When it comes to health coverage, there are a lot of options out there. FSAs and HSAs are healthcare plans that cover medically-related expenses not included under a traditional health plan. Do you know the difference between an FSA vs. HSA?

Both employers and employees should understand the difference between HSA and FSA. Read on to learn more about the plans. Plus, take a look at our handy HSA versus FSA chart.

- HSAs require an HDHP, are employee-owned, funds roll over, and contribution limits are higher than FSAs.

- FSAs are employer-established, employer-owned, give full-year access upfront, and unused funds may be forfeited or limited carryover.

- Both accounts use pre-tax dollars for qualifying medical expenses, lowering taxable income for employees and employers.

What are FSA and HSA plans?

Flexible spending accounts (FSAs) and health savings accounts (HSAs) work like personal savings accounts. However, the funds in the account can only go toward qualifying medical expenses. An employee who has an FSA or HSA contributes pre-tax dollars to their account, lowering their taxable income. Employees can use their account funds to cover out-of-pocket medical expenses.

The two plans work similarly. Employees, employers, or both can contribute to the employee’s account.

As an employer, you aren’t required to offer HSAs or FSAs. And, you aren’t required to contribute to an employee’s FSA or HSA plan if you do offer them. You can choose to contribute to your employees’ plans if you want.

If employees decide to contribute to an account, they determine the amount they want to contribute. Employers withhold the specified funds from an employee’s gross wages each pay period.

What is the difference between FSA vs. HSA?

Though there are similarities between the two plans, there are a number of differences between an HSA vs. FSA.

Here are some common questions about health savings account vs. flexible spending account plans:

- Who’s eligible to contribute?

- How much can an employee contribute?

- Who owns the account?

- When can an employee access their account funds?

- Can employees roll over funds in their accounts from year-to-year?

- Can an employee change contribution amounts throughout the year?

- How does the employee use funds?

HSA plans

A health savings account is a tax-free fund that qualifying individuals can use to pay for out-of-pocket health care costs.

Employees and self-employed individuals alike can open a health savings account … if they meet the requirements. An employee can only have an HSA if they have a high deductible health plan (HDHP).

A high deductible health plan is a type of health insurance with high annual deductibles and low monthly premiums. To have an HSA in 2026, the employee’s deductible must be at least $1,700 for self-only coverage and twice that amount ($3,400) for family coverage. And, the employee’s annual out-of-pocket expenses cannot be more than $8,500 (self) or $17,000 (family) for in-network services.

If you have employees who qualify, tell them about contribution limits. For 2026, an individual can contribute a maximum of $4,400 to their HSA if they have self-only coverage and $8,750 if they have family coverage. Individuals who are 55 years old or older can contribute an additional $1,000.

Employees, not employers, own HSAs. If an employee leaves your business, they can take their account with them. Account holders can also roll over HSA funds from year to year. The rolled-over funds do not count toward the individual’s maximum contribution limit.

Again, employees, employers, or both fund HSAs through contributions they make per pay period. If an employee has an HSA, withhold their contribution amount from their wages and remit it into their HSA. These funds are available as they’re deposited into the employee’s account.

An employee can change their HSA contribution amounts at any time throughout the year.

There are two options for how an employee can use their HSA funds after they incur a qualifying expense. Employees may receive a designated HSA debit card they can use to cover the bill. Or, they might receive reimbursements after paying for an eligible expense.

FSA plans

A flexible spending account is a tax-free fund that employees can use to pay for out-of-pocket health care costs.

Unlike an HSA, only employees can open FSAs. Self-employed individuals cannot have a flexible spending account.

An employee can open an FSA regardless of the type of health insurance plan they have. That means that employees with low-deductible health insurance plans can have FSAs.

For 2026 employees can contribute up to $3,400 to their FSA. However, employees do not own their accounts. Their employers do. If an employee leaves during the year, they forfeit their remaining FSA funds to you.

Employees elect how much they want to contribute to their FSA during open enrollment for employees. They receive their full amount at the start of the year, even though they haven’t contributed that much. That means that employees who leave mid-year and use more from their account than what they contributed must pay back the difference.

- Give employees a “grace period” of 2.5 months to use their funds

- Let employees carry over $680 of unused funds to the next year (2026 carryover amount)

To receive a reimbursement, employees must submit a claim to their employer, along with a written statement saying their plan hasn’t covered the expense.

