Withholding, remitting, and reporting payroll taxes are all a necessary part of being an employer. A big part of the responsibility of remitting these taxes is knowing when to pay them. After all, you don’t want to receive a letter from the IRS saying you missed a deadline. The government decides when you must pay the taxes, but the due dates aren’t uniform for all taxes. So, let’s answer the question, “When are federal payroll taxes due?”

When are federal payroll taxes due?

Again, the government mandates the federal payroll tax due dates for each business. The due dates for your business can depend on different factors (e.g., total tax liabilities). There are two main types of federal payroll-related taxes you must remit:

- Federal unemployment tax (FUTA)

- Federal income, Social Security, and Medicare taxes*

*Remember that Social Security and Medicare taxes are part of the Federal Insurance Contributions Act (FICA), and both employers and employees pay these taxes. You must withhold and remit federal income taxes on behalf of your employees.

Take the worry out of depositing and filing your federal payroll taxes with Patriot’s Full Service payroll software. We collect, deposit, and file your taxes for you.

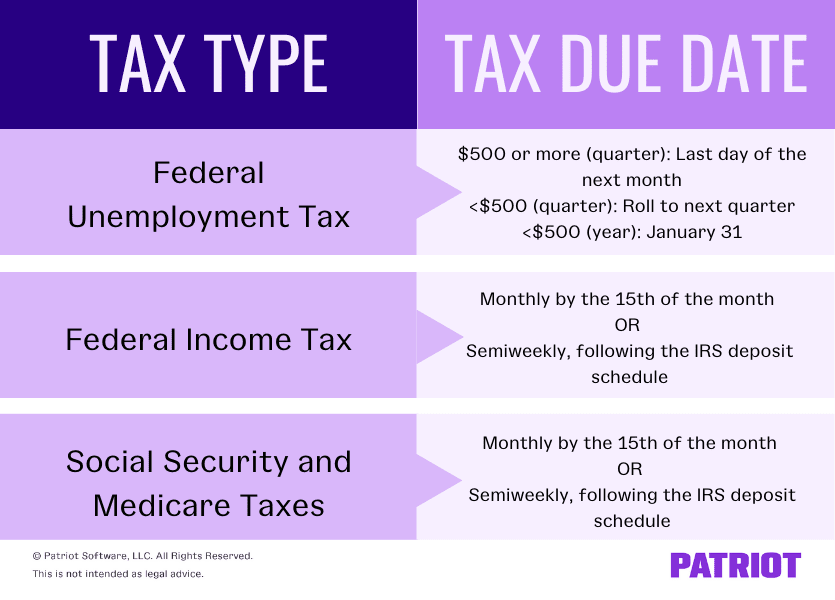

FUTA tax

As an employer, part of your employer responsibility is filing and paying FUTA tax. Because it is an employer-only tax, do not withhold FUTA taxes from your employees’ wages. FUTA taxes fund the federal government’s administration of state unemployment programs.

Generally, FUTA taxes are due quarterly. But, when you must pay FUTA tax also depends on your FUTA tax liability for the current quarter:

More than $500 in the current quarter: If your FUTA tax liability is more than $500 for the current tax quarter, deposit the funds by the last day of the month after the end of the quarter. For example, the first quarter ends on March 31. Your FUTA tax liability is due on April 30 for Quarter 1 (the last day of the month following the end of the first quarter).

Less than $500 in the current quarter: If your FUTA tax liability is less than $500 for the current quarter, roll the funds over into the next quarter. When your current quarter’s FUTA tax liability and the total amount of rolled over funds add up to more than $500, deposit the tax. If your FUTA liability is less than $500 for the entire year, deposit the funds separately or with Form 940 by January 31.

When are payroll taxes due? Check out the quarters and due dates for each quarter:

| Quarter | Quarter End Date | FUTA Tax Due Date |

|---|---|---|

| Quarter 1 (January, February, March) | March 31 | April 30 |

| Quarter 2 (April, May, June) | June 30 | July 31 |

| Quarter 3 (July, August, September) | September 30 | October 31 |

| Quarter 4 (October, November, December) | December 31 | January 31 |

If the due date falls on a weekend or banking holiday, the deposit is due the next business day.

Federal income, Social Security, and Medicare taxes

When are federal withholding taxes due? And, when are Social Security and Medicare taxes due? The good news is that all three of these taxes are due at the same time. The bad news is that the due date depends on your business and when the IRS tells you to pay the taxes.

But, there’s good news again! There are only two deposit schedules: semiweekly or monthly. Every employer must use one of these schedules. You do not get to choose your schedule. When to pay federal payroll taxes depends on the IRS’s guidelines. The IRS bases your deposit schedule on a lookback period.

If you are a monthly depositor, deposit all federal income, Social Security, and Medicare taxes (both employee and employer) by the 15th day of the following month. For example, taxes you incur in January are due by February 15. If the 15th day falls on a banking holiday or weekend, deposit on the next business day.

Remember that the pay date plays a role in paying the taxes if you’re a monthly depositor. For example, you pay your employees semimonthly. You pay your employees on February 15 for the pay period January 15 through January 31. The taxes for that pay period are due March 15 because you paid your employees in February even though the pay period was in January.

Semiweekly depositors must follow a strict tax deposit schedule:

- If your payday is on Wednesday, Thursday, or Friday, you must deposit these taxes by the following Wednesday

- If your payday is on Saturday, Sunday, Monday, or Tuesday, you must deposit these taxes by the following Friday

To learn even more about monthly and semiweekly deposit schedules, check out IRS Publication 15.

What is a lookback period?

A lookback period is a set period of time the IRS uses to review and determine your federal tax deposit schedule. How much you paid in federal payroll taxes during the lookback period determines your deposit schedule for the next tax year.

Your lookback period differs depending on what form your business files. The lookback period applies to either your Form 944 for that year (annual form) or to all four quarters on your Form 941 that year (quarterly form).

New employers have no tax liability during the lookback period. Because of this, all new employers start as monthly depositors.

Form 941

Form 941 is the quarterly form that many employers use to report their federal income, Social Security, and Medicare tax liabilities.

If you are a Form 941 filer, your lookback period is a four-quarter period that begins on July 1 and ends on June 30 of the following year. For example, the lookback period to determine your 2022 payroll tax deposit schedule is July 1, 2020 to June 30, 2021.

Using the lookback period, figure out the total amount of your tax deposits during that time. You are a monthly depositor if you paid $50,000 or less in taxes during the lookback period. You are a semiweekly depositor if you paid more than $50,000 in taxes during the lookback period.

Form 944

Form 944 is an annual form that some employers use to report their federal income, Medicare, and Social Security tax liabilities. Do not file this form unless the IRS tells you to.

The Form 944 lookback period applies to anyone who is a Form 944 filer in the current year or either of the two preceding years. The lookback period is the second preceding calendar year. For example, the lookback period for 2022 deposits is the 2020 calendar year.

Calculate your total tax liability for the lookback period. If your liability was $50,000 or less, you are a monthly depositor. If your liability was more than $50,000, you are a semiweekly depositor.

How do you pay federal payroll taxes?

You must pay all FUTA, federal income, Social Security, and Medicare taxes using the Electronic Federal Tax Payment System (EFTPS).

This article has been updated from its original publication date of February 15, 2017.

This is not intended as legal advice; for more information, please click here.