Do you want your business to make a profit? Duh, of course you do! But when you’re starting out, it may take a few years before you enter profit territory. And after you start making a profit, you may be at the break-even point for a while. So, what is the break-even point?

At a glance: Break-even point

- Definition: The break-even point (BEP) is where total sales equal total expenses (no profit, no loss)

- Core formulas:

- BEP in units = Fixed Costs / (Sales Price per Unit – Variable Cost per Unit)

- BEP in sales dollars = Fixed Costs / Contribution Margin Ratio, where Contribution Margin Ratio = (Sales – Variable Costs) / Sales

- Inputs you need: Fixed costs, variable cost per unit, sales price per unit, and (for multi-product businesses) your sales mix.

- What to do with it: Use BEP to set prices, control costs, plan sales targets, and monitor how close you are to profit.

What is a break-even point?

When your company reaches a break-even point, your total sales equal your total expenses. This means that you’re bringing in the same amount of money you need to cover all of your expenses and run your business. When you break-even, your business does not profit. But, it also does not have a loss.

Typically, the first time you reach a break-even point means a positive turn for your business. When you break-even, you’re finally making enough to cover your operating costs.

Also called the accounting break-even point, this metric uses revenues and expenses from your income statement. It differs from cash flow break-even (which looks at cash in vs. cash out) and from payback period (how long it takes to recover an initial investment).

Finding your break-even point can help you determine if you need to do one or both of the following:

- Increase your prices

- Cut expenses

If your business’s revenue is below the break-even point, you have a loss. But if your revenue is above the point, you have a profit.

Use your break-even point to determine how much you need to sell to cover costs or make a profit. And, monitor your break-even point to help set budgets, control costs, and decide a pricing strategy.

Break-even point formula

To learn how to find break-even point, you must know the break-even point formula. To know how to calculate break-even point, you need the following:

- Fixed costs

- Variable costs

- Selling price of the product

So, what’s the difference between fixed vs. variable costs? Fixed costs are expenses that remain the same, regardless of how many sales you make. These are the expenses you pay to run your business, such as rent and insurance.

On the other hand, variable costs change based on your sales activity. When you sell more items, your variable costs increase. Examples of variable costs include direct materials and direct labor.

Your selling price is how much you charge for the one unit or product.

Without further ado, here’s the break-even formula:

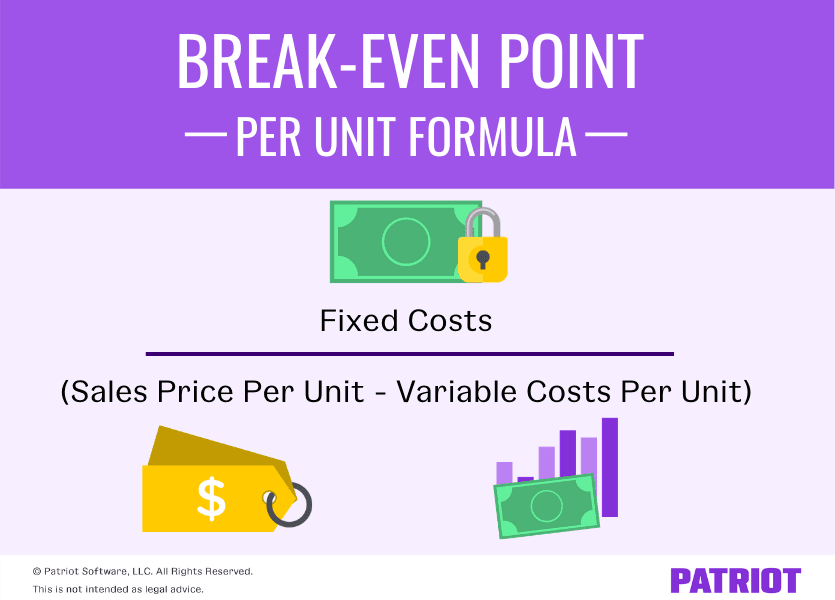

Break-even Point Per Unit = Fixed Costs / (Sales Price Per Unit – Variable Costs Per Unit)

The sales price per unit minus variable cost per unit is also called the contribution margin. Your contribution margin shows you how much take-home profit you make from a sale.

