In accounting, there’s one thing you can’t ignore: how debits and credits work. To keep accurate books, learn and understand the difference between credit vs. debit.

Debits and credits keep your books balanced and organized. Read on to learn more about debits and credits in accounting.

What are debits and credits in accounting?

Part of your role as a business is recording transactions in your small business accounting books. And when you record said transactions, credits and debits come into play.

Debits and credits are equal but opposite entries in your books. If a debit increases an account, you must decrease the opposite account with a credit.

Record accounting debits and credits for each business transaction. When you record debits and credits, make two or more entries for every transaction. This is considered double-entry bookkeeping.

So, what is the difference between debit and credit in accounting? Get the full scoop below.

Debit vs. credit: Debit

A debit (DR) is an entry made on the left side of an account. It either increases an asset or expense account or decreases equity, liability, or revenue accounts (you’ll learn more about these accounts later).

For example, you debit the purchase of a new computer by entering it on the left side of your asset account.

Debit vs. credit: Credit

On the other hand, a credit (CR) is an entry made on the right side of an account. It either increases equity, liability, or revenue accounts or decreases an asset or expense account (aka the opposite of a debit).

Using the same example from above, record the corresponding credit for the purchase of a new computer by crediting your expense account.

- Track your expenses, income, and money

- Get organized and prepared for tax time

- Enjoy free USA-based support

Credit and debit accounts

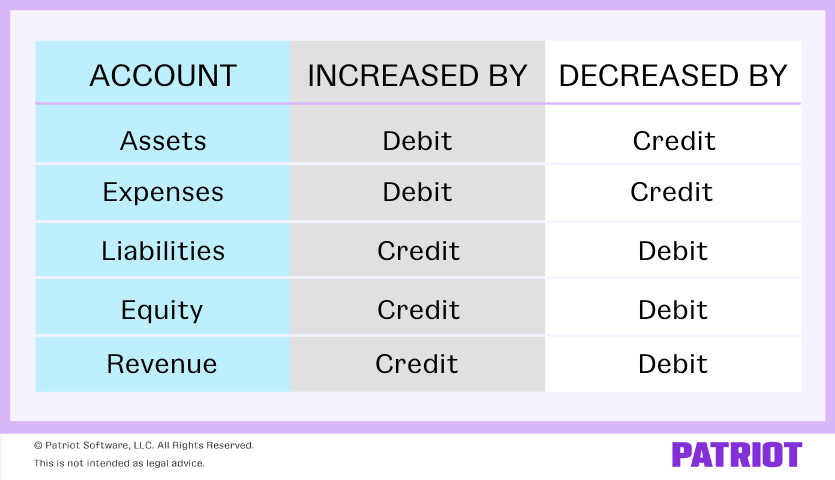

When recording transactions in your books, you use different accounts depending on the type of transaction. The main accounts in accounting include:

- Assets: Physical or non-physical types of property that add value to your business (e.g., land, equipment, and cash).

- Expenses: Costs that occur during business operations (e.g., wages and supplies).

- Liabilities: Amounts your business owes (e.g., accounts payable).

- Equity: Your assets minus your liabilities.

- Revenue/Income: Money your business earns.

Accounting credits and debits affect each account differently. Check out our chart below to see how each account is affected:

Debit and credit journal entry

So, what does a debit and credit journal entry look like? Here’s a basic example of how a debit and credit journal entry would look:

| Date | Account | Debit | Credit |

|---|---|---|---|

| X/XX/XXXX | Account | X | |

| Opposite Account | X |

Again, equal but opposite means if you increase one account, you need to decrease the other account and vice versa.

Debits and credits example 1

Let’s say you decide to purchase new equipment for your company for $15,000.

The equipment is an asset, so you must debit $15,000 to your Fixed Asset account to show an increase. Purchasing the equipment also means you increase your liabilities. To record the increase in your books, credit your Accounts Payable account $15,000.

Record the new equipment purchase of $15,000 in your accounts like this:

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| XX/XX/XXXX | Fixed Assets | Purchase of equipment | 15,000 | |

| Accounts Payable | 15,000 |

Debits and credits example 2

Say you purchase $1,000 in inventory from a vendor with cash. To record the transaction, debit your Inventory account and credit your Cash account.

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| XX/XX/XXXX | Inventory | Purchase inventory | 1,000 | |

| Cash | 1,000 |

Because they are both asset accounts, your Inventory account increases with the debit while your Cash account decreases with a credit.

Debits and credits example 3

Onto our last of the debits and credits examples: Sales on credit. You make a $500 sale to a customer who pays with credit. Increase your Revenue account through a credit. And, increase your Accounts Receivable account with a debit.

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| XX/XX/XXXX | Accounts Receivable | Sale to customer on credit | 500 | |

| Revenue | 500 |

Credits vs. debits: Quick recap

Have a firm grasp of how debits and credits work to keep your books error-free. Accurate bookkeeping can give you a better understanding of your business’s financial health. Not to mention, you use debits and credits to prepare critical financial statements and other documents that you may need to share with your bank, accountant, the IRS, or an auditor.

Check out a quick recap of the key points regarding debits vs. credits in accounting.

Debits

- Debits increase as credits decrease.

- Record on the left side of an account.

- Debits increase asset and expense accounts.

- Debits decrease liability, equity, and revenue accounts.

Credits

- Credits increase as debits decrease.

- Record on the right side of an account.

- Credits increase liability, equity, and revenue accounts.

- Credits decrease asset and expense accounts.

This article was updated from its original publication date of December 3, 2015.

This is not intended as legal advice; for more information, please click here.