There are a number of paid sick leave laws by state. To stay compliant, some employers have turned to third parties to handle sick pay. Do your employees receive third-party sick pay?

If you offer employees sick pay through a third party, you may have some questions. Is the pay taxable? What are your reporting obligations? Read on to find out. And if you’re unfamiliar with third-party sick pay, you can learn about that as well.

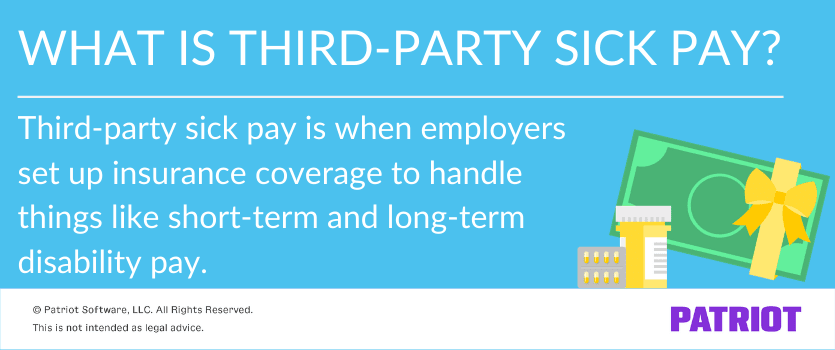

What is third-party sick pay?

Sick pay is when an employee receives their regular wages even though they are not working due to an illness, injury, or disability. Generally, employers who offer sick pay fund it themselves. But, some employers turn to third parties (e.g., insurance companies) to handle their sick pay for extended periods of times, like short-term or long-term disability.

Sometimes, the third party acts as the “employer’s agent,” or third-party administrator. Other times, the third party paying out sick wages is not the employer’s agent. This distinction is important for taxes, which we’ll get into later.

Unlike sick pay employees receive for missing a day here or there, short-term disability and long-term disability are types of insurance benefits. As a result, employees typically receive a percentage of what they would have earned if they were working.

Like other types of insurance, employers set up coverage with a third party before an employee needs it. The third party then doles out a percentage of the employee’s wages if the employee qualifies for sick pay.

What doesn’t count as sick pay?

Sick pay may include short- and long-term benefits, but it doesn’t include everything. According to the IRS, sick pay does not include:

- Disability retirement payments

- Workers’ compensation

- Medical expense payments

- Payments unrelated to absence from work (e.g., accident or health insurance payments)

Third party sick pay: Taxable or not?

When employers directly provide employees with sick pay, the wages are included in the employee’s total gross wages and taxed. But, sick pay through a third party works a bit differently.

So, is third-party sick pay taxable? Here’s the scoop:

- 100% taxable: If you pay 100% of your employee’s sick pay insurance, the entire amount is taxable. This is also true if your employee pays for it with pre-tax dollars.

- Partially taxable: If you only pay a portion of the insurance premium, the employee pays taxes on just that amount. For example, if you and your employee each contribute 50% of the premium, 50% of the sick pay is taxable.

- Nontaxable: If an employee pays for all of their insurance premium using only after-tax income, the sick payments are not taxed.

If sick pay is taxable, it is subject to Social Security, Medicare, FUTA (federal unemployment), and income taxes.

Who handles the taxes?

OK, OK … so who handles the taxes when you use a third party to distribute sick wages? Do you, or does the third party?

To answer that, we have to go back to the distinction between whether the third party is your “agent” or not.

Third party: employer’s agent

Employer agents are reimbursed on a cost-plus-fee basis. An agent does not have a direct insurance risk. Instead, they simply provide an administrative service.

If you have a third party acting as your agent, you are responsible for handling employment taxes. The third party does not take on the role of employer.

Calculate Social Security, Medicare, and FUTA taxes like normal. You (not the third party) pay the employer portion of the taxes. In this situation, the IRS treats sick pay as supplemental wages when it comes to federal income tax. You can either withhold a flat 22% on the wages for federal income tax or use the employee’s Form W-4 to determine withholding.

However, you can opt to enter an agreement with the third party to have them handle employment taxes.

Third party: not employer’s agent

If a third party handles sick pay and they are not your agent, they are responsible for handling employment taxes. They must use their own EIN (Employer Identification Number) and name for tax reporting purposes.

The non-agent does not have to withhold federal income tax on sick pay. But, an employee can choose to have the third party withhold the tax by filling out Form W-4S, Request for Federal Income Tax Withholding From Sick Pay, and submitting it to the third party.

The third party does have to calculate Social Security, Medicare, and FUTA taxes. They, not you, are responsible for paying the employer portion of these taxes.

However, the third party not acting as your agent can opt to transfer this employer liability back to you, the employer.

For more information on third-party sick pay and taxation, consult IRS Publication 15-A.

How to report IRS third-party sick pay

Reporting third-party sick pay can get a little tricky. You, the third party, or both you and the third party use a number of forms to report sick payments:

- Form 940: You prepare Form 940.

- Form 941 or 944: Both you and the third party file Form 941 or Form 944.

- Form 8922: Either you or the third party files Form 8922, Third Party Sick Pay Recap.

- You must file if you report sick pay on Forms W-2 using the name and EIN of the third party.

- Third party must file if they report sick pay on Forms W-2 under your name and EIN.

- Form W-2: Either you or the third party is responsible for third-party sick pay W-2 reporting, if applicable.

Check out IRS Publication 15-A for more information on reporting third-party sick pay.

Setting up third-party sick pay

If you’re interested in starting third-party sick pay, establish a plan. Your plan should be in writing and detail your contributions and who qualifies for sick pay.

When contracting with a third party to handle sick pay, provide the following information:

- Employee’s name and other identifying information (e.g., SSN)

- Employee’s total wages that will be paid during the calendar year

- Date(s) the employee last did work for the employer (generally only the last month)

- Amount of after-tax money the employee contributed to their sick pay plan, if any

Once your plan is established, make contributions to the third party in charge of the sick pay plan. Again, the contributions include the sick pay costs as well as a third-party fee if you use an agent.

Are you in charge of handling tax withholding on sick pay? Sign up for Patriot’s Full Service payroll and kick your responsibilities to the curb. We’ll file and deposit federal, state, and local taxes so you can worry about what you care most about: your business. Get your free trial today!

This article has been updated from its original publication date of March 19, 2015.