Commerce Tax return is due 45 days after the end of the fiscal year (June 30). If the 45th day falls on a holiday or weekend, the return is due on the next business day.

Use Form TXR-030.01 to file your Nevada Commerce Tax return. You can either e-File your return online or mail a hard copy to the state.

New Mexico

New Mexico’s sales tax is referred to as gross receipts tax. In New Mexico, businesses are responsible for imposing this tax on customers. And as the business owner, you must collect and remit the New Mexico GRT to state tax agencies.

In some cases, New Mexico’s GRT is already included as a part of the selling price.

In most cases, sales and leases of goods and property (tangible and intangible) are taxable. Unlike a number of other states, sales and performances are taxable in New Mexico.

For businesses in New Mexico, gross receipts tax is based on the business location.

The state gross receipts tax rate in New Mexico is currently 5.125%. However, depending on your locality, the GRT rate can be as high as 9.4375%.

For more information about New Mexico’s GRT, check out New Mexico’s Taxation & Revenue Department’s website.

Ohio

Ohio’s gross receipts tax is called the Commercial Activity Tax (CAT). It is an annual tax Ohio imposes on many businesses, including retail, wholesale, service, and manufacturing. This includes sole proprietorships, LLCs, S Corps, corporations, disregarded entities, trusts, and all other types of businesses.

Businesses with Ohio taxable gross receipts of $150,000 or more per calendar year must register for the CAT, file returns, and make payments to the state. Some businesses, such as nonprofit organizations, are exempt from Ohio’s CAT.

An out-of-state person is also required to register and pay the CAT if they have “bright-line” presence in Ohio (aka, nexus). You have bright-line presence if you have:

- At least $50,000 in property for a calendar year

- $50,000 or more in payroll in the state in a calendar year

- $500,000 or more taxable gross receipts in Ohio

- 25% or more of your total property, payroll, or gross receipts in Ohio

- Been domiciled in the state

For calendar years 2006 and later, taxpayers with $1,000,000 or less in taxable gross receipts must pay a minimum of $150 in CAT annually. The state taxes taxable gross receipts above $1,000,000 at 0.26%. You can find a list of rates on Ohio’s Department of Taxation website.

The due dates for the CAT vary depending on how much your business makes. If you make $150,000 – $1,000,000 in Ohio gross receipts, the tax is due on May 10 each year. If you make more than $1,000,000 in gross receipts, you must pay on a quarterly basis on May 10, August 10, November 10, and February 10.

Businesses that file the Ohio CAT must use the Ohio Business website to electronically file and pay the tax. You can also use CAT Telefile to electronically file and pay your Ohio gross receipts tax.

Oregon

Like Ohio, Oregon also has a CAT (Corporate Activity Tax). Businesses must pay Oregon’s CAT if they do business in the state. This includes all types of business entities (e.g., S Corp, LLC, etc.). Some items are exempt from CAT, including things like motor vehicle fuel sales, retail sales, and wholesale of groceries.

Oregon has four thresholds that determine whether a business or unitary group is responsible for the CAT. The thresholds depend on the amount of commercial activity the business or group has during the year. Check out Oregon’s CAT thresholds:

- Less than $750,000 (in sales): No CAT requirements.

- $750,000+: Businesses or unitary groups must register for the CAT.

- $1,000,000: Business or unitary group must file a return.

- More than $1,000,000: Business or unitary group must file a return and pay CAT.

Register your business for Oregon gross receipts tax within 30 days of meeting the $750,000 threshold. Failing to register can result in a penalty of $100 per month, up to $1,000 per calendar year.

Only taxpayers with more than $1,000,000 of taxable Oregon commercial activity must pay. The Oregon CAT rate is $250 plus 0.57% of your taxable commercial activity.

The Oregon CAT is an annual tax. CAT returns are due each year on April 15. Estimated payments are due April 30, July 31, October 31, and January 31 for the preceding quarter. You must make estimated payments to the state if you expect more than $5,000 of CAT liability for the calendar year.

You can pay estimated Oregon Corporate Activity Tax online or via mail using an OR-CAT-V.

