Most businesses offer employee benefits in addition to regular wages. Common employee benefits can range from different insurance options to types of retirement plans. Some employees have the option of opening an HSA. What is an HSA?

- An HSA lets individuals save pre-tax dollars for qualifying medical expenses when enrolled in a high-deductible health plan.

- 2026 HDHP minimum deductibles: $1,700 self-only, $3,400 family; out-of-pocket limits: $8,500 self-only, $17,000 family.

- 2026 HSA contribution limits: $4,400 self-only, $8,750 family; plus $1,000 catch-up for ages 55 and older.

- HSA funds are tax-advantaged: pre-tax contributions, tax-free distributions for qualified expenses, and tax deductions on tax returns.

- HSA funds roll over year to year; excess contributions incur income inclusion and usually a 6% excise tax.

What is an HSA?

An HSA, or health savings account, is a plan where individuals put aside pre-tax dollars to use on qualifying medical expenses, like copays, prescribed medicine, and medical equipment. Individuals must be enrolled in a high-deductible health plan to open an HSA and are only allowed to contribute up to a certain amount.

How does a health savings account work?

An employee sets up their HSA with a qualified trustee, like a bank. You can recommend trustees to your employees to help them set up their HSA. And, you can withhold the money from the employee’s gross wages to put into their HSA.

You can contribute to an employee’s HSA account if you so choose. But, you are not required to make contributions. Employer contributions are not included in the employee’s income. Your contributions cannot discriminate in favor of highly-compensated employees; they must be comparable for all employees.

If you are self-employed, you can open your own HSA, as well.

Don’t confuse an HSA with an FSA (flexible spending account) or an Archer MSA (medical savings account). All three are accounts used for health and medical expenses, but they differ in things like contribution limits and carryover policies.

To learn more about HSAs, continue reading.

HSA eligibility

According to HSA rules, employees can only open HSAs if they have a high deductible health plan (HDHP). An HDHP is health insurance that has low monthly premiums and high deductibles. That means the employee only pays a little bit out of their paycheck but pay more for their deductible.

To meet the requirements of an HDHP, the plan must have a deductible of at least $1,700 (self-only coverage) or $3,400 (family coverage) in 2026. The annual out-of-pocket expenses cannot be above $8,500 (self-only coverage) or $17,000 (family coverage) in 2026.

| Category | 2026 Requirements |

|---|---|

| Deductible (Self-only Coverage) | $1,700 (minimum) |

| Deductible (Family Coverage) | $3,400 (minimum) |

| Annual Out-of-pocket Expenses (Self-only Coverage) | $8,500 (maximum) |

| Annual Out-of-pocket Expenses (Family Coverage) | $17,000 (maximum) |

The employee cannot have any other health insurance. However, individuals can have insurance that targets specifics, like for a specific disease or illness or a fixed amount per period of hospitalization. Employees are also allowed to have accident, disability, dental care, vision care, and long-term care coverages.

Under the health savings account rules, an individual cannot open an HSA if they can be claimed as a dependent. Generally, an employee cannot contribute to both an FSA and HRA while contributing to their HSA. However, there might be some exceptions. Consult the IRS’s Publication 969 for more information on multiple health accounts.

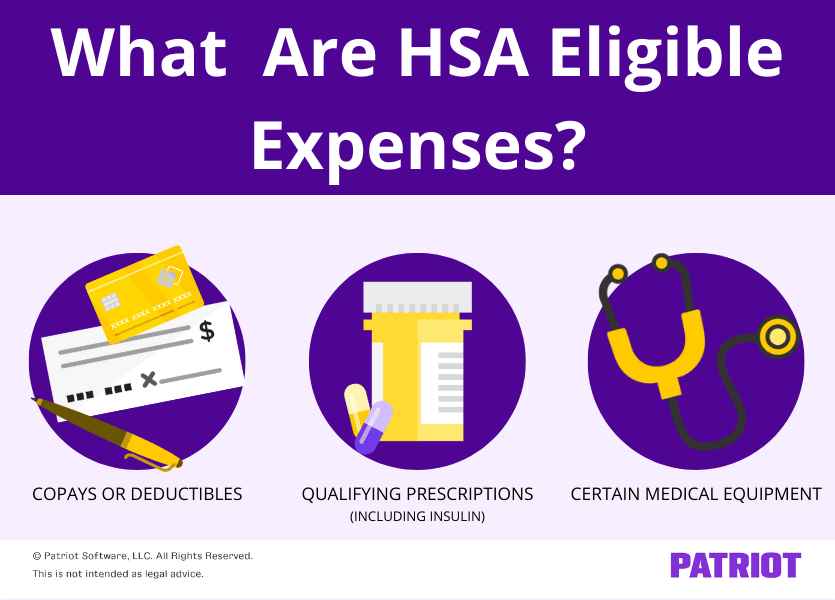

What can account holders use HSA funds on?

When account holders, their spouses, and dependents spend money on qualifying medical expenses, they will be reimbursed with their HSA funds. Individuals can use funds for the following:

- Copays or deductibles

- Prescribed medicine (including insulin)

- Certain medical equipment

Specific things you can use HSA funds on include contact lenses, crutches, chiropractic care, hospital services, and dental treatment. For a full list, view the IRS’s Publication 502, Medical and Dental Expenses.

2026 HSA contribution limit

According to the 2026 HSA contribution rules, an employee can contribute up to $4,400 if they have self-only coverage under their HDHP. Or, they can contribute up to $8,750 if they have family coverage under an HDHP.

If the employee is 55 years old or older, they can contribute $1,000 more to their HSA.

Any amount that exceeds the contribution limit must be included in the individual’s gross income; if it is not, it must be reported as “other income” on the individual’s tax return. There is generally a 6% excise tax on any money over the contribution limit.

Are HSA plans taxable?

The funds are taken out of the employee’s wages before the income is taxed, making an HSA plan a pre-tax benefit. This reduces the employee’s tax liability and is one of the notable benefits of an HSA.

And, the individual who opens the account can receive a tax deduction when filing their taxes.

Requirements for receiving distributions

When an HSA account holder receives distributions from their plan, HSA plan rules require that the individual keep records indicating the medical expense hasn’t been paid with another policy.

The individual must report their distribution on Form 8889, Health Savings Accounts. If the distribution is not for a qualified medical expense, the individual generally pays a 20% tax.

HSA rollover rules – can employees carry money over?

Unlike other health accounts, the funds in an HSA do not expire. Individuals can carry money over from their HSA.

Employees can also carry money over from an Archer MSA to an HSA. Rollover money can be in addition to the contribution limits.

Need an easier way to manage your payroll? Patriot’s online payroll software offers a simple way to withhold taxes, benefits, and other deductions from employee wages. Enjoy a free trial today!

This article has been updated from its original publish date of October 5, 2011.

This is not intended as legal advice; for more information, please click here.