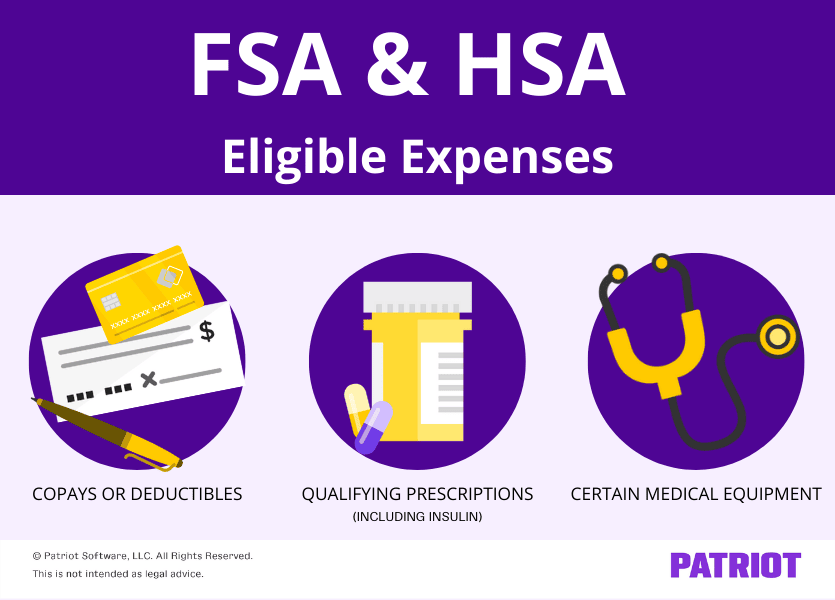

FSA vs. HSA eligible expenses

So, what can your employees use FSA and HSA funds for? Account-holders, their spouses, and dependents use the funds in the holder’s plan to pay for qualifying medical expenses.

Regardless of if the employees have a FSA vs. HSA, the following are IRS eligible expenses:

- Copays or deductibles

- Qualifying prescriptions (including insulin)

- Certain medical equipment

For a full list of medical expenses account holders can use their FSA or HSA funds on, view the IRS’s Publication 502, Medical and Dental Expenses.

HSA vs. FSA chart

Depending on your business and the health insurance plan(s) you offer, you might only be able to offer an FSA. But if you are eligible to offer either FSA and HSA plans, compare the two to see which is right for your business.

Use our chart to get quick answers to all of your questions relating to FSA and HSA plans. Ready to find out which is the best option for your small business and employees?

Eligibility to Contribute

FSA

Employers must establish an FSA plan for employees to contribute. Employees can open an FSA regardless of if they have an HDHP or not.

Self-employed individuals cannot open an account.

HSA

Employees are eligible if they have an HDHP. The deductible must be at least $1,700 (self) or $3,400 (family). And, the annual out-of-pocket expenses can’t exceed $8,500 (self) or $17,000 (family).

Self-employed individuals can open an account.

Annual Employee Contribution Limits

FSA

For 2026, employees can contribute up to $3,400 per year.

HSA

For 2026, employees can contribute up to $4,400 if they have self-only coverage and $8,750 if they have family coverage. If the employee is 55 years or older, they can contribute an additional $1,000.

Eligible Expenses

FSA

Copays or deductibles

Qualifying prescriptions (including insulin)

Certain medical equipment

HSA

Copays or deductibles

Qualifying prescriptions (including insulin)

Certain medical equipment

Account Ownership

FSA

An FSA is owned by the employer. Unused funds belong to employers, not the employees.

HSA

An HSA is owned by the employee. They can take their accounts with them if they quit.

Access to Money

FSA

At the beginning of the plan year. An employee has complete access to their annual election at any time, regardless of if they have contributed that amount yet or not.

HSA

As the employee contributes to their plan. An employee only has access to what has actually been deposited into their HSA account.

Rollover Rules

FSA

Employers choose whether an employee can keep their unused funds or not. There are three options:

FSA Forfeiture: Employee forfeits money, and employers get to keep it.

Grace period: Employee has a 2.5-month grace period after the plan year ends to use on expenses. The remaining money after the grace period is the employer’s.

Carryover: Employees can add up to $680 (2026 amount) of unused funds to next year’s plan (in addition to contribution limit). Employers decide the carryover limit, and any funds over the limit are the employer’s.

HSA

Funds do not expire from year-to-year. Rollover money is in addition to the contribution limits.

Receiving Funds

FSA

To receive a reimbursement, the employee needs to submit a claim and a written statement that says the expense isn’t covered by a different plan. Account-holders do not need to report FSA contributions on their tax forms.

HSA

Individuals either receive an HSA debit card or reimbursements to pay for eligible expenses. The account holder must report these distributions on Form 8889, Health Savings Accounts.

Option to Change Contributions

FSA

Your employee must determine their contribution amount at the beginning of the year. If the employee has a family status change (i.e., marriage, divorce, etc.), they can change their contribution amount during the year.

HSA

The account holder can change their contribution amount, as long as it does not exceed the contribution limit.

Advantages of FSAs and HSAs

Regardless of whether you offer an FSA or HSA plan, employees benefit. Tax reduction and employee satisfaction are just two of the reasons you might choose to offer an FSA, HSA, or both.

By reducing an employee’s taxable income, you also decrease your tax liability. As the employer, you need to make a matching contribution for FICA tax. The lower an employee’s FICA tax liability, the less you have to pay.

When you offer an FSA or HSA plan, you can keep employees satisfied, reduce their tax liability, and reduce your employer taxes.

Thinking about offering an FSA or HSA plan to employees? Don’t get overwhelmed by your employer responsibilities. Patriot’s online payroll lets you track your employees’ FSA and HSA deductions easily and accurately. Try it for free today!

This article has been updated from its original publication date of March 3, 2015.

This is not intended as legal advice; for more information, please click here.