Worried that your company is going under? If you’re struggling with large amounts of business debts, it might be time to consider your small business bankruptcy options.

Bankruptcy is overwhelming enough without the confusion that comes with understanding legal lingo. Read on for a clear overview of what is business bankruptcy and the types of bankruptcies out there.

What is small business bankruptcy?

Bankruptcy is a legal process available if you are unable to repay your debts. Through business bankruptcy, eligible companies’ debts are eliminated or put on a repayment plan. Creditors receive a portion of debt repayment through the debtor’s (aka the person filing bankruptcy for a small business) available assets.

Both individuals and businesses can file for bankruptcy. In 2020, there were 22,482 business bankruptcies and 659,881 non-business bankruptcies for a total of 682,363.

Bankruptcy has the potential to wipe out all the debts you list when filing. But, not all debts are eligible to be forgiven through bankruptcy. Debts you may still owe after successfully filing for bankruptcy include tax claims.

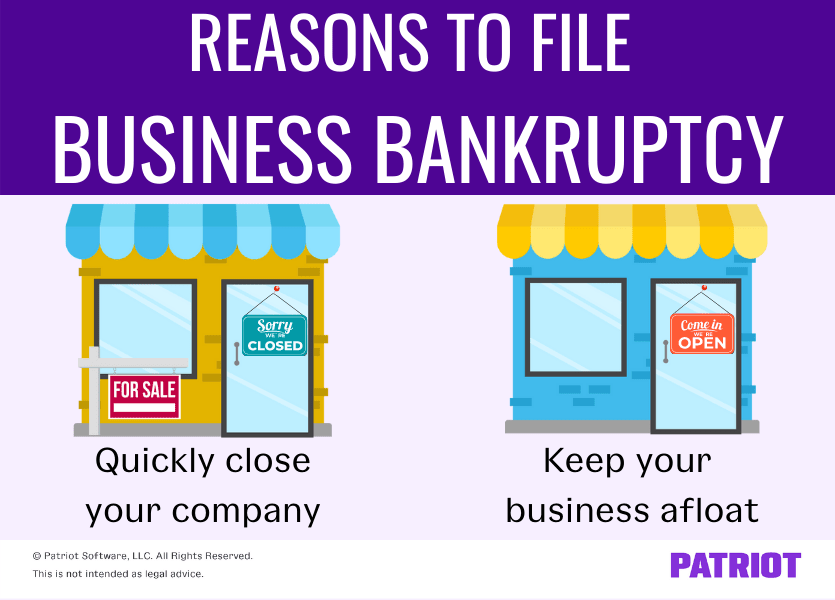

Reasons to file business bankruptcy

If your business is failing, bankruptcy might be your best option. You might file for bankruptcy to:

- Quickly close your company: You don’t have to deal with wrapping up every aspect of your business, such as selling inventory, getting rid of equipment, and collecting unpaid invoices

- Keep your business afloat: If you want to continue operating, filing bankruptcy can keep you in business while lessening your debt

So, what causes bankruptcy in business? You may be left with small business bankruptcy as a result of:

- Poor market conditions

- Lack of financing

- Hasty decision-making

- Cash flow issues

- Lawsuits

How does the bankruptcy filing process work?

Federal courts handle bankruptcies. To get the ball rolling with bankruptcy, you must file a petition with your local federal bankruptcy court. The petition asks for information like your name and address, debt amounts, number of creditors, and asset value.

Once you send the petition, you receive an automatic stay. That means your creditors must stop trying to collect money from you.

You must also file bankruptcy schedules when starting the bankruptcy process. The schedules list your assets and liabilities, income and expenses, and contracts and leases.

The type of bankruptcy you file and your business structure affect what happens after filing. In some cases, your business debts are dismissed. But depending on the type of bankruptcy and structure you operate under, your personal assets could be at risk.

Types of bankruptcies for business

There are three main bankruptcy filing options available for businesses: Chapter 7, Chapter 11, and Chapter 13. Chapter 7 uses liquidation while Chapters 11 and 13 use reorganization.

