You know that paying someone comes at a cost. In addition to giving employees their paychecks, you also have the cost of payroll taxes. So, how much does an employer pay in payroll taxes? Keep reading to learn more about the employer cost of payroll taxes.

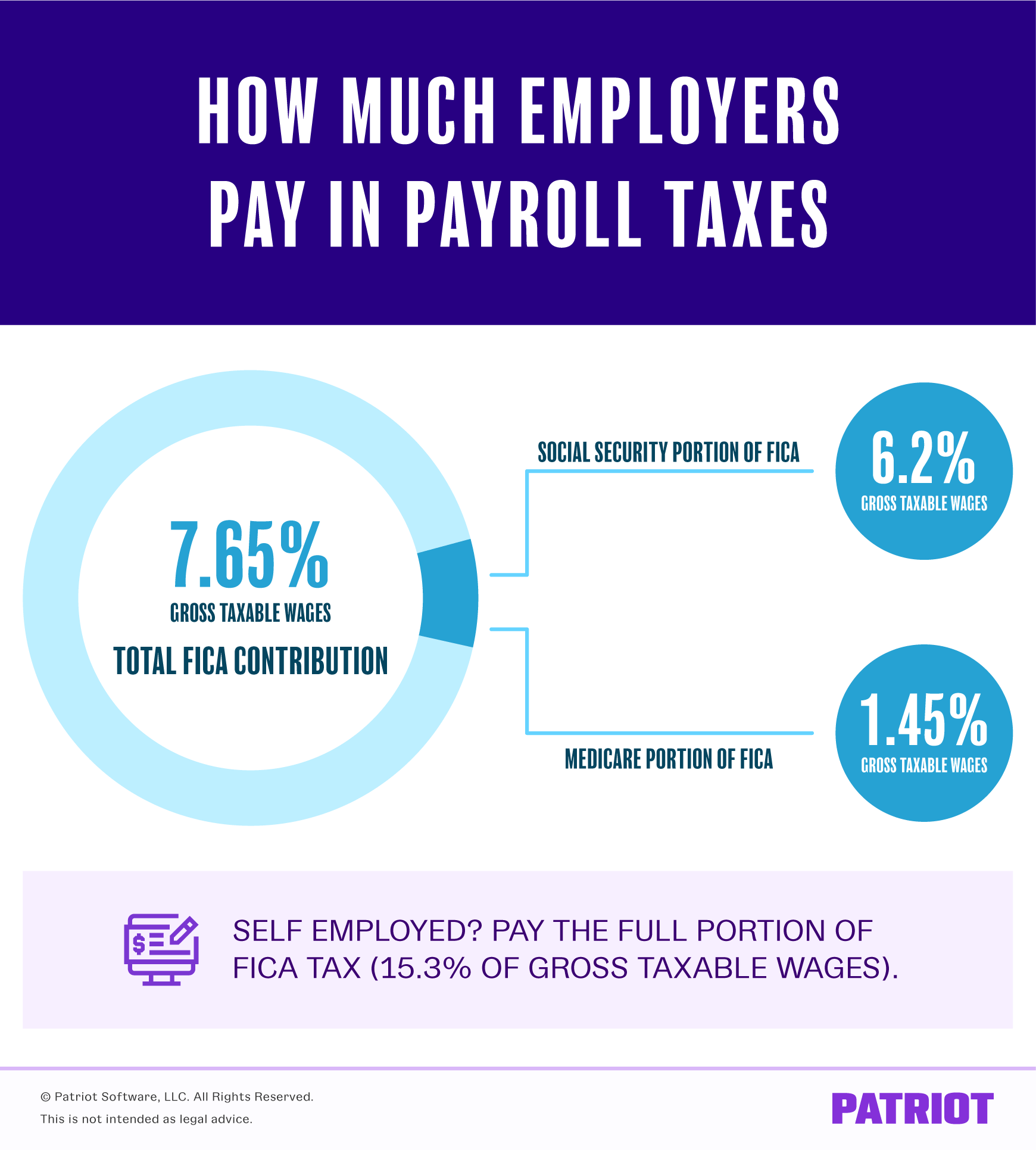

- Employer payroll taxes equal half of FICA: 6.2% Social Security and 1.45% Medicare, totaling 7.65% of gross taxable wages.

- Social Security has a wage base ($184,500 in 2026); contributions stop after that limit per employee.

- Employers do not pay the additional 0.9% Medicare tax for wages over $200,000; employees pay the extra amount.

- Employers also pay unemployment taxes: FUTA (generally 0.6% up to $7,000) and state SUTA rates and wage bases vary by state.

How much do employers pay in payroll taxes?

So, how much does an employer pay in payroll taxes? The cost of payroll taxes largely depends on the number of employees you have and how much you pay your employees. Why? Because payroll taxes are a percentage of each employee’s gross taxable wages and not a set dollar amount.