Tennessee

All businesses must pay Tennessee gross receipts tax, or “business tax,” if they make more than $10,000 in sales in any Tennessee county and have substantial nexus in the state. This can include a company with a physical business location in the state as well as out-of-state businesses performing certain activities in Tennessee.

If you’re in-state and have gross receipts of more than $3,000 but less than $10,000, you must obtain a minimal activity license from your county. If your gross receipts exceed $10,000, you must get a standard business license. You cannot operate until you have the proper license.

Register your for the Tennessee Business Tax online through the Tennessee Taxpayer Access Point (TNTAP).

The amount of gross receipts tax you pay depends on your business’s classification. To determine your company’s classification, look at the business tax classification guide. After you find your classification, check out the Tennessee’s Department of Revenue to find your rate.

Your tax return is due on the 15th day of the fourth month following the end of your fiscal year (e.g., April 15 if your fiscal year coincides with the calendar year).

You can either electronically file your tax return or mail it to the state using Form BUS428. To file and pay your gross receipts tax online, use the online portal (TNTAP).

Texas

The Texas gross receipts tax is called Texas Franchise Tax. According to the Texas Comptroller, “each taxable entity formed in Texas or doing business in Texas must file and pay franchise tax.” This includes entities like corporations, S corporations, LLCs, partnerships, business associations, and more.

The following entities are exempt from filing and paying the Texas Franchise Tax:

- Sole proprietorships (except for single-member LLCs);

- General partnerships when direct ownership is made entirely of natural persons (except for limited liability partnerships)

- Entities exempt under Tax Code Chapter 171, Subchapter B

- Certain unincorporated passive entities

- Certain grantor trusts, estates of natural persons and escrows

- Real estate mortgage investment conduits and certain qualified real estate investment trusts

- Nonprofit self-insurance trust created under Insurance Code Chapter 2212

- Trust qualified under Internal Revenue Code Section 401(a)

- Trust exempt under Internal Revenue Code Section 501(c)(9)

- Unincorporated political committees

Generally, all companies that are registered in Texas, or have nexus or meet economic nexus thresholds in the state must file a franchise tax return annually. To find out if your company is responsible for Texas Franchise Tax, fill out the accountability questionnaire.

You register for the franchise tax automatically when you register your company with the state (e.g., registering for a sales tax permit).

The amount of tax you owe depends on your entity’s margin. Use the Texas Franchise Tax calculator to find out how much you must pay. If your business’s annual revenue is less than $1,180,000 or you owe less than $1,000, you will not owe any tax. If your annual revenue is $20,000,000 or less, you can use the EZ computation (multiplying your total by a tax rate of 0.375%).

The Texas GRT is due on May 15 each year. If May 15 falls on a weekend or holiday, then your form and payment will be due on the following business day.

You can electronically file and pay your franchise tax online. Or, you can fill out a form and mail it to the state. The form you use depends on your situation (e.g., no tax due, using the EZ computation, etc.).

Washington

Washington’s gross receipts tax is the Washington Business and Occupation (B&O) Tax. You must register with the Washington Department of Revenue to pay B&O tax if:

- Your business is required to collect sales tax

- Your gross income is $12,000 per year or more

- Your business is required to pay taxes or fees to the Department of Revenue

- You are a buyer or processor of specialty wood products

You can register for the Washington B&O tax online using My DOR. After you register with the state, you will receive information about your tax filing frequency for the B&O tax. Here’s a breakdown of when the tax is due for each frequency:

- Monthly filers: 25th of the following month

- Quarterly filers: End of the month following the close of the quarter

- Annual filers: April 15

B&O tax rates vary depending on your classification. To find your classification, check out the Department of Revenue’s website. Once you know your business’s classification, you can find your rate using this list.

You can report and pay your B&O tax on your excise tax return or by electronically filing online through My DOR.

Looking for an easy way to track your business transactions? Patriot’s online accounting software lets you streamline the way you record your business’s income and expenses. Try it for free today!

This article has been updated from its original publication date of October 13, 2020.

This is not intended as legal advice; for more information, please click here.