So, what is liquidation? What is reorganization?

- Liquidation: During liquidation, the business closes and its assets are divided among creditors.

- Reorganization: Reorganization involves the restatement of assets and liabilities to extend the life of the company. New arrangements are made to pay creditors, and the business continues to operate.

The type of bankruptcy you choose depends on whether you want to liquidate or reorganize your business and what entity you have.

Chapter 7 for business owners

Chapter 7 bankruptcy uses liquidation to handle a failing business. If you file Chapter 7, you must close the business and give up your assets. The assets you forfeit depend on your business structure.

Individuals and businesses can file Chapter 7, including the following types of business structures:

- Sole proprietorships

- Partnerships

- Corporations

- Limited liability companies (LLCs)

Although all business entities can file, sole proprietors receive a different outcome than other structures.

If you’re a sole proprietor declaring bankruptcy, consider filing under Chapter 7. This type of bankruptcy is cheaper and easier than others for sole proprietorships.

Chapter 7 for sole proprietors

With Chapter 7, unsecured debts get wiped out. You do not need to pay your qualifying debts. This can wipe out debts such as credit card debts, loans, back rent, utility bills, and lawsuit judgments.

Chapter 7 relieves you of most business and personal debts, but there is a downside. Because a sole proprietorship is not a separate legal entity, you are personally responsible for all business assets. As a result, your personal assets are at risk.

While some assets are exempt, items such as your equipment, vehicles, and mortgage could be seized and sold to pay debts.

Chapter 7 for partnerships, corporations, and LLCs

Although you can file Chapter 7 bankruptcy for your business if it’s not structured as a sole proprietorship, it works a little differently.

And for many non-sole proprietorship businesses, this difference is a turnoff.

Unlike sole proprietorships, partnerships, LLCs, and corporations cannot wipe out business debts with Chapter 7. However, it transfers the burden of selling off assets and paying creditors to the bankruptcy trustee, not the owners.

Small business Chapter 11

Chapter 11 bankruptcy uses reorganization to manage failing businesses. With Chapter 11, you continue to run your business under the bankruptcy terms.

Individuals and businesses can file Chapter 11, including the following types of business structures:

- Sole proprietorships

- Partnerships

- Corporations

- Limited liability companies (LLCs)

The process reorganizes your debts so you can make smaller payments to creditors. However, you need to have enough incoming cash each month to make the new payments.

Chapter 13 bankruptcy for business

Chapter 13 is a reorganizing option only available for individuals, including sole proprietors. If your business is structured as a partnership, corporation, or LLC, you cannot file bankruptcy under Chapter 13.

Chapter 13 works similarly to Chapter 11. You continue to run your business while paying creditors. And, you do not have to give up your business assets.

However, filing under Chapter 13 only wipes out your personal liability for business debts, not the business debt itself.

How to choose the best business bankruptcy option

Small business bankruptcies should be one of the last options for a failing business. Before filing bankruptcy, you may consider other options, like improving cash flow management, obtaining new financing, or selling your company.

If your business is going under, bankruptcy could protect you from losing everything you’ve worked for. But, which is the right type of bankruptcy to file?

Take a look at our chart comparing the three major business bankruptcy options:

| Chapter 7 | Chapter 11 | Chapter 13 | |

|---|---|---|---|

| Purpose | To liquidate the business | To reorganize and stay in business | To reorganize and stay in business |

| Business Structures | Sole proprietorship, partnership, LLC, corporation | Sole proprietorship, partnership, LLC, corporation | Sole proprietorship |

| Number of Cases (2020) | 436,919 | 7,568 | 237,099 |

Speak with a small business lawyer who specializes in business bankruptcy before filing.

Need a better way to keep your books organized and manage business finances? Patriot’s accounting software makes it easy to record transactions with a few easy clicks, generate reports, and more. Plus, we offer free USA-based support. Get your free trial today!

This article has been updated from its original publication date of December 15, 2016.

This is not intended as legal advice; for more information, please click here.