Just about everything you do in your business comes with a cost. Whether it’s time, money, effort, or something else, you pay a price. But, what happens when you set a limit for production and have to produce more than your set limit? You encounter what’s known as marginal cost. What is marginal cost?

Marginal cost definition

The marginal cost meaning is the expense you pay to produce another service or product unit beyond what you intended to produce. So if you planned to produce 10 units of your product, the cost to produce unit 11 is the marginal cost.

Businesses typically use the marginal cost of production to determine the optimum production level. Once your business meets a certain production level, the benefit of making each additional unit (and the revenue the item earns) brings down the overall cost of producing the product line.

Marginal costs include more than just the cost of materials. The marginal cost of production includes everything that varies with the increased level of production. For example, if you need to rent or purchase a larger warehouse, how much you spend to do so is a marginal cost.

Marginal cost is not the same as the markup on your products. Markup is how much more your selling price is than the amount the item costs you to produce.

How to calculate marginal cost (marginal cost formula)

Before we dive into the marginal cost formula, you need to know what costs to include. Marginal costs include variable and fixed costs. Variable costs include the labor and materials that go into your final product’s production. Fixed costs include expenses like administrative work and overhead.

Fixed costs do not change if you increase or decrease production levels. So, you can spread the fixed costs across more units when you increase production (and we’ll get to that later).

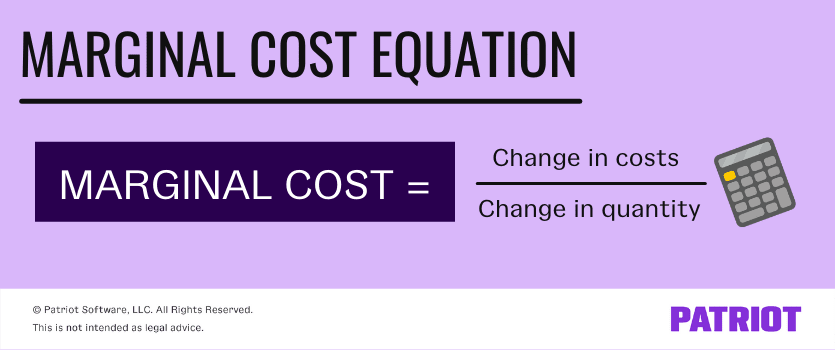

Now that you know the difference between the types of costs, let’s look at the marginal cost formula and how to find marginal cost. Your marginal costs is the total change in costs divided by the change in quantity:

Marginal Cost = Change in Costs / Change in Quantity

Change in costs

So, what is the change in costs you need for the marginal cost equation? Each production level may see an increase or decrease during a set period of time. This can occur when you need to produce more or less volume.

An increase or decrease in production costs during a set period of time is a change in costs. To calculate the total change in costs, subtract the previous production’s costs from the current batch’s costs:

Change in Costs = Production Run B Costs – Production Run A Costs

Change in quantity

The change in quantity is the difference between how many units your business produces between production runs. A change in quantity can be an increase or decrease. To determine the change in quantity, subtract the number of units your business produced in the first production run from the number of units in the second production run:

Change in Quantity = Production Run B Unit Amount – Production Run A Unit Amount

Marginal cost examples

Before we look at some examples of marginal cost, let’s find out the cost of production for a typical business.

Your business produces screen-printed T-shirts. Each T-shirt you produce requires $5.00 of T-shirt and screen printing materials to produce, which are your variable costs. You spend $2,000 each month on fixed costs (e.g., overhead). You produce 500 T-shirts each month.

To find how much it costs to produce each T-shirt on a standard production run, divide the fixed costs by the unit amount and add the variable costs:

Cost Per Unit = ($2,000 / 500) + $5.00

Cost Per Unit = $9.00

Your standard costs are $9.00 per unit.

To find your total cost of production, multiply the cost per unit by the number of units:

Cost of Production = $9.00 X 500

Cost of Production = $4,500

Your total cost of production is $4,500 per month for 500 T-shirts.

Example 1

You decide to increase your T-shirt production and produce 750 T-shirts per month. Your variable and fixed costs do not change. To find the new production cost, divide the new unit amount by the fixed costs and add the variable cost:

Cost Per Unit = ($2,000 / 750) + $5.00

Cost Per Unit = $7.67

Find your change in costs by multiplying the cost per unit by the unit amount. Subtract the new cost of production from your old cost:

Change in Costs = ($7.67 X 750) – $4,500

Change in Costs = $1,252.50

Your change in costs is $1,252.50.

To find your change in quantity, subtract your original production unit amount from the new production amount:

Change in Quantity = 750 – 500

Change in Quantity = 250

You produce 250 more units per month.

After you determine the change in costs and the change in quantity, calculate the marginal cost of production:

Marginal Cost = $1,252.50 / 250

Marginal Cost = $5.01

Your marginal cost of production is $5.01 per unit for every unit over 500. In this example, it costs $0.01 more per unit to produce over 500 units.

Example 2

In this example, you continue to produce 750 T-shirts but purchase a new facility. The new facility increases your fixed costs by $200 per month. Your new fixed costs are $2,200 ($2,000 + $200). Calculate your new costs per unit:

Cost Per Unit = ($2,200 / 750) + $5.00

Cost Per Unit = $7.93

Your new cost per unit is $7.93.

Calculate the new change in costs:

Change in Costs = ($7.93 X 750) – $4,500

Change in Costs = $1,447.50

Because your quantity did not change, you can use the marginal cost formula to calculate the new marginal cost of production:

Marginal Cost = $1,447.50 / 250

Marginal Cost = $5.79

Your marginal cost pricing is $5.79 per additional unit over the original 500 units. In this example, you can see it costs $0.79 more per unit over the original 500 units you produced ($5.79 – $5.00).

Why are marginal costs important?

The marginal cost of production helps you find the ideal production level for your business. You can also use it to find the balance between how fast you should produce and how much production is too low to help growth.

And by figuring out your marginal cost, you can more accurately determine your margin vs. markup to better price your products and turn a profit.

This is not intended as legal advice; for more information, please click here.