The break-even point is your total fixed costs divided by the difference between the unit price and variable costs per unit. Keep in mind that fixed costs are the overall costs, and the sales price and variable costs are just per unit.

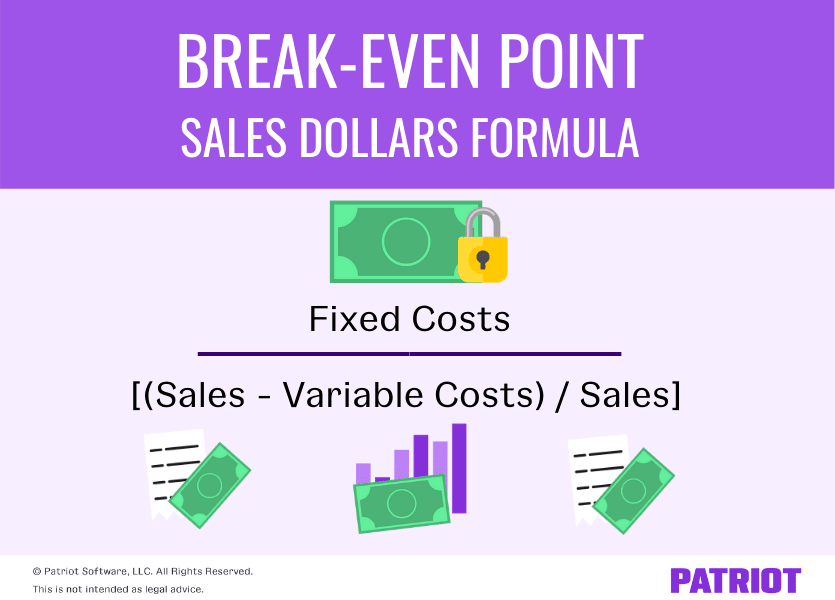

To calculate your break-even point for sales dollars, use the following formula:

Break-even Point for Sales Dollars = Fixed Costs / [(Sales – Variable Costs) / Sales]

Another way to write this is: Break-even Sales Dollars = Fixed Costs / Contribution Margin Ratio, where Contribution Margin Ratio = Contribution Margin per Unit / Sales Price per Unit (for a single product) or Total Contribution Margin / Total Sales (for multiple products).

You can use the above formulas to do a break-even analysis. A break-even analysis can help you see where you need to make adjustments with your pricing or expenses.

Step-by-step: How to calculate your break-even point

How to calculate break-even point:

- List fixed costs for the period

Monthly rent, salaries, and insurance are examples.

- Compute variable cost per unit

Materials, direct labor, packaging, and transaction fees are examples.

- Confirm your sales price per unit

Finalize numbers.

- Find contribution margin per unit

Contribution Margin per Unit = Sales Price – Variable Cost per Unit

- Find BEP in units

BEP in Units = Fixed Costs / Contribution Margin per Unit

- Find contribution margin ratio

Contribution Margin Ratio = Contribution Margin per Unit / Sales Price per Unit

- Find BEP in sales dollars

BEP in Sales Dollars = Fixed Costs / Contribution Margin Ratio

Break-even point examples

If you’re a visual learner, this one’s for you. To further understand the break-even point calculation, check out a few examples below.

Break-even point in units

Check out some examples of calculating your break-even point in units.

Example 1

Break-even point in units is the number of goods you need to sell to reach your break-even point. As a reminder, use the following formula to find your break-even point in units:

Fixed Costs / (Sales Price Per Unit – Variable Costs Per Unit)

Say you own a toy store and want to find your break-even point in units. Your fixed costs total is $6,000, your variable costs per unit is $25, and your sales price per unit is $50. Plug your totals into the break-even formula to find out your break-even point in units.

$6,000 / ($50 – $25) = 240 units

You need to sell 240 units to break even.

Example 2

Let’s take a look at how cutting costs can impact your break-even point. Say your variable costs decrease to $10 per unit, and your fixed costs and sales price per unit stay the same.

$6,000 / ($50 – $10)

$6,000 / $40 = 150 units

When you decrease your variable costs per unit, it takes fewer units to break even. In this case, you would need to sell 150 units (instead of 240 units) to break even.