Payroll tax includes two specific taxes: Social Security and Medicare taxes. Both taxes fall under the Federal Insurance Contributions Act (FICA), and employers and employees pay these taxes.

Payroll tax percentage is 15.3% of an employee’s gross taxable wages. In total, Social Security is 12.4%, and Medicare is 2.9%, but the taxes are split evenly between both employee and employer.

So, how much is the employer cost of payroll taxes? Employer payroll tax rates are 6.2% for Social Security and 1.45% for Medicare.

If you are self-employed, you must pay the entirety of the 15.3% FICA tax, plus the additional Medicare tax, if applicable (and we’ll get to that in a minute).

Social Security

Social Security taxes have a wage base. In 2026, this wage base is $184,500. The wage base means that you stop withholding and contributing Social Security taxes when an employee earns more than $184,500.

Take a look at an example. Let’s say you have an employee who earns $2,000 biweekly:

$2,000 X 6.2% = $124

The employer cost of payroll tax is $124.

Keep in mind that some pre-tax deductions (e.g., Section 125 plans) can lower the gross taxable wages and impact how much you contribute per employee paycheck.

For example, an employee with gross wages of $1,500 biweekly and a $500 Section 125 deduction has $1,000 in gross taxable wages ($1,500 – $500). So, you calculate Social Security on $1,000 instead of $1,500:

$1,000 X 6.2% = $62

The employer cost of the Social Security tax is $62.

Medicare

Unlike Social Security, Medicare taxes do not have a wage base. Instead, Medicare has an additional withholding tax for employees who earn more $200,000.

Do employers pay the additional Medicare tax? No, employers only pay 1.45%, even if an employee earns more than $200,000. Additional Medicare tax only applies to employees.

For example, an employee earns $250,000 per year, so the employee pays 1.45% on the $250,000 in wages, plus 0.9% on the $50,000 over $200,000.

Calculate the Medicare tax for the entire gross wages:

$250,000 X 1.45% = $3,625

As the employer, you only pay $3,625 for Medicare taxes on the employee’s $250,000.

Because the employee pays the additional Medicare tax, find the total tax amount for $50,000 ($250,000 – $200,000):

$50,000 X 0.9% = $450

Add together the totals for both to find the total the employee pays:

$3,625 + $450 = $4,075

The employee pays $450 more in Medicare taxes than the employer in this example.

Like Social Security taxes, pre-tax deductions may impact Medicare tax calculations. Subtract applicable pre-tax deductions from the total gross wages before calculating the Medicare tax amount to withhold and contribute.

For example, your employee earns $1,500 biweekly but has a $500 Section 125 deduction. Calculate the Medicare taxes for $1,000 in gross taxable wages ($1,500 – $500):

$1,000 X 1.45% = $14.50

Withhold and contribute $14.50 for Medicare taxes.

- Run payroll in 3 easy steps

- Enjoy accurate calculations

- Spend more time on what matters most

Self-employed tax

If you are self-employed, pay the entire cost of payroll taxes (aka self-employment taxes). And, pay the additional 0.9% Medicare tax, too, if you earn more than the threshold per year.

Let’s say you earn $100,000 per year. You would pay the full 12.4% of Social Security tax:

$100,000 X 12.4% = $12,400

Because you do not hit the wage base for Medicare, do not pay the additional 0.9%. However, you must pay the full 2.9% of Medicare:

$100,000 X 2.9% = $2,900

Add together the amounts for both Social Security and Medicare:

$12,400 + $2,900 = $15,300

You can also multiply your gross wage by the entirety of the FICA tax:

$100,000 X 15.3% = $15,300

If you earn more than the Social Security wages base, stop calculating Social Security tax. If you earn more than $200,000 (single), multiply all earnings over the base by 3.8% for the additional Medicare tax.

Employer-only paid taxes

In addition to the employer-employee payroll taxes you pay, there are other payroll taxes paid by employer on behalf of your employees. The two main taxes are:

- Federal unemployment tax (FUTA)

- State unemployment tax (SUTA)*

*Some states (e.g., Pennsylvania) include state unemployment tax as an employee-paid tax, too. Check with your state to see if your employees must pay into unemployment.

Federal unemployment tax is 6.0% on the first $7,000 in employee wages. However, most states and businesses receive a tax credit of 5.4% and only pay 0.6% to FUTA. So, the maximum amount most employers pay into FUTA each year per employee is $42 ($7,000 X 0.6%). If a business or state does not receive the tax credit, the maximum amount per employee is $420 ($7,000 X 6%).

State unemployment taxes and wage bases vary by state. Typically, employers receive notices from the state regarding their SUTA rate each year. States base employer rates on a number of factors, including the length of time you’ve been in business, the number of unemployment claims, etc. Check with your state to determine the wage base and your unemployment tax rate.

Your state may have additional taxes you pay as an employer (e.g., privilege tax). Contact your state for more information.

This article has been updated from its original publication date of August 9, 2021.

This is not intended as legal advice; for more information, please click here.