You must withhold the right amount of taxes on employee wages when paying employees. But what if you need to pay an independent contractor? To keep tax information straight between independent contractors and employees, you need to know the difference between Form W-9 vs. W-4. Read on for the scoop.

What is the difference between W-9 vs. W-4?

New employees mean new IRS forms to complete. And because the IRS treats taxes differently between employees and independent contractors, there are two separate forms you need to know about.

To put things simply:

- Employees must complete Form W-4

- Independent contractors must use Form W-9

But like with all things tax-related, understanding W-9 vs. W-4 can be tricky. Let’s break down the difference between W-4 and W-9.

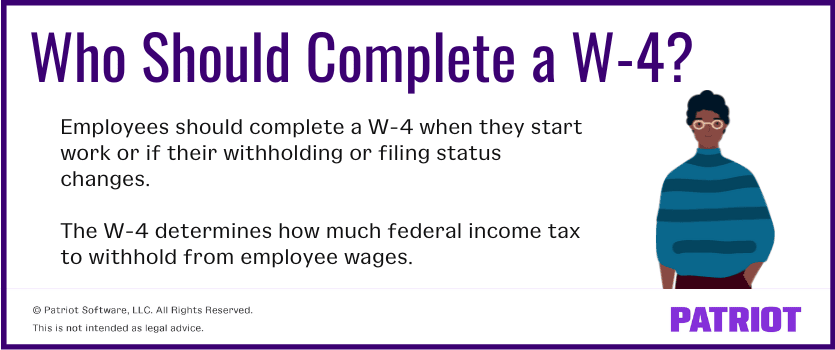

Form W-4

You must use IRS Form W-4, Employee’s Withholding Certificate, to determine how much federal income tax to withhold from employee wages. Employees must complete Form W-4 when they start a new job or if their withholding or filing status changes.

In 2020, the IRS released a new Form W-4 to reflect changes of the Tax Cuts and Jobs Act, which simplified the filing process and improved tax withholding accuracy. The new Form W-4 is only for employees hired after 2019.

New W-4

What’s the difference between the old W-4 and the new W-4? The main difference is how employees manage their tax withholding. Here’s a little breakdown:

- Forms from 2019 or earlier: Offer withholding allowances

- W-4 forms from 2020 or later: Let employees increase or decrease their taxes withheld and their wages subject to withholding

If you’ve hired new employees after 2019, make sure they use a Form W-4 from 2020 or later. Employees hired before 2019 don’t have to use the new W-4 form unless they want to update their withholdings or switch to the newer W-4 form.

What’s on the form?

Employees must fill out the following information on Form W-4:

- Name

- Address

- Social Security number

- Filing status (e.g., single, married filing jointly, etc.)

- Additional jobs or spouse work information

- Number of dependents

- Adjustments (e.g., deductions, withholdings, and non-job related income)

Remember that some states require that employees also complete a state-specific W-4 form to help withhold state income tax.

See IRS Publication 15-T for more information.

Using the computational bridge

If juggling the old W-4 and the new W-4 sounds confusing, consider using the computational bridge. The IRS created the computational bridge so business owners can choose to use one income tax withholding table instead of two. How does it work? The computational bridge is a four-step process that lets employers convert early W-4 forms to W-4s from 2020 and later.

The computational bridge is optional and only applies to W-4s from 2019 or before.

Let’s look at an example of this in action. An employer decides to expand and hire new employees. Half of the employees use a W-4 from 2019 or before, and the other half use a W-4 from 2020 or later. The employer realizes that using different income tax withholding tables is a hassle, so they decide to use the computational bridge to convert early W-4 forms to the revised W-4. Once they convert all the forms to the newer W-4, the employer only needs to use one withholding table.

Remember to use the computational bridge only for W-4 forms from 2019 or earlier. You must stop using the computational bridge whenever an employee switches to the newer W-4 from 2020 or later.

For more information on the computational bridge, see IRS Publication 15-T.

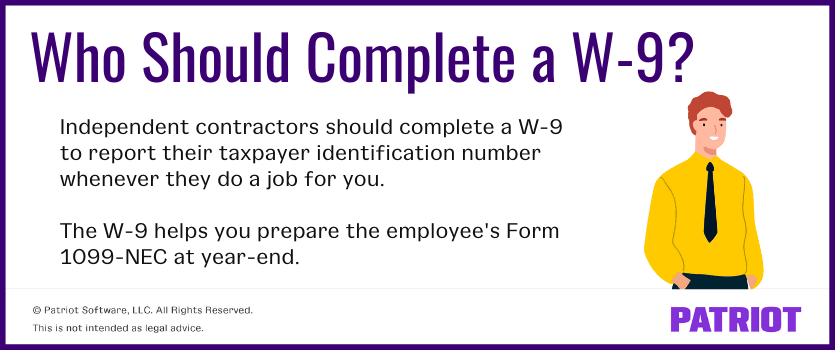

Form W-9

Independent contractors must complete Form W-9, Request for Taxpayer Identification Number and Certification. Then, you use the form to prepare a contractor’s Form 1099-NEC at year-end. Form W-9 lets independent contractors report their taxpayer identification number (TIN) when they do a job for you.

Remember that the W-9 isn’t only for contractors. You may need a W-9 to report other types of income, like:

- Acquisition or abandonment of secured property

- Cancellation of debt

- Contributions made to an IRA

- Real estate transactions

If you’re unsure if a worker needs to fill out Form W-9, check out the IRS’s Form W-9 Instructions.

What’s on the form?

Independent contractors must include the following information on their Form W-9:

- Name

- Business or entity name

- Tax classification

- Exemptions

- Address

- TIN

- Signature

Independent contractors must enter their Social Security number for the TIN if they file as individuals. If they file as a resident alien, sole proprietor, or disregarded entity, they must follow the instructions for Part I. Otherwise, independent contractors should use their Employer Identification Number (EIN).

Keep a Form W-9 on file for each independent contractor you hire and pay $600 or more in nonemployee compensation during the tax year.

If independent contractors fill out the W-9 incorrectly, you may have to withhold and remit backup withholding.

Backup withholding

If an independent contractor makes a mistake on their W-9, you may need to withhold and remit backup withholding. Backup withholding requires you to withhold a 24% tax on the wages of an independent contractor. Remit backup withholding if the:

- Independent contractor didn’t give you a TIN

- Contractor didn’t certify their TIN

- IRS tells you the TIN is incorrect

- IRS tells the contractor their payments are subject to backup withholding because they didn’t report interest or dividends on their tax return

- Independent contractor didn’t certify they aren’t subject to backup withholding

Use Form 945, Annual Return of Withheld Federal Income Tax, if an independent contractor’s payments are subject to backup withholding.

For more information on exemptions from backup withholding see “Exempt payee code” in the Form W-9 instructions.

Patriot software knows you may need to hire employees and independent contractors to get things done. That’s why Patriot’s online payroll software makes paying employees and independent contractors a breeze. You can even pay your contractors with direct deposit. Try it for free today!

This is not intended as legal advice; for more information, please click here.