Break-even point in sales dollars

The break-even point in dollars is the amount of income you need to bring in to reach your break-even point. Determine the break-even point in sales by finding your contribution margin ratio.

Again, here’s the break-even point for sales dollars formula:

Fixed Costs / [(Sales – Variable Costs) / Sales]

The following part of the above formula is for your contribution margin ratio: [(Sales – Variable Costs) / Sales]

Example 1

To simplify things, let’s use the same amounts from the last example:

- Fixed costs: $6,000

- Variable costs per unit: $25

- Sales price per unit: $50

First, find your contribution margin. Again, this is your sales price per unit minus your variable costs per unit.

Contribution Margin = $50 – 25

Contribution Margin = $25

Next, find your contribution margin ratio. Divide your contribution margin by your sales price per unit.

Contribution Margin Ratio = $25 / $50

Contribution Margin Ratio = 50% (or 0.50)

To find your break-even point, divide your fixed costs by your contribution margin ratio.

Break-even point in sales = $6,000 / 0.50

You would need to make $12,000 in sales to hit your break-even point.

Example 2

If you raise the price to $55 with variable cost still $25, CM per unit becomes $30.

New BEP units = $6,000 / $30 = 200 units.

A higher price (with demand holding) lowers the units needed to break even.

Margin of safety (quick check)

- Margin of Safety (in dollars) = Actual or Forecast Sales – Break-even Sales

- Margin of Safety (as a %) = (Actual or Forecast Sales = Break-even Sales) / Actual or Forecast Sales

A higher margin of safety means more cushion before losses begin.

How to lower your break-even point

There are several steps you can take to lower your break-even point and start turning a profit faster. These include:

- Increase price where the market allows (monitor demand)

- Reduce variable costs (negotiate materials, optimize labor, lower shipping and fees)

- Reduce fixed costs (renegotiate rent, right-size software and headcount, etc.)

- Improve product mix toward higher contribution margin items

- Reduce discounts and returns that eat into your contribution margin

Tools to calculate your break-even point

Spreadsheet: Build a simple model with inputs for fixed costs, variable costs per unit, price, and sales to automatically calculate BEP units and dollars.

Accounting software: Use profit and loss reports to identify fixed vs. variable expenses and track margins over time.

Calculator: You can use a calculator template to test “what-if” scenarios (e.g., what if you increased the price by $2)

Break-even vs. payback period vs. cash runway

- Break-even (accounting): Sales = Expenses on the income statement—no profit or loss for a period.

- Payback period: How long until cumulative cash inflows recover an initial investment. Common approach: find the last period with negative cumulative cash flow, then add the fraction needed to turn positive. Use with NPV/IRR for time value of money.

- Cash flow break-even/runway: Based on burn rate (monthly net cash outflow) and cash on hand. Runway = Cash / Monthly Burn. Improving margins and revenue growth extends runway toward profitability.

These metrics answer related but different questions: “What sales cover my costs now?” (break-even), “When do I recoup my investment?” (payback), and “How long can I operate with current cash?” (runway).

Frequently asked questions

Use BEP units = Fixed Costs / (Price – Variable Cost per Unit). For dollars, use BEP sales = Fixed Costs / Contribution Margin Ratio.

Fixed costs don’t change with sales volume (e.g., rent, salaried admin, insurance). Variable costs rise with units sold (e.g., materials, packaging, transaction fees, sales commissions). Some costs are semi-variable; use your best estimate of the variable portion.

It’s sales price minus variable cost per unit. Contribution margin represents how much each sale contributes to covering fixed costs and profit.

Use a weighted average contribution margin based on your sales mix. Then, apply the same formulas. If your mix shifts toward higher-margin items, your BEP improves.

Yes, if they’re part of your income statement for the period. Typically, they’re treated as fixed costs in basic break-even analysis.

Recalculate when prices, costs, or product mix change, and at least quarterly to keep plans aligned with current margins.

It assumes constant prices and costs, linear relationships, and a single product or stable mix. It may ignore capacity constraints and step-fixed costs (e.g., adding a new facility). Use your best judgment, and use your break-even analysis alongside cash flow analysis.

This article has been updated from its original publication date of January 3, 2017.

This is not intended as legal advice; for more information, please click here.